Tax revenues and their comparison with the Budget

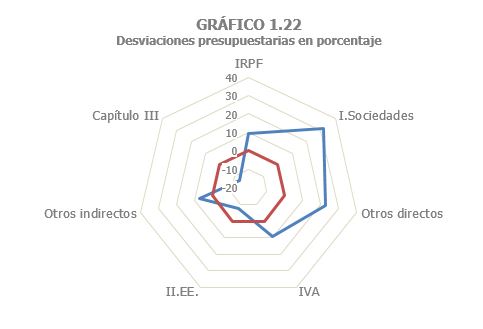

Revenues in 2022 were much higher than budgeted, even despite the fact that the measures on the price of electricity were extended for the first six months of the year after the presentation of the 2022 Budgets and were extended again and expanded (with the additional reduction in the VAT rate) already late this year. The collection exceeded the budget by 23.111 billion ( Table 1.7 ). The largest deviations occurred in the Personal Income Tax (about 9,353 million, due to the favorable performance of employment and salaries and the good results of the annual declaration), in the Corporate Tax (7,699 million due to the improvement in profits and the increase in income from the 2021 annual declaration) and VAT (6,944 million due to the positive evolution of consumption and the acceleration of prices).

Income from personal income tax was higher than expected, amounting to 9.353 billion, 9.3% of the budgeted revenue. The main source of deviation is found in work retentions. The improved performance of employment and average remuneration compared to what was contemplated in the macroeconomic scenario of the 2022 Budget largely explains the higher income (in 2021, an increase in employee remuneration for 2022 of 3.8% was forecast and the year closed with an increase of 6.5%). The other source of positive deviation was the results of the annual declaration, both due to higher income and lower returns.

In terms of corporate tax, revenue was 7,699 million higher than that included in the 2022 Budget, i.e. 31.5% higher than expected. The deviation, which was concentrated in the fractional payments, was due to a forecast for the end of 2021, the basis for the 2022 projection, which assumed lower revenues than those finally recorded.

In VAT, the final collection was 6,944 million above what was forecast in the 2022 Budgets (9.2% more than budgeted). The main reason for this deviation was the assumptions about price growth in the macroeconomic scenario projected last year, which assumed lower price increases than actually occurred.

In Special Taxes, however, the deviation was negative: The collection was lower than budgeted by 1.62 billion (-7.4% compared to the forecast). The main cause of the error was the extension to the whole of 2022 of the reduction in the rate of the Electricity Tax, a measure approved in mid-September 2021, initially with a duration of three and a half months and, therefore, with an expected impact of only one month on cash income in 2022. Added to this is the negative effect of fuel prices on revenue from the Hydrocarbon Tax.

Three concepts stand out in the rest of the income: the Tax on Foreign Trade with a deviation of 878 million due to the increase in import prices above expectations; the underestimation of other revenues in Chapter II amounting to 608 million due to the delay in the entry into operation of the Tax on Single-Use Plastics; and the negative deviation of 256 million in the Rates as a result of the ruling that left the Fee for the use of continental waters for the production of electrical energy without income.