Accrued taxes and tax revenues

Accrued taxes enlarged by 10.2% in 2025 (Table 1.4), a rate similar to that of the sum of the main tax figures (10.1%, Table 1.3). The 10.2% expansion implies a slowdown of more than three points compared to the 13.4% reached in 2024. The slowdown is one point lower for accrued taxes when excluding the estimate outcome of the Personal and Corporation Income Tax annual return (10.8% in 2024 and 8.7% in 2025). The growth in accrued taxes was due to the 7% increase in the bases and an increase in the average tax rate of 2.9%.

The 10.4% increase in tax revenues slightly exceeded that of accrued taxes. Revenue growth in 2025 is explained by the increase of the tax bases and the positive impact of regulatory and management measures, quantified at €7.82 billion (Table 1.5 shows the breakdown), representing 2.7 points of revenue growth. The overall effect includes a negative impact of €2.98 billion from extraordinary receipts and refunds, and a positive impact of €10.8 billion that was mainly the result of the actions in the Corporate Income Tax, the return to normality in VAT and in taxes on electricity, new taxes (on the Interest and Charges Margin of certain Financial Entities and on Liquids for Electronic Cigarettes) and the increase in the rate in the Tobacco Excise Duty.

Analysing the evolution of bases and income by figures, in the PIT gross household incomes increased by 7.2% in 2025, down by almost two points compared to the 8.9% reached in 2024, but what points towards four years of increases averaging 7.9% (Table 2.1).

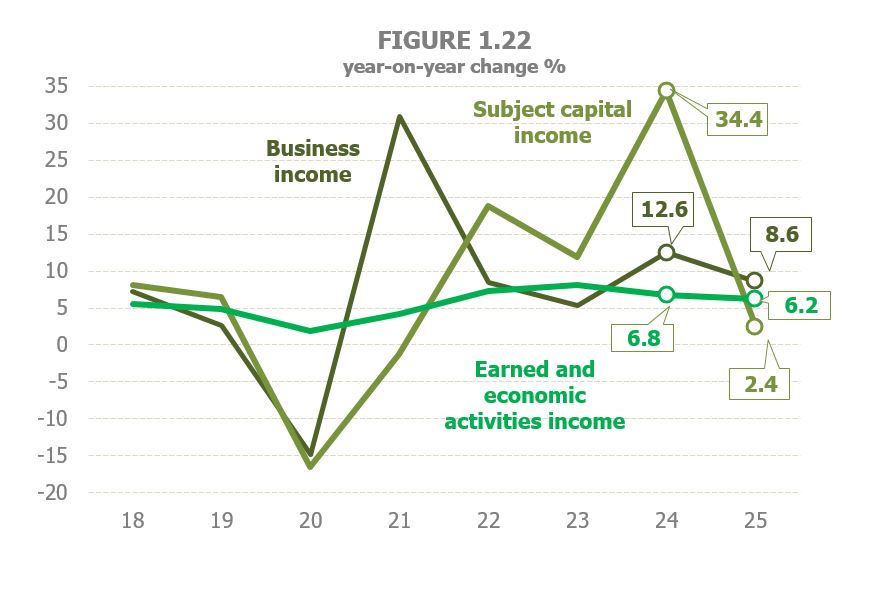

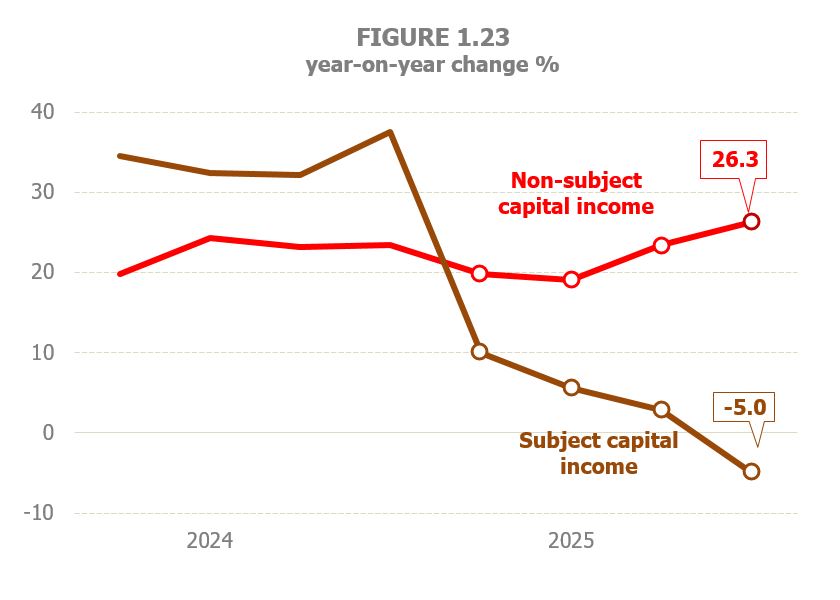

The loss of momentum affected all components of income subject to withholdings and instalment payments, being particularly marked in capital income subject, (Figure 1.22) subsequent to the strong dynamism they showed in 2024 due to the boost received at that time from income from movable capital and mutual investment funds. On the contrary, capital income not subject to withholdings is expected to continue to grow strongly, above 22% (Figure 1.23), driven by the development of non-subject capital gains, thanks to the positive evolution of real estate sales and the share price. A smaller slowdown in non-subject rental income (9.5% in 2025, 10.6% in the previous year) is also foreseen, mainly linked to housing rentals.

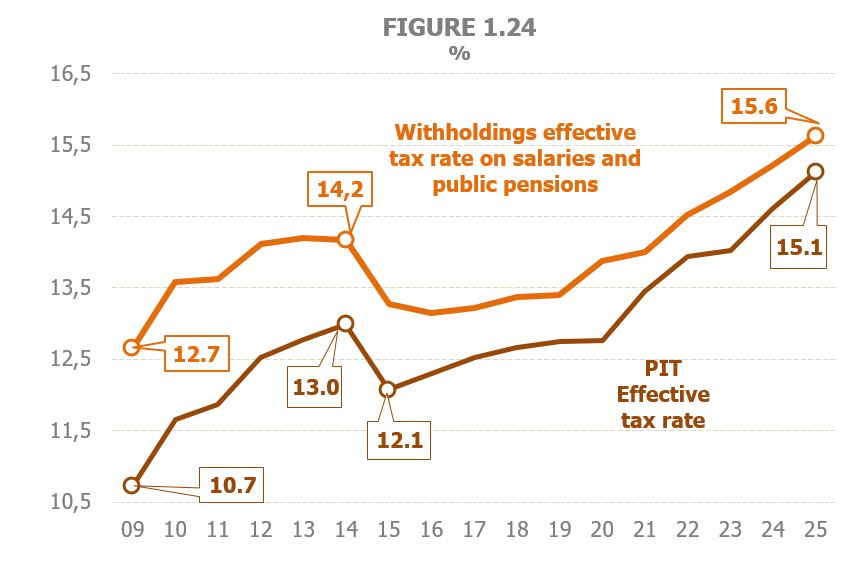

Accrued PIT once again showed significant progress in 2025, 10.9%, already marking five consecutive years of strong growth, above 11% on average, as a result of the good performance of income and the increase in the effective tax rate, which has enlarged by 3.5% on average annually between 2021 and 2025. Its evolution is clearly determined by that of the effective rate on public salaries and pensions (Figure 1.24), which has also grown significantly in recent years, pushed by rising average incomes. Excluding the outcome of the annual return, accrued PIT increased by 8.4% in 2025, as a result of the increase in the bases by 7.2% and the effective tax rate by 1.1% (Table 2.1).

PIT revenues grew by 10.1% in 2025, a high rate despite being negatively affected by regulatory and management changes that subtracted €1.15 billion from this tax figure’s collection (Table 1.5). The items that contributed the most to revenue growth were withholdings on earned income and the gross outcome of the annual return for the year 2024, entered in 2025.

As previously mentioned, the regulatory measures had a negative impact of €1.15 billion in 2025. The most relevant was certainly the one related to refunds to mutualists. These extraordinary refunds, following a judgment in their favour, were already being paid in previous years, especially in 2024, but in 2025, they received a new boost. A total of €2,717 million were paid, compared to €551 million in 2024, thus, in differential terms, the negative impact amounted to €2.17 billion. The rest of the measures touching the PIT had a positive effect of €1 billion. About €600 million are the result of the measures implemented to mitigate the effects of the dana at the end of October 2024, mainly the deferment of the second instalment payment of the annual return (the taxpayers of the province of Valencia were able to enter that second instalment, of about €300 million, in February 2025 instead of 5 November 2024, as customary). The remaining €412 million include, as the most notable measures with a positive impact, the adjustment of the annual return outcome due to changes in the general reduction for earned income and the changes in the percentage of reduction in rentals of properties intended to housing (that went from 60% to 50%, although 60% is maintained for contracts in force, and increased to 70% or 90% for certain types of contracts), and, with a negative impact, the increase in the deduction on donations (the level of the first bracket of the deduction base was enlarged, the general applicable percentage of deduction was increased and the number of years to apply the increased percentage was reduced) and the changes introduced by the Regional Governments in the autonomous bracket (mostly changes in the exempt minimum and rates, partially offset by the withdrawal of some temporary deductions).

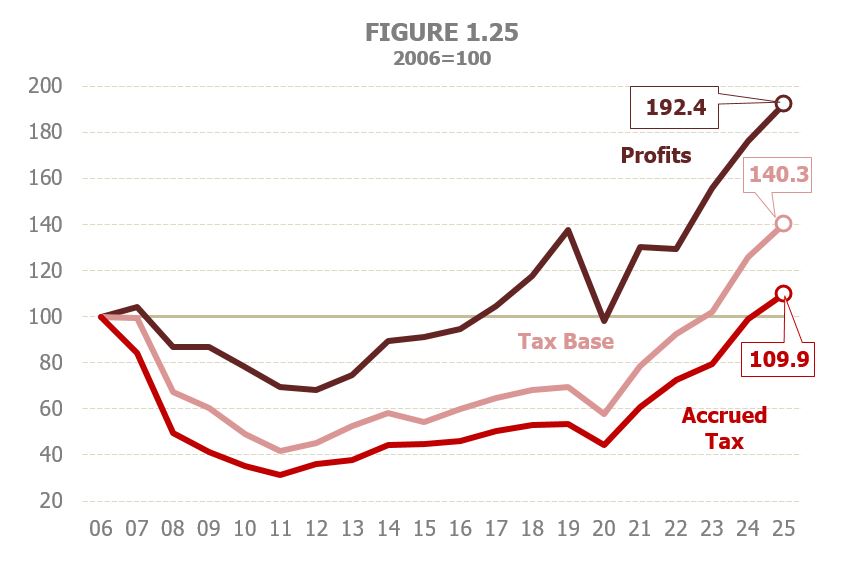

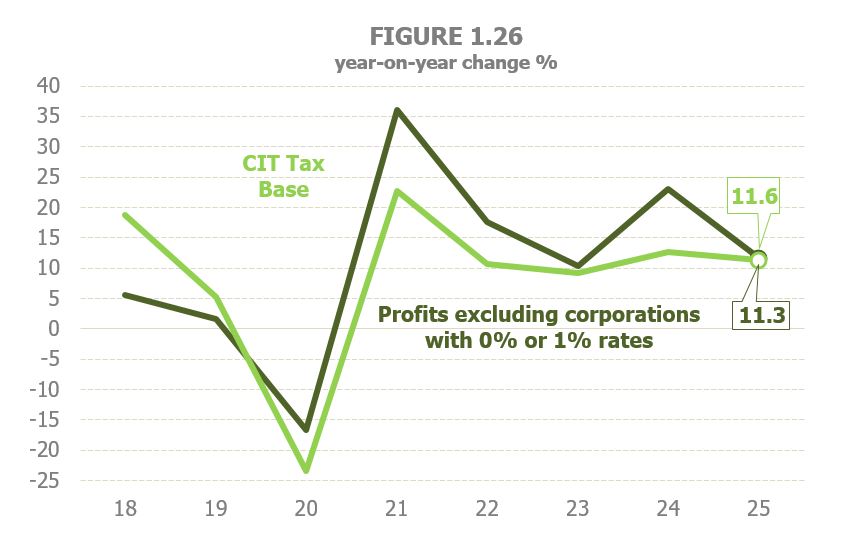

The Consolidated Corporate Income Tax base surged by 11.6% in 2025 (Table 3.1), also chaining five years of strong increases. This positive evolution of the tax base has meant that every year since 2023 the previous historical high of 2006 has been exceeded, although this result has not been fully transferred to the accrued tax, which in 2025, for the first time, exceeded the level reached that year (Figure 1.25). The evolution of the tax base is fairly similar to that of corporate profits, excluding those with 0% and 1% tax rates. The change in the double taxation regulation in 2021 reduced the quantity of these adjustments in the consolidated groups, favouring a gradual rapprochement of the tax base to these benefits (Figure 1.26 and Table 8.5). Profits (excluding corporations with 0% and 1% rates) are estimated to have grown by 11.3% in 2025, above what profits reported by Large Corporations and Groups in their instalment payments showed (6.1%, Table 3.2).

Accrued Corporate Income Tax is forecasted to have increased by 11.2% in 2025, a rate slightly lower than that of the tax base, due to the minimal reduction in the effective rate. The good performance of the accrued tax is supported by the increase in instalment payments and by the outcome of the annual return, for which a net positive result is expected for the first time since 2010.

Corporate Income Tax revenue grew by 8.1% (Table 3.1), hitting €42.27 billion. The surge is shaped by regulatory and management changes that added €3.64 billion to revenue. As in the PIT, there is a downside due to extraordinary receipts and refunds, €713 million, of which €463 million come from the ruling on RDL 3/2016 that overturned the limitations to the compensation of negative bases and, therefore, led to extraordinary refunds for the previous non-prescribed years. In particular, in this latter case, €1.43 billion were refunded in 2025 and €879 million in 2024. Besides this impact, the measures that have had the greatest effect were those enclosed in Law 7/2024, applicable to the 2024 annual return and to the 2025 instalment payments. Firstly, the limit of 50% to the consolidation of the losses of the companies belonging to groups. The measure was in force in 2023 with an impact on the instalment payments of that year and, residually, on the annual return submitted in 2024. With the endorsement of the measure for the years 2024 and 2025, there is a full impact on the 2024 annual return, submitted from July 2025 (in differential terms, €1.48 billion), and on the instalment payments of that year (€1.47 billion). Secondly, the recovery of the limits to the carry-forward of negative tax bases of previous periods for companies with a turnover of more than €20 million. In 2023, because of the ruling that overturned RDL 3/2016, these limits were the general ones, what translated into a loss of revenue. Law 7/2024 restores it to the previous situation. Because of the way the impact is estimated, this recovery is treated as a reversal of the loss of the previous year and the same amount with opposite sign is estimated (€1.7 billion). And, thirdly, the rise of the applicable percentage (from 10% to 15%) to the decrease of the tax base due to the capitalisation reserve and the reduction of the period for the maintenance of own funds increase and for the unavailability of the reserve. This measure is estimated to have a negative impact on revenues of €324 million.

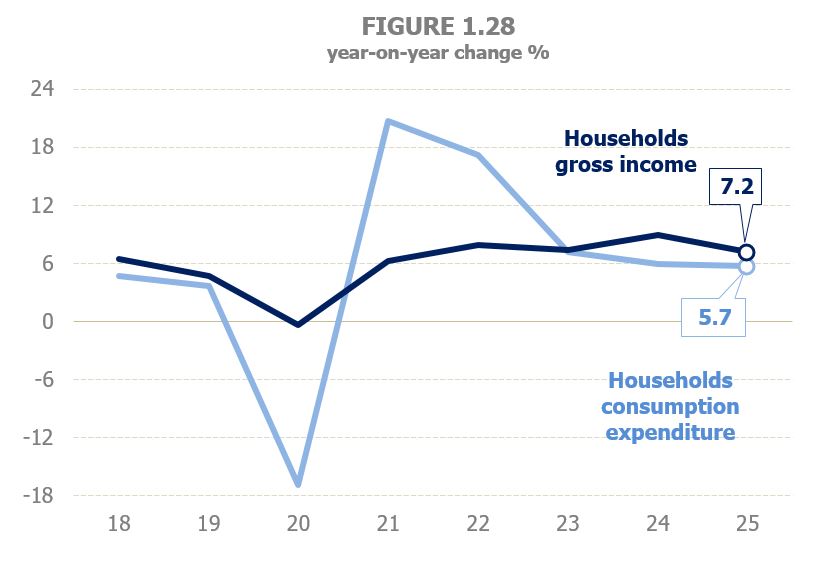

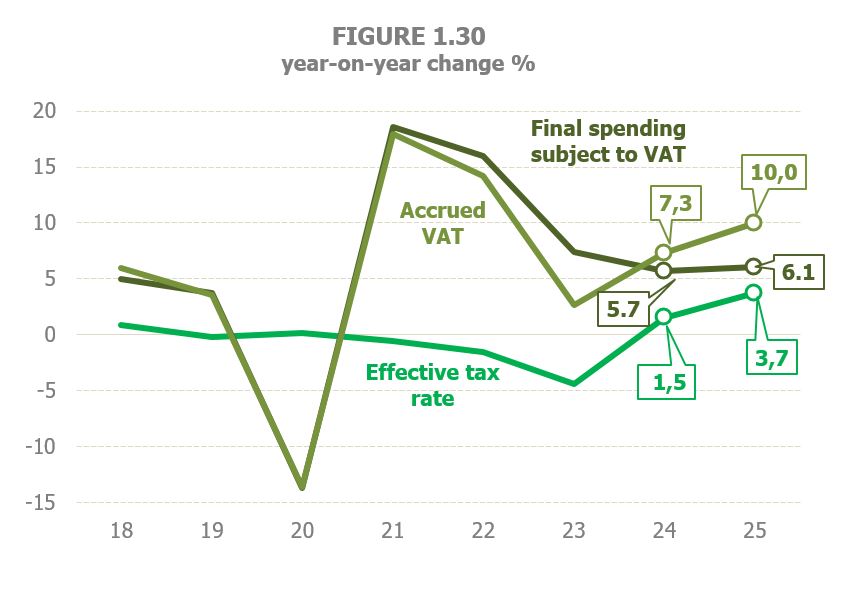

As for VAT, final spending subject to this tax grew by 6.1% (5.7% in 2024, Table 4.1), thanks to the slight increase in its volume component and with a practically stable deflator. Expenditure of households, the main component of final spending subject to VAT, showed a slight slowdown in its growth rate (5.7% compared to the previous 6% in 2024), lower than that estimated for household gross income (Figure 1.28). The largest increase in total expenditure was due to the more positive evolution of its other two components. Thus, current and capital expenditure of Public Administrations increased by 6.9% in 2025 (3.2% in 2024) and household’s expenditure on new housing by 9.7% (7.4% formerly).

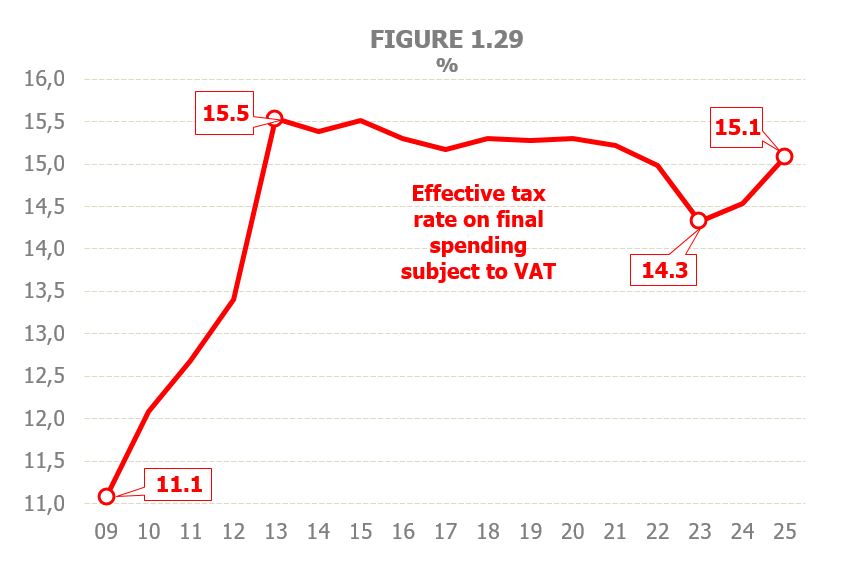

The increase in rates on energy products and food staples triggered an increase in the average rate estimated at 3.7 points, thus returning to a level similar to that seen prior to the successive cuts implemented since 2020 (Figure 1.29). Accrued VAT increased by 10% in the year, driven by the rate hikes and exceeding by almost three points the estimated rate for 2024 despite the humble increase in spending (Figure 1.30). Net accrued VAT recorded a similar rise.

VAT revenue grew by 9.9% in 2025 (7.9% previously, Table 4.2), thanks to the increase of rates, the same as accrued VAT. In 2025, from 1 January, rates applied to VAT were those applicable before the different measures that had been taken since mid-2021; that is, the rate of 21% on electricity and natural gas and the rate of 4% on basic food staples.

The return to these rates was made progressively during 2024, in the case of gas definitively from the very first months, in that of electricity non-regularly, depending on the prices in force in each month and, in the case of food staples, since October with an intermediate step between that month and December (2% and 7.5% rates). In addition, given the lag between the time the tax is due and the time the cash receipts are entered, the full impact of the recovery of the rates is spread over three years, 2024, 2025 and 2026. The share matching 2025 amounts to €562 million in energy products (compared with the initial months of 2024 and those in which electricity prices were high and, therefore, the reduced rate was maintained) and €2 billion in food staples (comparing the standard rates of 2025 with the reduced rates applied in most of 2024 and the intermediate ones of the month of October, entered in December). The total impact on VAT, including also extraordinary revenues and refunds and other minor measures, was €2.22 billion.

The value of consumption subject to Excise Duties grew by 1.4% following two years of declines (Table 1.3). This trend reversal is driven by the higher value of those consumptions with the greatest weight in the aggregate, as electricity (6.1%) and tobacco (1.5%) due to higher prices and, only in the case of electricity, also to higher consumption. The value of consumptions of hydrocarbons went on the opposite direction (-1.9%), dragged down by falling prices (Table 9.1), and by the value of alcohol and beer, due to lower consumption.

In 2025 revenue from Excise Duties grew by 4.3%, up to €23.08 billion, driven by the impact of regulatory changes. Regulatory measures brought in revenues of €831 million. There were three measures to bear in mind. Firstly, the full recovery of the rate on the Electricity Excise Duty. Similar to what happened in VAT, the return from 0.5% in force since September 2021 to 5.11% took place gradually in 2024, closing from July. The comparison of 2025, already a full year with the standard rate, and the half-year of 2024 in which the rate was approaching that level, results in an impact of €436 million. Secondly, the increase in rates on the Tobacco Excise Duty with effect from 1 January 2025. In the case of the most widely consumed product, cigarettes, the increase meant going from a fixed rate of €0.47 per package to €0.69 and from a proportional rate of 51% to 48.5%. The impact is estimated at €365 million during the first eleven months of the measure (the effect in December has been seen in January 2026). And, thirdly, the new Tax on Liquids for Electronic Cigarettes that, as said, collected €30 million euros since the first receipts in April. When the additional revenue provided by theses regulatory changes is subtracted, the increase in Excise Duty would stand at 0.6%.

Hydrocarbons Excise Duty, the weightiest item (Table 5.5), grew by just 0.5%, up to €12.37 billion, thanks to a higher consumption (2%), specially of gasoline and reduced-rate diesel and biofuels, while diesel-oil and natural gas not used as fuel in vehicles declined.

Tobacco Excise Duty receipts increased by 6%, amounting to €7.34 billion (Table 5.6) thanks to the rake hike in force since 1 January and despite the fall of consumption (-4.5%) accounted for both by the price rises and the hoarding ahead of the rate hikes at the end of 2024. The Tax on Liquids for Electronic Cigarettes collected €30 million in its first year.

The Electricity Excise Duty (Table 5.7) grew by 42.8% as the 5.11% rate recovered in July 2024 was in force throughout the entire period. The outcome is a record-breaking collection of €1.59 billion, above the 2012 peak (€1.51 billion). In addition to the tax rate, higher consumption and higher prices before taxes, also played a role on the increase.

Receipts from taxes on alcohol decreased by 3.4% dragged down by consumptions. The fall was more intense, by 3.8% (Table 5.2) in the case of Alcohol and alcoholic beverages Excise Duty, the one that taxes beverages with a higher alcohol content, while the Beer Excise Duty recorded a 2.8% drop (Table 5.3).

The Tax on Non-Reusable Plastic Packaging collected €599 million, 4.8% more than in 2024.

Regarding other tax figures, the Non-Resident Income Tax (Table 6.1) collection in 2025 went up by 33.8%, marking five consecutive years of growth and surpassing the amount of €5 billion. This strong growth is underpinned by both, the positive performance of withholdings and payments on account and the higher collection of the annual return, boosted by an extraordinary receipt and by the positive developments of the annual settlements accrued in 2024 and cashed in 2025.

Revenue in the ‘Other Receipts’ from Chapter I increased exceptionally in 2025, influenced by two elements. On the one hand, the debut in 2025 of the new Tax on the Interest and Charges Margin of certain Financial Entities, which involved revenues of €1.42 billion. This tax, that replaced the Special Levy (non-tax revenue), in force in 2023 and 2024, although managed by the Spanish Tax Agency, is assigned to the Autonomous Communities.However, the impact on revenue of this assignment will be visible from 2026. On the other hand, the Tax on the Electricity Production Value also made a significant contribution to the increase in collection, adding €924 million more than in 2024 (Table 6.2), mostly (€807 million) due to the full recovery of the tax, fully standardized in 2025 following the gradual recovery in 2024 after its suspension in 2021.

As for the rest of the concepts included in Chapter II, it is worth noting the performance of its two main components: The Tax on Insurance Premiums, that grew by 7.9% following the already sharp increase of 9.1% in 2024 (Table 1.6 and Table 6.4), and the Tax on Foreign Trade, which increased by 13.3% after two years of drops (Table 6.3). The trend of the Tax on Financial transactions also was quite positive, growing by 36.5% and adding more than €90 million to collection. On its side, the Tax on Digital Services expanded by 9.2%.

Chapter III receipts, Fees and other revenues, (Table 1.6 and Table 6.6) grew by 7% (€141 million more than in 2024). As for fees, all the growth was due to the Canon for the use of continental waters (€182 million more than in 2024), that made up for the loss of revenue (more than €100 million in the Public Radioelectric Domain Fee due to a legal dispute with the administration by some operators.