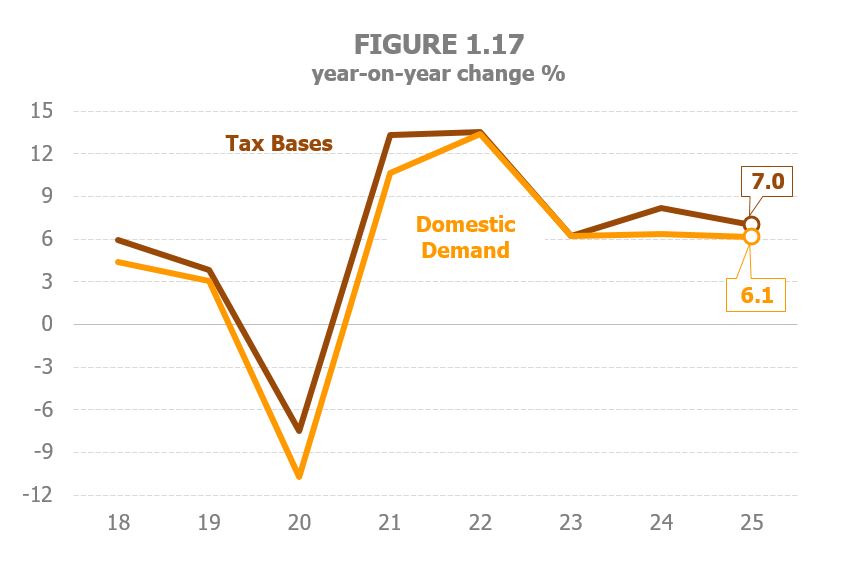

Tax bases

Main Tax Bases are estimated to have expanded by 7% in 2025, which translates into a moderation of just over one point compared to the rate achieved the previous year (Table 1.3). This marks, therefore, the third consecutive year with an average increase in the aggregate tax base of 7%. The same slowdown profile was spotted, as already seen, in the economic activity. GDP growth, both in real and nominal terms, moderated by just under one point compared with 2024. Domestic demand, a nominal variable more linked to the evolution of the aggregate tax base than GDP, also reflected this slower pace of growth, albeit to a lesser extent (the year closed with an increase just three tenth below 2024). Figure 1.17 shows the connection between the tax base and the estimated domestic demand as calculated by the National Accounting.

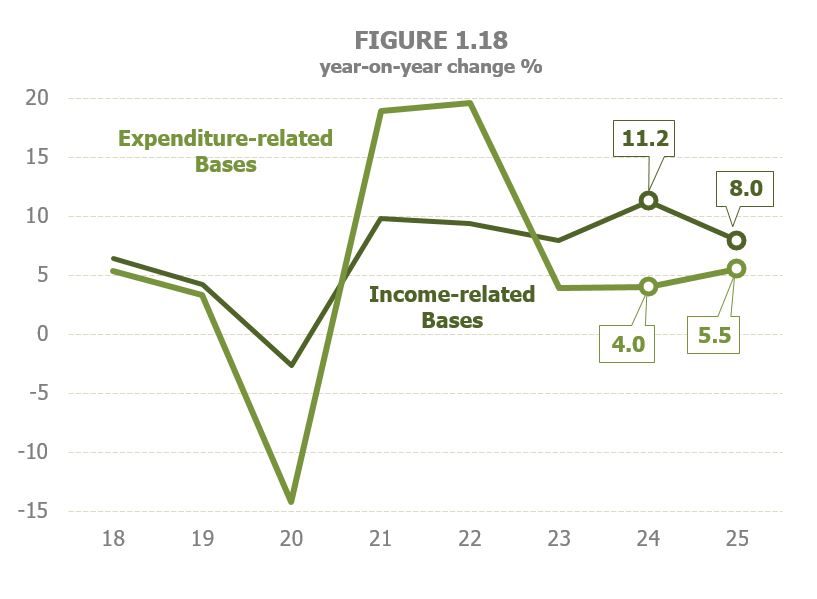

The lower increase in the aggregate tax base is due to the performance of income-related bases, that showed a slowing trend, stressed by the build-up in 2024 of large increases in income from movable capital and from economic activities.

Gross household income grew by 7.2%, 1.7 points below the 8.9% of 2024, while the Corporation tax base increased by 11.6%, a rate that, while high, is below the 23.1% reached a year earlier, a rebound driven by regulatory changes. In short, the aggregate tax base on income increased by 8%, which meant a slowdown of more than three points compared to 11.2% in 2024. On their side, expenditure-related bases grew by 5.5%, exceeding the previous year's figure by one and a half points (Figure 1.18). Final spending subject to VAT rose by 6.1%, compared to 5.7% in 2024, thanks to the slight increase in its volume component and with a practically stable deflator. The value of Consumptions subject to Excise Duties went back to positive rates, following two years of declines. The 1.4% increase was based on higher fuel and electricity consumption and higher prices for tobacco and electricity, in both cases amplified by rate hikes.

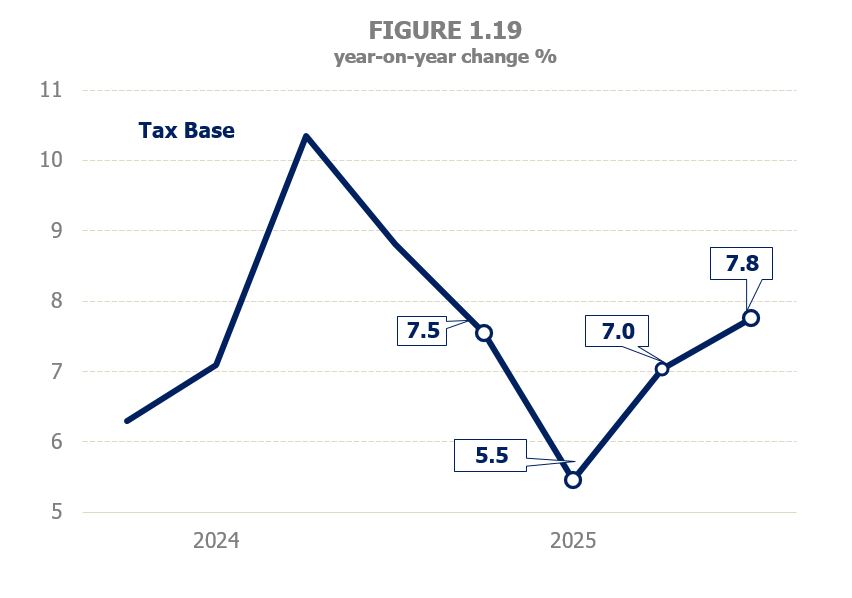

The aggregate tax base began the year with a clear downward trend (Figure 1.19). Up to June the increase was 6.5% compared to 9.6% in the previous semester, partly due to the strong rebound in the corporate income tax base in the second half of 2024. As of the middle of the year, on the other hand, the bases picked up, so that, between July and December, the base increased by 7.4%, with household incomes and the consolidated tax base of Corporate Income Tax remaining stable and larger growth in spending subject to VAT.