FAQs

What does this entail?

The publicationStatistics on Wealth Tax DeclarantsIt is a census-based operation, based on the annual declarations of the declaration form D-714 (Wealth Tax) submitted by all taxpayers obliged to declare due to personal obligation (residents) or real obligation (non-residents). The Wealth Tax is a direct, personal tax levied on the net assets of individuals under the terms established by law. This tax is understood to be the set of assets and rights of economic content held by the individual as of December 31 of the year in which the tax is levied, less any charges and encumbrances that diminish their value and any personal debts and obligations for which they are liable.

What information can be found in this publication?

In this statistic, the Tax Agency publishes three blocks of information. Block I, "Distribution of assets", contains a set of tables referring to the structure of the assets, broken down in turn into each of the components. In the other two blocks, the information is presented item by item grouped by types of assets following the structure of the model itself, but while in the second block the information is presented item by item by Tax Base sections, in Block III the summary information of the declarations corresponding to the personal obligation to declare is presented classified by Autonomous Communities of the Territory of application of the tax.

What does it contribute to heritage analysis?

The Wealth Tax Declarants Statistics provides information on the assets of individuals who are required to file a tax return. It also provides information on the distribution of personal assets by asset type.

Where do you get the information from?

The "Statistics on Wealth Tax Declarants" is obtained from the administrative records of Wealth Tax returns for the fiscal year covered by the statistics. The information provided is static and refers to assets as of December 31 of the reference year of the declaration.

Who is required to file a declaration?

As of 2011, taxpayers who are individuals and who meet any of the following circumstances are required to file a Wealth Tax return: when yourtax basedetermined in accordance with the rules of the tax isgreater than 700,000 eurosor when, if the above circumstance does not apply, the value of their total assets or rights, regardless of where they are located, determined in accordance with the regulations governing the Tax, is greater than 2,000,000 euros. Furthermore, all taxpayers under real obligation were also liable for the tax, that is, all natural persons who did not have their habitual residence in Spanish territory, but who held property or rights that could be exercised there.

Why is there no publication from 2008 to 2010?

Effective January 1, 2008, the tax burden on this tax was eliminated, both for personal and real obligations. A 100% tax credit was applied to the total amount owed. The formal obligation to file a tax return was eliminated. This is why there are no administrative records to obtain the basic statistical information. Royal Decree-Law 13/2011, of September 16, reinstated the tax levy with effect for the 2011 and 2012 fiscal years. Subsequently, Law 16/2012, of December 27, extended the validity of the tax to 2013, and Law 22/2013, of December 23, on the General State Budget for 2014, in its Article 72, extended the obligation to file the tax to 2014.

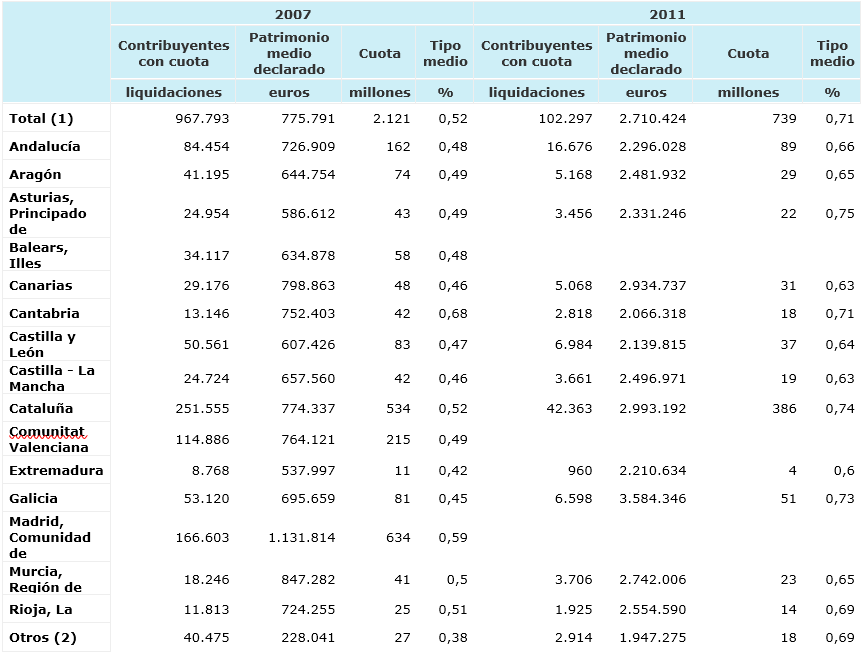

Are the statistics from 2007 comparable with those from 2011 and later?

There are numerous differences between the two statistics due to changes in the tax. The fundamental difference lies in the conditions of the personal obligation to declare. While in 2007, the taxpayers of the tax by personal obligation were natural persons resident in Territories with a Common Tax Regime whose taxable base determined in accordance with the rules of the tax was greater than 108,182.18 euros or, when, not having the previous circumstance, the value of the goods or rights, in accordance with the rules of the tax was greater than 601,012.10 euros. In 2011, the previous limits were increased to 700,000 euros and 2,000,000 euros, respectively. Furthermore, it is worth noting the changes in the rate scale and the fact that, in 2011, some autonomous communities They maintained the 100% tax rebate.

The following table shows a comparison of the main variables in 2007 and 2011. In it you can clearly see the changes between one year and the next.

Who is required to file the Temporary Solidarity Tax on Large Fortunes (ITSGF)?

Individuals who are taxpayers of the Wealth Tax, whether by actual or personal obligation, provided their assets exceed 3,000,000, are subject to this tax and must file a ITSGF return, form 718, provided that the taxable amount for this tax, after applying any applicable deductions or allowances, is payable.

Note

(1) In 2011, only the CC.AA. are taken into account. with positive quota.

(2) Ceuta, Melilla and taxpayers by royal obligation.