Introduction

Regulations: Art. 50 LawPIT

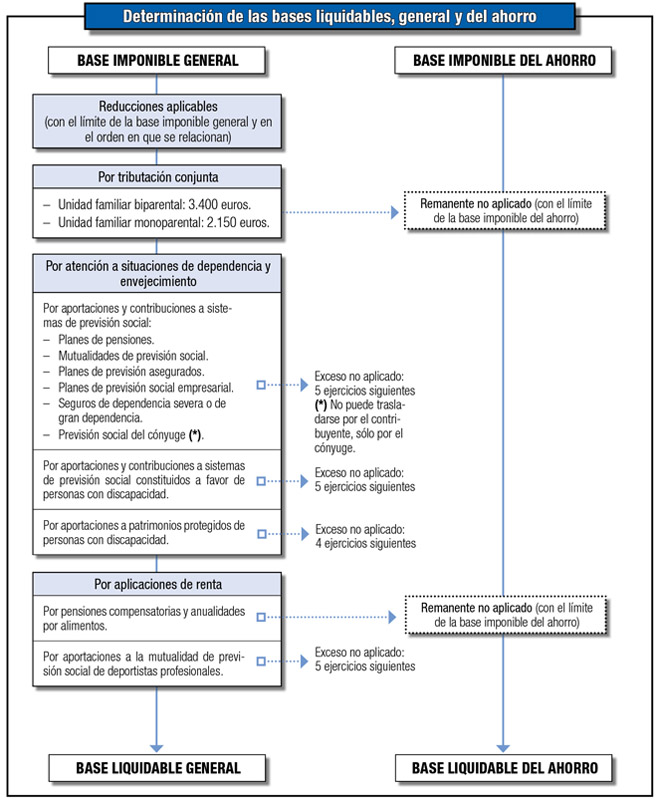

Once the general tax base and the savings taxable base have been determined, as a result of the income integration and compensation procedure discussed in the previous chapter, the general taxable base and the savings taxable base must be determined. The process of determining these last magnitudes can be represented schematically as follows:

The general taxable base is the result of applying the legally established reductions to the general tax base. whose commentary is made in this Chapter.

The taxable savings base is the result of decreasing the taxable savings base by the unapplied remainder , if any, of the reductions for joint taxation, compensatory pensions and alimony annuities, without this being able to result in a negative result as a consequence of such reductions.