10.7.26. Other deductions: For savings-investment in the acquisition or construction of the first main residence and for expenses derived from veterinary controls and vaccination for the ownership of assistance dogs

For savings-investment in the acquisition or construction of the first main residence

-

Amount

He 15% of the amounts deposited during the tax period in accounts of credit institutions provided that the taxpayer allocates, before the lapse of 6 years from the date of opening of the account, the deposited amount that has generated the right to the deduction to the acquisition or construction of his first main residence.

The maximum annual deduction will be 750 euros and the maximum total will be 3,000 euros.

-

Requirements and conditions

-

Taxpayers must be under 36 years of age.

-

The property must be located within the territory of the Autonomous Community of Castilla-La Mancha and be considered a primary residence in accordance with the Personal Income Tax Law.

-

For the purposes of this deduction, the acquisition of housing shall be understood as the acquisition in the legal sense of the right of ownership or full control thereof, without such consideration being distorted because this property is shared with other co-owners.

-

The sum of the general tax base and the savings base cannot exceed 27,000 euros in individual taxation or 36,000 euros in joint taxation.

-

In the case of joint taxation, the amount of the deduction will be prorated among the taxpayers based on the contribution made by each of them.

-

Amounts deposited in accounts that have generated the right to deduction may not be subject to deduction again when they are used for the acquisition of the main residence.

-

Contributions made into the account within the year in which the taxpayer turns 36 may be included in the deduction.

-

The accounts in which the amounts used to calculate the deduction are deposited must be separate from any other type of taxation, and each taxpayer may only maintain one such account.

-

The account balance on the tax accrual date must be higher than on the accrual date of the previous tax period, at least by the same amount that gave rise to the deduction.

-

The requirement of availability will be considered not to be breached when the deposited amounts that have generated the right to the deduction are fully replenished or contributed prior to the accrual of the Tax, to an account of the same or another credit institution that fulfills the same purpose and conditions.

-

The requirement that the amount in the account be used for the acquisition of the main residence will not be considered unfulfilled in the event of the taxpayer's death before the end of the maximum period of 6 years.

-

In the event of non-compliance that results in the loss of the right to deductions already claimed, the taxpayer must regularize the tax situation in accordance with the Personal Income Tax regulations.

-

For expenses related to veterinary check-ups and vaccinations for owning assistance dogs

-

Amount

He 30% of the amounts paid in the tax period for veterinary expenses and vaccination derived from the ownership of assistance dogs.

The maximum amount of the deduction will be 100 euros per year per taxpayer and will be applicable throughout the period of ownership of the animal by the taxpayer.

-

Requirements and conditions

-

For the purposes of this article, assistance dogs shall be understood as those defined in paragraph cc) of article 3 of Law 7/2023, of March 28, on the protection of the rights and welfare of animals and in articles 2.h) and 4 of Law 5/2018, of December 21, on access to the environment of people with disabilities accompanied by assistance dogs.

Assistance dog: The one who, after passing a selection process, has completed his training in a specialized entity officially recognized or approved by the competent administration, with the acquisition of the necessary skills to provide service and assistance to people with disabilities, as well as warning dogs or dogs for assistance to people with autism spectrum disorder.

Assistance dogs are classified as follows:

-

Guide dog: The dog trained to guide a person with a visual impairment, whether total or partial, or with an additional hearing impairment.

-

Sound signaling dog: The dog trained to alert people with hearing disabilities to the emission of sounds and their origin.

-

Service dog: The dog is trained to provide help and assistance to people with physical disabilities in daily life activities, both in the private and public environment.

-

Warning dog: The dog trained to give a medical alert to people suffering from recurrent seizures with sensory disconnection resulting from a specific disease such as diabetes, epilepsy or another legally recognized organic disease.

-

Dog for people with autism spectrum disorder: The dog is trained to protect the physical integrity of a person with autism spectrum disorder, guide them, and control emergency situations they may experience.

The following are excluded from the scope of this law:

-

Dogs used in animal-assisted therapy activities, even when the recipients are people with disabilities.

-

Dogs used in projects for the care or treatment of people who are victims of gender violence or other crimes, people at risk or social exclusion, or elderly people.

-

Dogs intended to provide emotional support to people affected by personality disorders or mental illness.

-

Any other animals other than those of the canine species, regardless of their purpose.

-

-

Expenses related to vaccinations, deworming, sterilization and other treatments that are mandatory according to the specific regulations applicable to assistance dogs will be considered deductible, provided they have been effectively paid by the taxpayer.

-

That the link between the passive subject and the assistance dog has been recognized by the competent department for social welfare, in accordance with Law 5/2018, of December 21, or by another autonomous community.

-

That the expenses are duly justified by means of an invoice issued by a legally authorized veterinary professional or center.

-

That the expenses have not been subsidized by public or private entities.

-

The sum of the general tax base and the savings base cannot exceed 27,000 euros in individual taxation or 36,000 euros in joint taxation.

-

Completion

To complete the deductions for savings-investment in the acquisition or construction of the first main residence and for expenses derived from veterinary controls and vaccination for the ownership of assistance dogs (introduced by Law 1/2026, of March 26, on Administrative and Tax Measures of Castilla-La Mancha) taxpayers must calculate the amount of the deduction(s) to which they are entitled and enter it in Renta Web as follows:

-

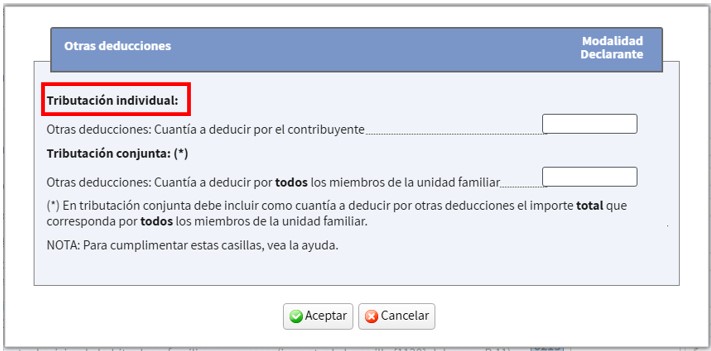

If they file an individual tax return: They will enter the amount of the deduction(s) in the "Other deductions" box (box 0969) within the "Individual taxation" section.

-

If you file a joint return: They will declare the total amount of the deduction(s) to which both spouses are entitled, indiscriminately in the declarant's declaration or in that of the spouse in the box "Other deductions" (box 0969) within the section "Joint taxation".

Or in “Other deductions” of the spouse's “Joint Taxation” return.

Since this is a single box for joint taxation, the total amount entered by one spouse will be transferred to the other. The amount of the deduction to which they are entitled is the amount shown in that box for the taxpayer or the spouse, not the sum of both. You can check the amount you are entitled to by selecting box (0969) "Other deductions" in "Joint Provision".

Examples of completion

-

A single taxpayer with no children pays 200 euros for the vaccination of his assistance dog. The sum of the general tax base (box 0435) and the savings base (box 0460) is 40,000 euros.

Since the sum of the bases exceeds 27,000 euros, the taxpayer is not entitled to the deduction and therefore will not enter any amount in "Other deductions".

-

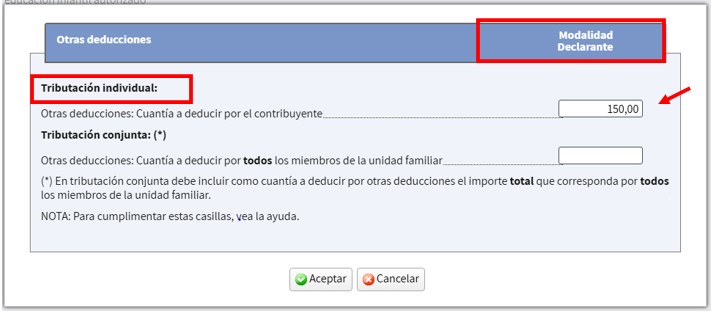

A single taxpayer without children meets the requirements to apply the savings-investment deduction for the acquisition or construction of the first main residence having deposited 1,000 euros in the year.

Deduction amount: 1,000*0.15= 150 euros. Since the maximum annual deduction is 750 euros, the amount of the deduction will be 150 euros.

The declarant will enter 150 euros in the "Other deductions" box "Individual taxation" in their declaration.

Amount of the deduction

-

A married couple meets the requirements to apply for the savings-investment deduction in the acquisition or construction of their first main residence.

The declarant has deposited 10,000 euros in the year and the spouse 8,000 euros.

-

If they file an individual tax return:

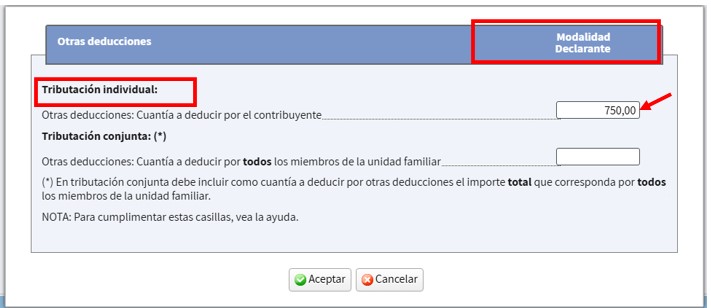

The declarant:

Deduction amount: 10,000*0.15= 1,500 euros. Since the maximum annual deduction is 750 euros, the amount of the deduction will be 750 euros.

The declarant will enter 750 euros in the "Other deductions" box "Individual taxation" in their declaration.

ImpoPart of the deduction “Declarant modality” box 0969

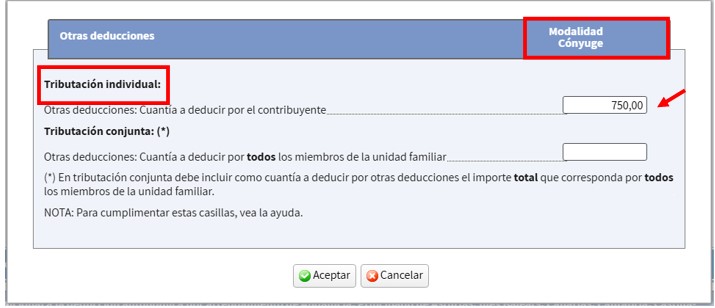

The spouse:

The amount of the deduction will be: 8,000*0.15= 1,200 euros. Since the maximum annual deduction is 750 euros, the amount of the deduction will be 750 euros.

The spouse will enter 750 euros in the "Other deductions" box under "Individual taxation" in their tax return.

Ideduction amount “Spouse modality” box 0969

-

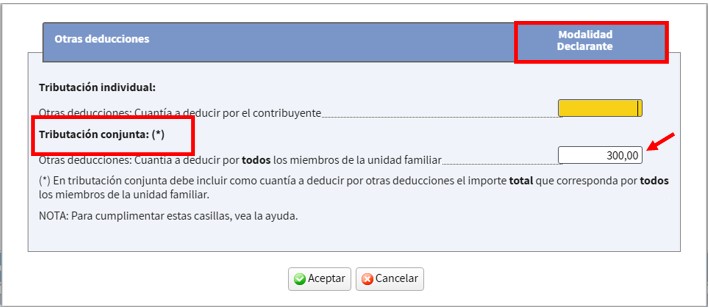

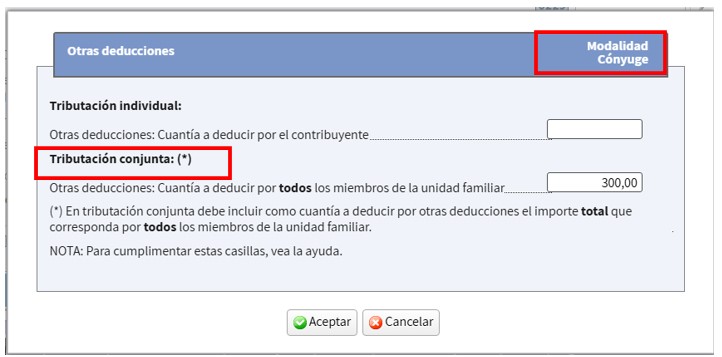

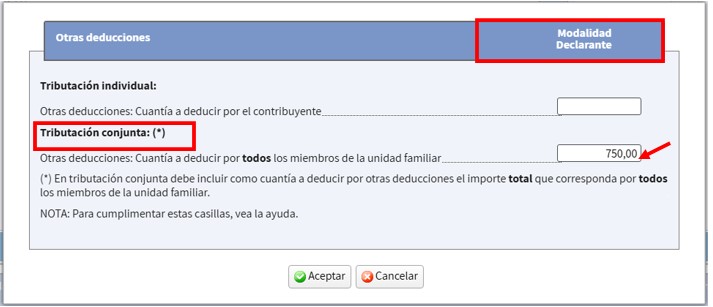

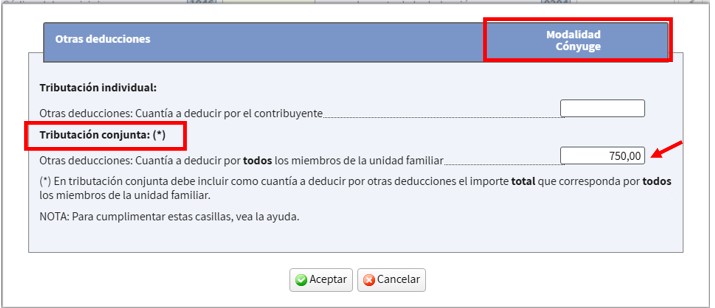

If they file a joint return

The amount of the deduction will be: (10,000+8,000)*0.15= 2,700 euros. Since the maximum annual deduction is 750 euros, the amount of the deduction in joint taxation will be 750 euros.

In the "Other deductions" box within the "Joint taxation" section dand the individual declaration of the declarant or the spouse 750 euros will be deposited. This amount will be reflected for both the declarant and the spouse.

If it is stated in the declarant's declaration.

If it is included in the spouse's declaration.

The amount of the deduction in joint taxation (750 euros) can be viewed by selecting box 0969 in “Joint modality”.

-

-

If, exceptionally, a taxpayer is entitled to the deduction for savings-investment in the acquisition or construction of the first main residence and for expenses derived from veterinary controls and vaccination for the ownership of assistance dogs, they will calculate the amount of each deduction and the sum of both will be entered in the "Other deductions" box in accordance with the above.

In the event that you have already filed the return without including the amount of these deductions You will need to modify the submitted declaration, which will result in a lower amount to be paid or a larger refund. You can find more information on how to submit this amendment at: Modify a previously submitted declaration 2025.