Graphic scheme: Application of personal and family minimum and determination of full contributions

Taxation of the general taxable base

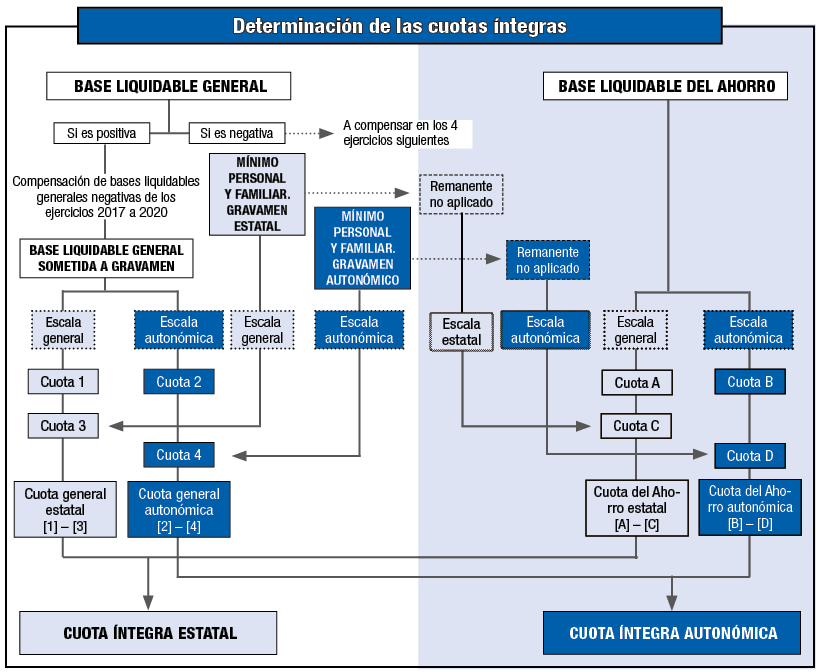

The taxation of the general taxable base of personal income tax is structured in four phases:

Phase 1: The general and regional tax scales are applied to the entire general taxable base, including the amount corresponding to the personal and family minimum that forms part of it, obtaining the corresponding partial quotas (Quota 1 and Quota 2).

Phase 2: The general scale of the tax is applied to the part of the general taxable base corresponding to the state personal and family minimum established in the Personal Income Tax, obtaining the partial quota (Quota 3).

Phase 3: The corresponding autonomous scale is applied to the part of the general taxable base corresponding to the personal and family minimum increased or decreased by the amounts established, where applicable, by the Autonomous Community in its autonomous regulations, obtaining the partial quota (Quota 4).

In the 2021 financial year, the Autonomous Community of the Balearic Islands, the Community of Madrid and the Autonomous Community of La Rioja have regulated personal and family minimum amounts different from those established in the Personal Income Tax Law. Consequently, taxpayers resident in their territory must apply, for the purposes of the regional tax (phase 3), the amounts regulated in the regulations of said Autonomous Community.

The rest of the taxpayers (including those of the Community of Castilla y León, which has set amounts for the personal and family minimum of identical amounts to those established in the Personal Income Tax Law) must apply the same amount of the personal and family minimum for the purposes of the state tax (phase 2) and the regional tax (phase 3).

Note: Please note that the Autonomous Community of Catalonia had regulated in its article 88 of the Law of the Parliament of Catalonia 5/2020, of April 29, on fiscal, financial, administrative and public sector measures, and on the creation of the tax on facilities that impact the environment, a minimum of the taxpayers that has been declared unconstitutional by the Judgment of the Constitutional Court 186/2021, of October 28, issued in the constitutional appeal 1200-2021.

Phase 4: The general state full quota (Quota 1 minus Quota 3) and the general autonomous full quota (Quota 2 minus Quota 4) are calculated from the four partial quotas obtained.

Taxation of the taxable base of savings

The taxation of the taxable base of personal income tax savings is structured in four phases:

Phase 1: The amount of the taxable savings base is taxed at the rates of the state and regional savings scale set for 2021, obtaining the corresponding partial quotas (Quota A and Quota B).

Phase 2: The amount of the state quota resulting from applying the scale to the taxable savings base (Quota A) will be reduced, where applicable, by the amount derived from applying the state savings scale set for 2021 (Quota C) to the remainder of the unapplied state personal and family minimum (that is, to the excess of the aforementioned minimum over the amount of the general taxable base).

Phase 3: The amount of the regional quota resulting from applying the scale to the taxable savings base (Quota B) will be reduced by the amount derived from applying to the unapplied remainder of the regional personal and family minimum (that is, to the excess of the aforementioned minimum over the amount of the general taxable base) the regional savings scale set for 2021 (Quota D).

Phase 4: From the four partial quotas obtained, the full quota of state savings (Quota A minus Quota C) and the full quota of regional savings (Quota B minus Quota D) are calculated.