10.15.39. Other deductions: For expenses related to the promotion and training of music

For expenses related to the promotion and training of music

Amount

The amounts paid during the tax period to cover expenses related to the promotion and training of music, with the limit of 150 euros per taxpayer.

Requirements and conditions

-

Expenses that qualify for a deduction:

-

The fees and charges paid for music education at conservatories and music schools, or Music and Dance schools, registered in the Register of educational centers of the Valencian Community, both public and private.

-

The fees paid by the members of musical societies integrated into the Federation of Musical Societies of the Valencian Community.

-

Expenses related to musical training and improvement, including master's degrees, courses and seminars, taught by official teaching centers.

-

The purchase of instruments and scores within the framework of music training or dissemination activities carried out by the centers referred to in the preceding letters. The portion of expenses financed with public subsidies will not be deductible.

-

The purchase of tickets for attending music concerts organized by the entities referred to in letters a. and b. previous ones.

-

-

The sum of the general taxable base and the savings taxable base must not exceed 60,000 euros in individual taxation or 78,000 euros in the case of joint taxation.

-

The disbursements may be used for expenses made by the taxpayer, their spouse, and those persons who give the right to the application of the family allowances for descendants.

-

When two taxpayers are entitled to this deduction because they have paid expenses related to the acquisition of goods or services for other people, the deduction base will be divided equally between them.

-

The amounts must have been paid by credit or debit card, bank transfer, nominative check or deposit into accounts at credit institutions.

Limit

The deduction limit will apply to taxpayers whose sum of the general taxable base (box 0500) and the savings taxable base (box 0510) is less than 54,000 euros in individual taxation, or less than 72,000 euros in joint taxation.

When the sum of the general taxable income and the savings taxable income is between 54,000 and 60,000 euros in individual taxation, or between 72,000 and 78,000 euros in joint taxation, the amount of the deduction limit will be as follows:

-

In individual taxation, the result is the product of the deduction limit and a percentage obtained from the application of the following formula: 100 X (1 – the coefficient resulting from dividing by 6,000 the difference between the sum of the general taxable base and the taxpayer's savings and 54,000).

-

In joint taxation, the result of multiplying the deduction limit by a percentage obtained from the application of the following formula: 100 X (1 – the coefficient resulting from dividing by 6,000 the difference between the sum of the general taxable base and the taxpayer's savings and 72,000).

Completion

To complete the deduction for expenses related to the promotion and training of music (created by Decree Law 2/2026, of March 6, of the Consell) taxpayers must calculate the amount of the deduction to which they are entitled and enter it in Renta Web as follows:

-

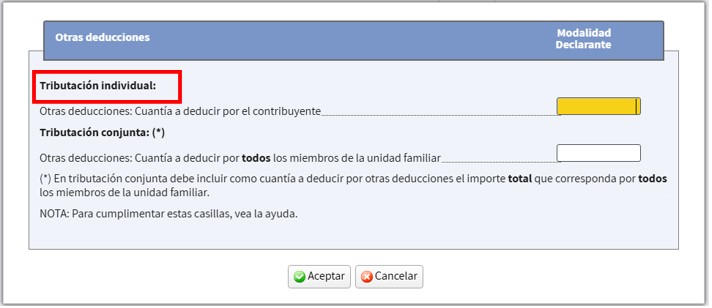

If they file an individual tax return: They will enter the amount of the deduction in the "Other deductions" box (box 1121) within the "Individual taxation" section.

-

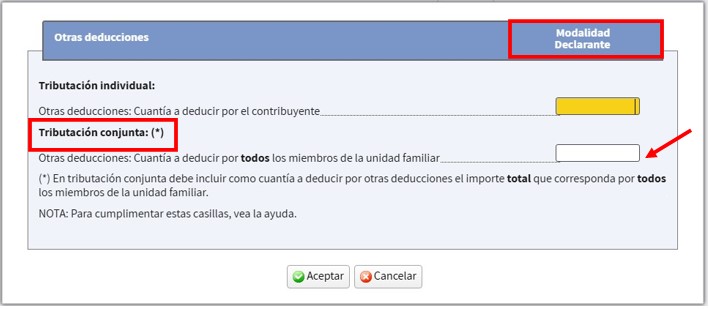

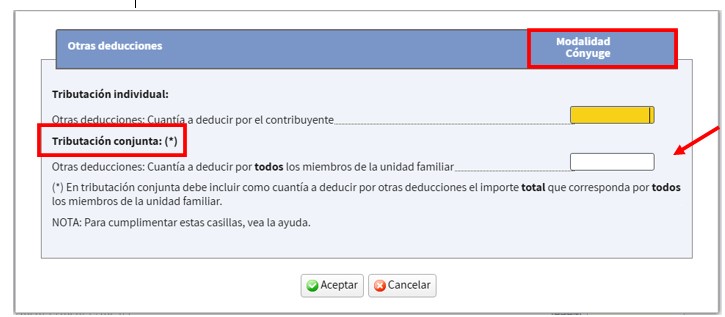

If you file a joint return: They will declare the total amount of the deduction to which both spouses are entitled, indiscriminately in the declaration of the declarant or in that of the spouse in the box “Other deductions” (box 1121) within the section “Joint taxation”.

Or in “Other deductions” of the spouse's “Joint Taxation” return.

Since this is a single box for joint taxation, the total amount entered by one spouse will be transferred to the other. The amount of the deduction to which they are entitled is the amount shown in that box for the taxpayer or the spouse, not the sum of both. You can check the amount you are entitled to by selecting box (1121) "Other deductions" in "Joint method".

Examples of completion

-

A single taxpayer with no children pays 1,000 euros for a music training course at an official teaching center. The taxpayer has a general taxable base of 80,000 euros (box 0500 of their tax return) and a savings taxable base of 5,000 euros (box 0510 of their tax return).

Since the sum of the taxable bases exceeds 60,000 euros, the taxpayer is not entitled to the deduction and therefore will not enter any amount in "Other deductions".

-

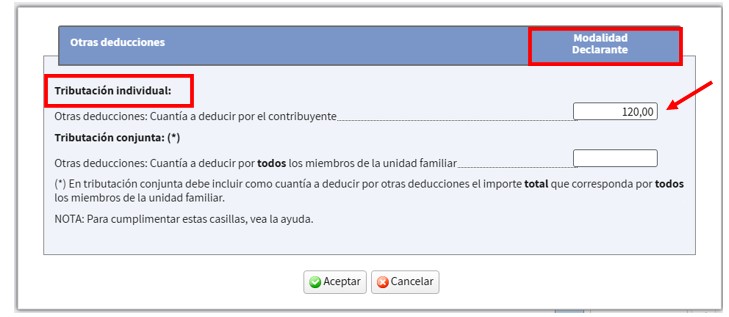

A single taxpayer with no children has purchased sheet music for an amount eligible for deduction of 120 euros. The taxpayer has a general taxable base of 20,000 euros (box 0500 of their tax return) and a savings taxable base of 500 euros (box 0510 of their tax return).

Calculation of the deduction limit: The general taxable base plus the savings taxable base is 20,500 euros (box 0500+box 0510= 20,000+500). Since this amount is less than 54,000, the deduction limit is 150 euros.

The deduction will be the amounts paid (120 euros) with a limit of 150 euros. Therefore, in the "Other deductions" box, "Individual taxation" will enter 120 euros.

-

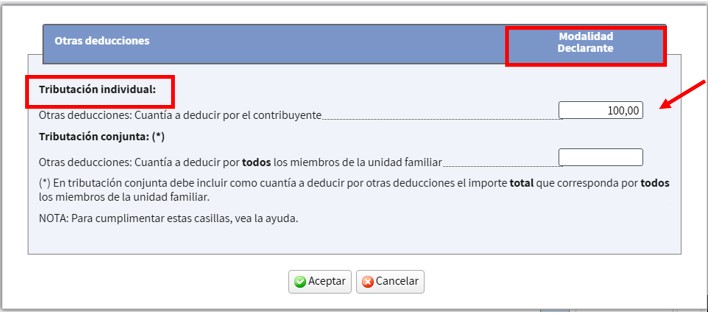

A single taxpayer with no children has purchased concert tickets that qualify for the deduction for an amount of 100 euros. The taxpayer has a general taxable base of 55,000 euros (box 0500 of their tax return) and a savings taxable base of 200 euros (box 0510 of their tax return).

Calculation of the deduction limit: The general taxable base plus the savings taxable base is 55,200 euros (box 0500+box 0510= 55,000+200). Since this amount is greater than 54,000, the deduction limit is less than 150 euros.

The amount of the deduction limit will be: 150*[100*(1-(55,200-54,000)/6,000)]%= 150*80%=120 euros.

The deduction will be the amounts paid (100 euros) with the previously calculated limit (120 euros). Therefore, in the "Other deductions" box, "Individual taxation" will enter 100 euros.

-

A married couple has paid a total of 2,000 euros in fees to the music conservatory attended by their son, for which they are entitled to apply the minimum allowance for dependents.

The declarant has a general taxable base of 56,600 euros (box 0500 of his declaration) and a savings taxable base of 400 euros (box 0510 of his declaration).

The spouse has a general taxable base of 17,800 euros (box 0500 of their declaration) and a savings taxable base of 400 euros (box 0510 of their declaration).

In the joint declaration, the general taxable base is 73,000 euros (box 0500 of the joint declaration) and the taxable base for savings is 800 euros (box 0510 of the joint declaration).

Both spouses will file the returns, choosing the tax option that is most favorable to them.

-

If they file an individual tax return.

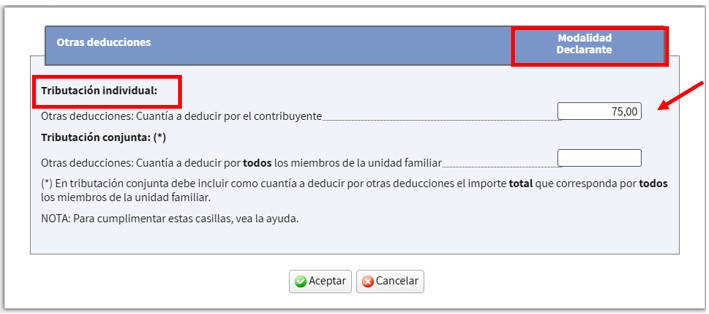

The declarant:

Calculation of the deduction limit: The general taxable base plus the savings taxable base is 57,000 euros (box 0500+box 0510= 56,600+400). Since this amount is greater than 54,000, the deduction limit is less than 150 euros.

The amount of the deduction limit will be: 150*[100*(1-(57,000-54,000)/6,000)]%= 150*50%= 75 euros.

The deduction will be 1,000 euros (2,000/2) with the previously calculated limit (75 euros). Therefore, in the "Other deductions" box, "Individual taxation" will be entered as 75 euros.

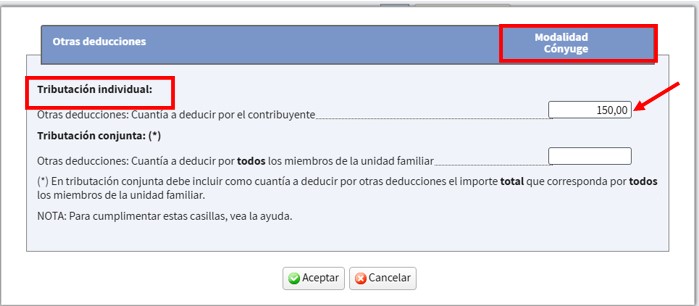

The spouse:

Calculation of the deduction limit: The general taxable base plus the savings taxable base is 18,200 (box 0500+box 0510= 17,800+400). Since this amount is less than 54,000, the deduction limit is 150 euros.

The deduction will be 1,000 euros (2,000/2) with a limit of (150 euros). Therefore, in the "Other deductions" box, "Individual taxation" will be entered as 150 euros.

-

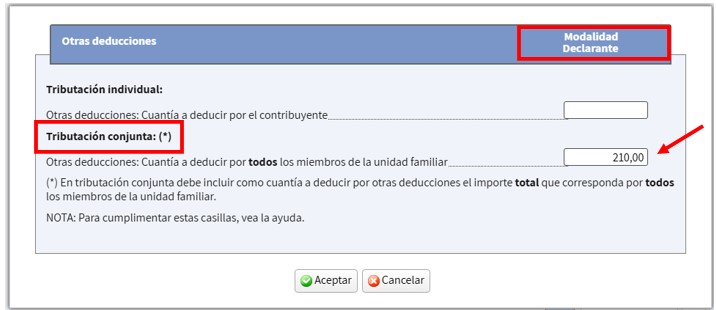

If they file a joint return.

Calculation of the deduction limit: the general taxable base plus the savings taxable base 73,800 euros (box 0500+box 0510 =73,000+800). Since this amount is greater than 72,000, the deduction limit is less than 150 euros per taxpayer.

The amount of the deduction limit for each taxpayer it will be: 150*[100*(1-(73,800-72,000)/6,000)]%=150*70%= 105 euros.

The deduction for the declarant will be 1,000 euros (2,000/2) with the limit of (105 euros).

The deduction for the spouse will be 1,000 euros (2,000/2) with a limit of (105 euros).

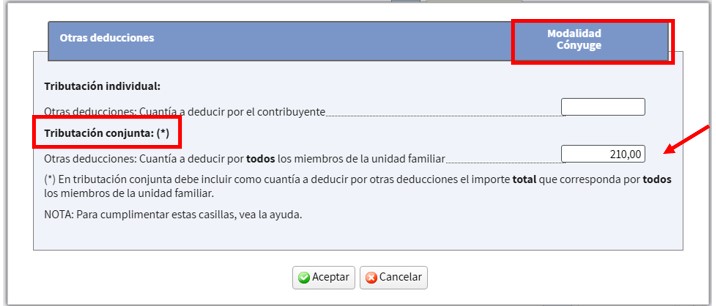

In the joint declaration the deduction will be the sum of both amounts 210 euros. Therefore, in the “Joint Taxation” box 210 euros will be deposited from the declaration of the declarant or the spouse. This amount will be reflected for both the declarant and the spouse.

If it is stated in the declarant's declaration.

If it is included in the spouse's declaration.

The amount of the deduction in joint taxation (210 euros) can be viewed by selecting box 1121 in “Joint modality”.

-

In the event that you have already filed the return without including the amount of this deductionYou will need to modify the submitted declaration, which will result in a lower amount to be paid or a larger refund. You can find more information on how to submit this amendment at: Modify a previously submitted declaration 2025.