Process description

Broadly speaking, the IOSS works as follows:

- The seller is registered for the purposes ofVAT in a single Member State, applies and collects the corresponding VAT on distance sales of goods dispatched or transported to consumers in the EU, and declares and settles said VAT to the Member State of identification, which will then distribute it among the Member States of destination of the goods.

- In this case, the goods are exempt from VAT when imported into the EU. The customs authorities of the Member State of import prepare a monthly list of the value of imports for each IOSS VAT identification number and share it with the tax administration of the Member State of identification.

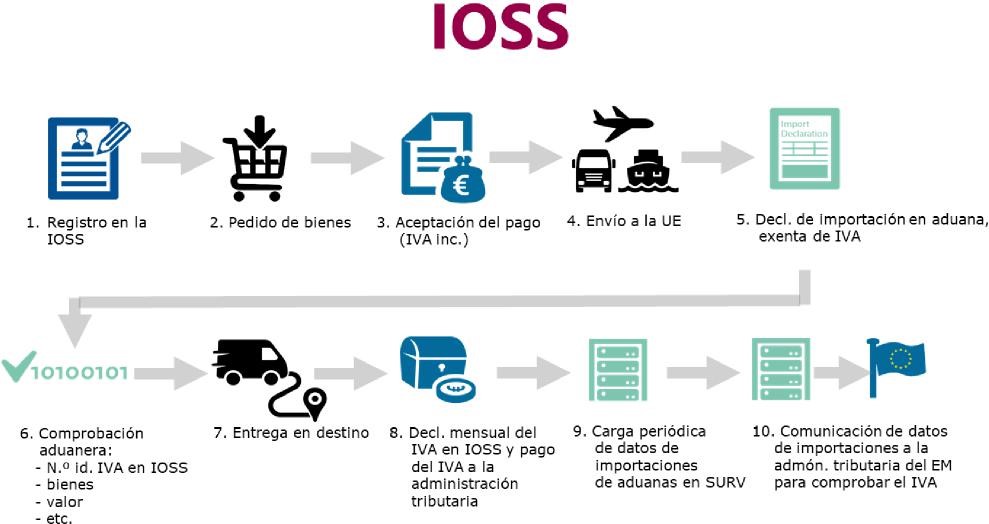

The following image shows a summary of the IOSS process.11:

11 Please note that this is a simplified assumption and there are several alternatives. ( e.g. As regards payment, it can also be made upon delivery).