3. Corporate Income Tax

In 2025 the CIT collected €42.27 billion, 8.1% more than the previous year (Table 3.1). In 2025, regulatory changes took centre stage, adding €3.64 billion to collection (Table 1.5), specially driven by those set out in the Law 7/2024, applicable to the 2024 annual return, most of which was paid in 2025, and to the 2025 instalment payments. The two measures with the greatest impact were the limit to the consolidation of the losses of the companies belonging to groups (in force in 2025 instalment payments, but not in 2024 instalment payments) and the recovery of the limits on the carry-forward of negative tax bases of previous periods for companies with a turnover of more than €20 million. In addition, it must be noted that revenue was negatively affected by the strong growth of refunds from other periods, such as those resulting from the refund requests matching the fiscal year 2023 (of a large sum that were completed at the beginning of 2025) and the extraordinary ones related to the court ruling on RDL 3/2016.

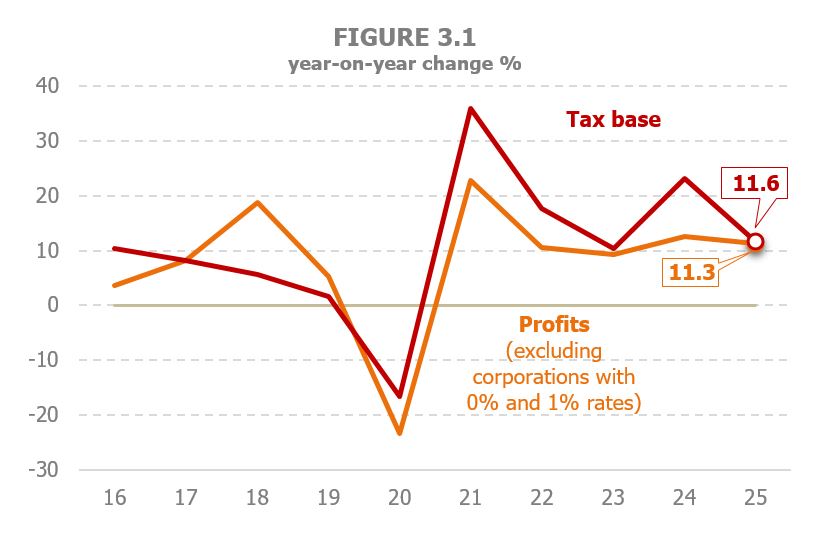

Corporation profits growth in 2025 (excluding those with 0% or 1% rates) is estimated at 11.3%, marking five consecutive years with an average increase above 13%. The rise was lower for profits reported by Large Corporations and Groups in their instalment payments, 6.1% (7.5% in Large Corporations not integrated in groups and 5.1% in Groups; Table 3.2 ).

Instalment payments, the main constituent of the tax, increased by 8.1% as a result of the trend in profits and the boost provided by regulatory changes. Out of the €3.17 billion additional collection in 2025, €3.07 billion come from the instalment payments. Withholdings on capital income amounted to around €260 million additional receipts, a far distant figure from the more than €860 million recorded in 2024, thanks to the aforementioned upturn in withholdings on movable capital income and the sharp increase of withholdings on mutual investment funds. The contribution of the outcome of the annual return (that of fiscal year 2024) was also positive by almost €560 million. Revenue rose by 16.9%, partly driven by regulatory changes, although refunds also increased significantly, as a big share of those requested in 2024, matching the fiscal year 2023, were paid in 2025 (Table 3.3). On the contrary, the payment of a larger amount of extraordinary refunds and the lower receipts from tax assessments made by the Administration, subtracted almost €770 million from the collection.

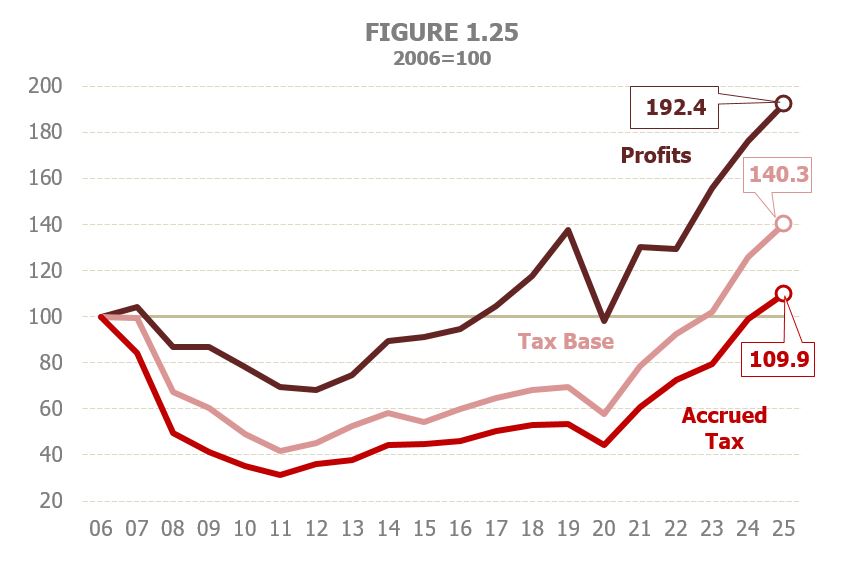

The consolidated Corporate Income Tax base surged by 11.6% in 2025, a rate that, although high, embodies a significant moderation compared to the 23.1% recorded in 2024, favoured by the regulatory changes at the time (50% limit to the consolidation of losses in Groups and the recovery of the limits on the off-set of negative tax bases from previous periods). This tax base has shown an average increase in the last five years close to 20% surpassing the already positive trend in profits (Table 3.1 and Figure 3.1). 2025 has once again set an all-time high in terms of the tax base, surpassing the 2023 figure, the year when the previous record set in 2006 was beaten for the first time. Furthermore, it is expected that the accrued tax will also exceed, for the first time, the peak recorded at that time (Figure 1.25). The detailed trend of the tax since 1995 is shown in Table 8.5.

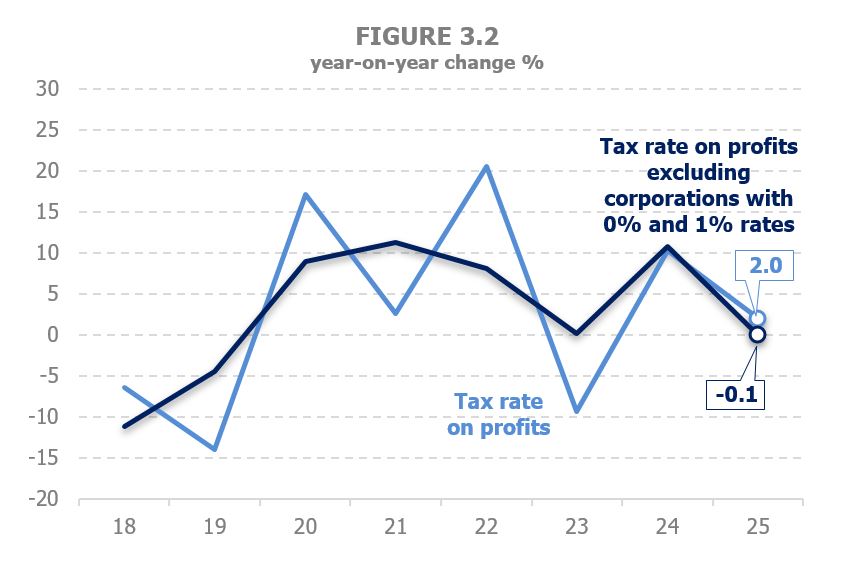

The effective tax rate on the tax base is expected to decrease slightly in 2025 (-0,3%) following a 1.3% increase in 2024, driven by the impact of regulatory changes (Figure 3.5). The changing incidence of regulatory changes over the last five years, when the progress of the tax base has been quite notable, has resulted in a moderate increase (0.4%) of the average rate in the period 2021-2025. The tax rate on profits, excluding corporations with 0% or 1% rates, is estimated to remain virtually stable in 2025 (-0.1%). The calculation of the tax rate does not include this type of corporations, mostly financial entities, due to the wide variability of their profits, linked to the valuation of their assets, that, in turn, depends on changes on interest rates and on responses of financial markets. This has a significant impact on profit fluctuations and, consequently, on changes on the tax rate (Figure 3.2), although it has little or no effect on the tax itself given their low or null taxation.

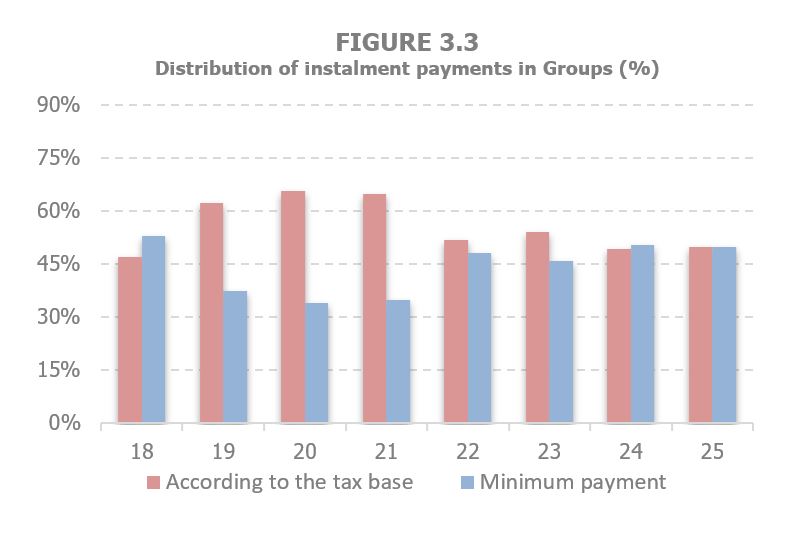

Accrued Corporate Income Tax is estimated to increase by 11.2% in 2025 (7.9% without taking into consideration the due tax of the annual return), thanks to a 7.7% increase of instalment payments and the expected favourable outcome of the annual return. In the case of consolidated Groups, the increase in the instalment payments stood at 7.5%, with a stronger growth in those declaring according to the taxable base (8.7%) than for those that do so on the minimum payment (6.3%). The presence of regulatory measures (the limitation to 50% to the off-set of losses in the consolidation of the companies belonging to the group) explains why the progress of these payments was larger than the increase in profits (estimated at 5.1%). What has been unusual this year is the irregular trend of the three instalment payments, with a large increase of the first, an adjustment in the second due to the slowdown of profit in the central part of the year and a recovery at the end of the year. In Large Non-Group Corporations, instalment payments increased by 5.4%. In the case of these corporations the increase tends to concentrate mainly in those payments performed according to the tax base, unlike in Groups where the minimum payment, calculated on the basis of profits, is very relevant. The different pattern is clearly shown by Figures 3.3 and 3.4. As for SMEs, growth reached a rate of 14%, with strong increases both in those that were taxed according to their last annual return (11.7%), and in companies that declared according to the profits of the year (21.1%).

Tax revenue in terms of cash grew by 8.1% (Table 3.1), in line with the performance of the instalment payments. Both, withholdings on movable capital and those on mutual investment funds increased at a steady pace (7.0% and 12.2% respectively), albeit in sharp decline following the figures recorded in the previous year. The progress of the withholdings on leases was somewhat lower, as was the slowdown compared with 2024 (5.4% in 2025, 5.7% previously).

The outcome of the annual return matching the settlement of the fiscal year 2024 added almost €560 million to the collection, as a result of the increase of gross receipts (16.9%), boosted both by the good performance of profits and by the regulatory changes (Table 3.3). The refunds paid also exceeded those in 2024, although it must be borne in mind that these combine refunds requests matching two fiscal years, those of 2024 and those of 2023, in addition to the extraordinary ones. The former dropped by 4.9%, as the same regulatory changes that favour the increase of positive net outcomes, imply a lesser increase of refund requests. On the contrary, the latter, those matching 2023, paid in the first months of 2025, involved large sums in line with the requests for that fiscal year. Finally, it must be added the extraordinary refunds stemming from the judgement that overturned RDL 3/2016. The final result of all these was an increase in the total refunds paid as of the outcome of the annual return.