3. Corporate Income Tax

Corporate tax revenues grew by %, mainly the very favourable performance of profits in both 2022 and 2021. The former were reflected in a sharp increase in split payments (17.7%), which was also widespread by type of company, although particularly high in consolidated groups and, within them, in groups in the banking and energy sectors. The 2021 profits were reflected in a significant increase (41.7%) in the annual return revenues, mostly from the 2021 return filed in July 2022. The impact of this increase on total tax revenue was offset by the increase in refunds (26.6%) as a result of the increase in applications in the last campaign (about 5,000 million more than the previous year), the advance in the implementation of these refunds compared to last year and the existence of extraordinary refunds derived from sentences or linked to deferred tax assets (DTA).

The consolidated tax base of Corporate Tax grew by 20.8% ( Table 3.1 ), linking two years of strong increases (in 2021 the increase was 35.5%, although the comparison was made with the year with the highest incidence of the pandemic). Profits also grew at a good pace, by 17% (36% in 2021). These increases, already remarkable in themselves, are even more so when one takes into account that they are compared with a year in which extraordinary operations were recorded (a bank merger and the sale of assets by a large company). In the case of split payments ( Table 3.2 ), the profits of consolidated groups rose by 14.9%, reaching almost 60% for those who paid taxes according to their minimum payment, while for Large Companies not integrated into groups the increase was 19%.

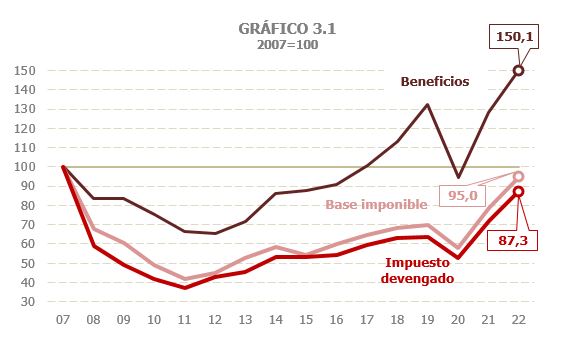

Chart 3.1 shows the 2022 figure in the context of the evolution of the tax over the last 15 years. Profits for 2022 represent a new record in the historical series, surpassing the figure achieved in 2019. Compared to 2007, the year with the highest corporate tax collection, profits are 50% higher than then. However, the tax base and the tax accrued are still below the 2007 figures. The same is true for tax revenue, which is still lower than that achieved in the 2005-2007 period. The detailed trend of the tax since 1995 is shown in Table 8.5.

The effective rate on the tax base remained practically stable (+0.2%; Table 3.1 ; Chart 3.5 ), following the trend of recent years (the 2022 rate is the same as that of 2017) and as a logical consequence of regulatory stability. The rate on profits, which depends not only on regulations but also on the different pace of profit growth in different types of companies, is expected to rise by 3.5%, although the level is still lower than the average rate observed before 2018.

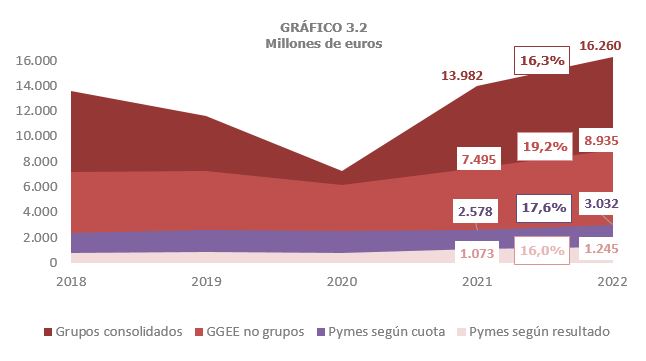

The Corporate Tax accrued increased by 21% ( Table 3.1 ), a rate similar to that estimated for the tax base. The increase in the tax accrued is over 5.3 billion, of which almost 4.35 billion correspond to the higher fractional payments, the main concept within the tax. Split payments grew by 17.3% ( Table 3.2 ), although the rate would reach 24.4% if the extraordinary income that occurred then is not taken into account in 2021. The favourable performance of the bases and the greater contribution of payments based on profits (minimum payment) were the cause of the strong growth in payments. Chart 3.2 shows the evolution by type of taxpayer. Payments by consolidated groups grew by 16.3% (35.7% excluding extraordinary items in 2021) thanks to the contribution of the minimum payment (2,943 million more than the previous year). In the case of Large Companies not belonging to groups, the increase in payments was 19.2%, 3 points less than in 2021, although that year was compared to the year of the pandemic. For their part, SMEs as a whole saw their payments increase by 17.1%. It should be noted that these companies can make the payment in installments according to the last annual installment submitted or according to the profits of the period. In the first group, the increase in payments in 2022 was 17.6% (1.2% in 2021, a year in which most payments were based on 2020), while in the second group the increase rose to 16%.

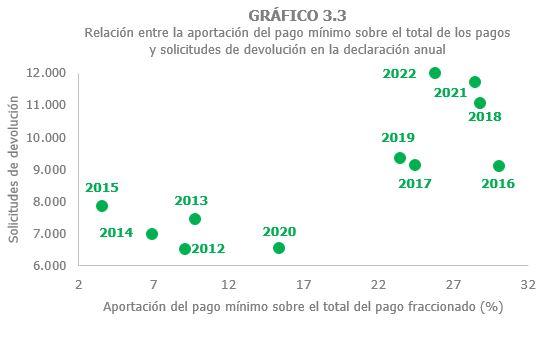

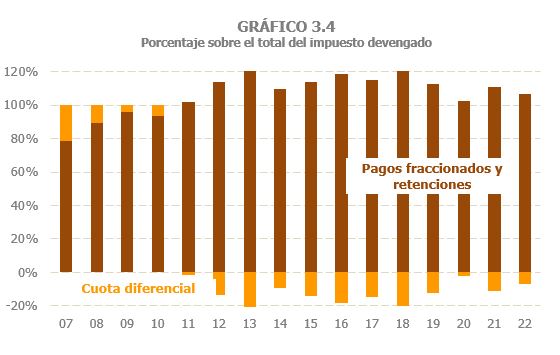

As regards the rest of the tax, it is worth noting that, as has happened in previous years, the behaviour of payments, and in particular of the minimum payment, with high incomes, conditions the evolution of the differential rate. Figures 3.3 and 3.4 illustrate this situation. The high percentage of income from minimum instalment payments (almost 26% of total payments in 2022) also implies a high amount of refund requests when the annual declaration is filed and, consequently, a negative differential rate. Figure 3.3 shows the relationship between the percentage of the minimum payment and refund requests, and Figure 3.4 shows its effect on the differential rate: Since the payment rates were raised in 2011 and, above all, since 2012 when this minimum payment was introduced, which depends on profits and not on the tax base, the differential rate has always been negative, unlike what happened previously ( Table 3.3 ).

Cash grew by % (Table 3.1) in line with the evolution of profits and bases in 2022 and 2021. The two concepts that most boosted tax collection were installment payments and income from the annual declaration.

The split payments, which are the main component of the tax and are linked to the profits of the year, grew by 17.7% and the increase would be even greater if the extraordinary income that occurred in 2021 is not taken into account.

For its part, annual tax return revenues grew by 41.7%. Revenues derived exclusively from the liquidation of the 2021 financial year rose by more than 45%, which is explained by the growth in profits in 2021 (36%). Part of these high rates are due to the poor results of 2020, but the figures for 2022 are also better than those recorded before the pandemic ( Table 3.1 ).

Revenue growth was limited by the increase in returns made (26.6%), which is due to three reasons ( Table 3.3 ): the increase in refund requests from the 2021 campaign, the acceleration in their execution, and the existence of extraordinary refunds due to rulings and the management of deferred tax assets (DTA).

Regarding the first point, it should be remembered that, in any given year, the refunds made in Corporate Tax combine two campaigns: In the first few months, most of the refunds requested in the previous year's campaign are paid (in 2022, those for the 2020 fiscal year), while in the final months, the amounts requested in the following campaign (in this case, 2021) begin to be returned. In 2022, the refunds made in the first months were around 2 billion euros lower than those of the previous year due to fewer applications in 2020, but, on the other hand, the refunds corresponding to 2021 practically doubled due to the increase in applications and the advance in the implementation schedule.