Information note 3. The recent evolution of the result of the personal income tax return

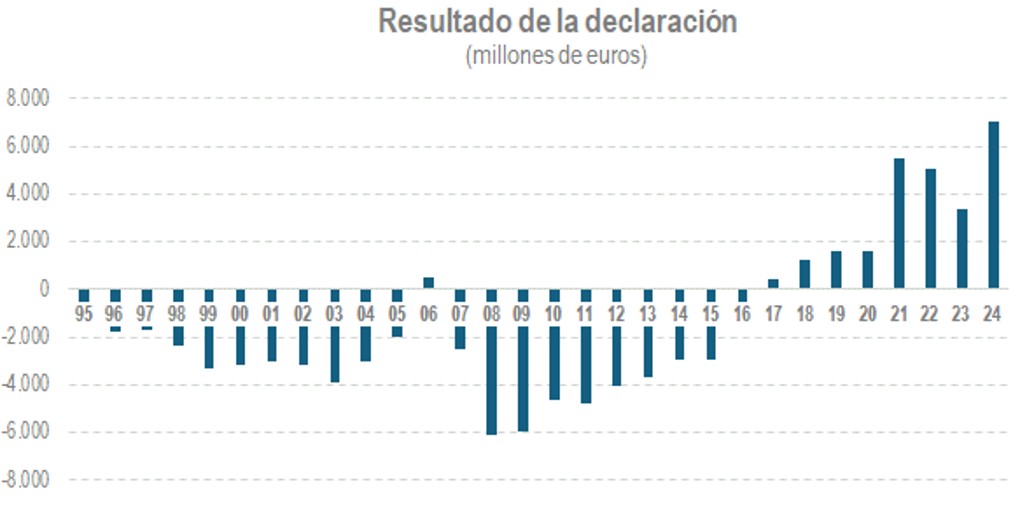

One of the most striking facts in the evolution of PIT It is the growing trend in recent years of the result of the annual declaration that, throughout the 30 years covered by the database of the Annual Tax Collection Report (IART), went from being consistently negative to becoming positive since 2017 and registering high amounts from 2021 onwards. The following graph, prepared from Table 8.2 of IART, reflects that trajectory:

It must be clarified, first of all, that in a tax like the PIT In a system where income of very diverse types is declared, which is progressive, which adapts to the personal and family conditions of taxpayers, and which is influenced by multiple regulations, the causes of any change in habitual behavior cannot be singular. All these aspects are even more relevant in this case because what is being analyzed is the result of the declaration, a balance whose sign alone says nothing about the overall performance of the tax. It is only the result of the tax settlement, the difference between the amount due and what has already been paid, it is not the full tax.

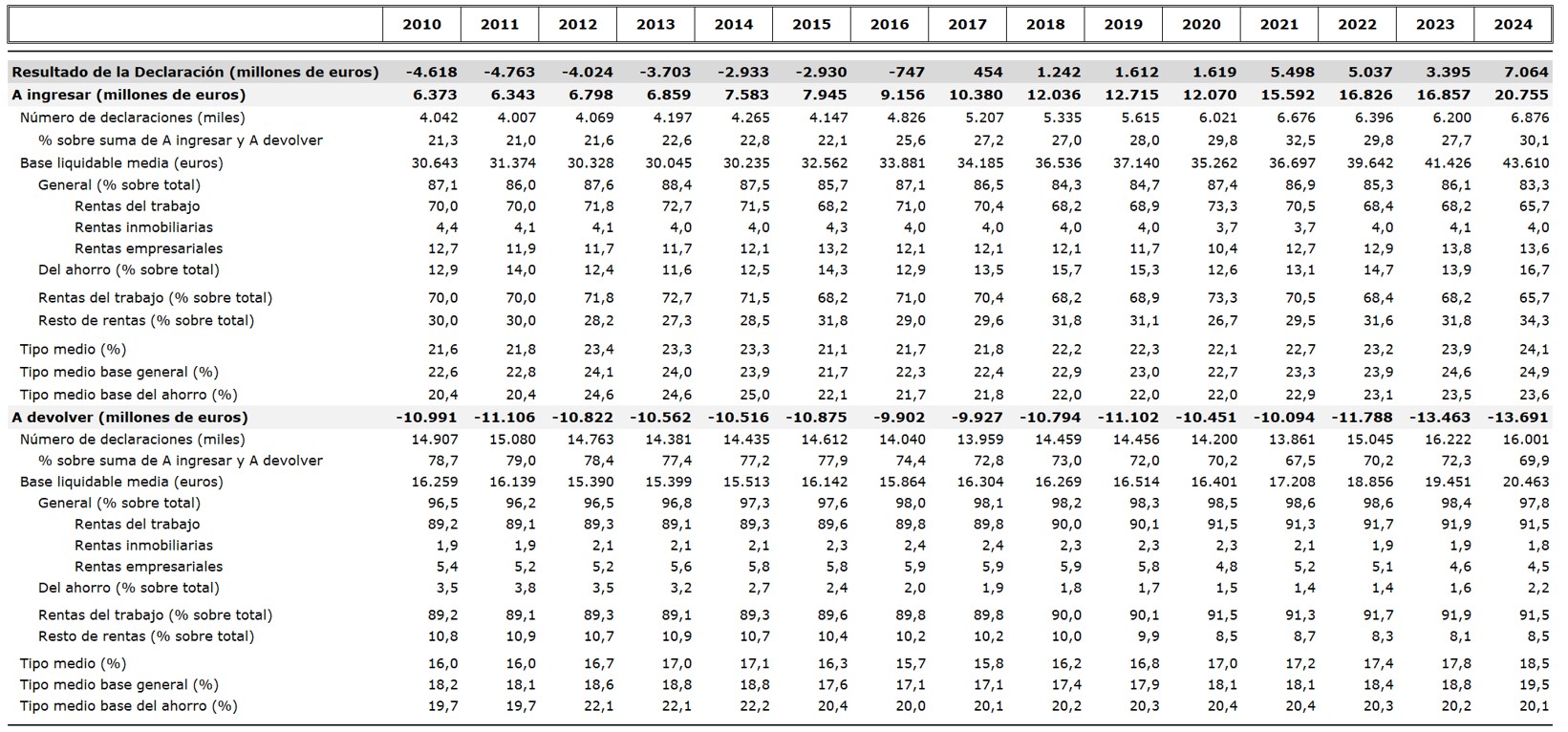

It is precisely this liquidation character that makes the result very sensitive to the variation of certain incomes. Thus, in recent years the evolution has been greatly influenced by the behavior of income that is not fully subject to the withholding system or fractional payments, such as, for the most part, capital gains and income from real estate capital and, to a lesser extent, income from economic activities and, for the higher income brackets, income from movable capital. As can be seen in Table 8.2 of IARTBetween 2020 and 2024, the reduced net returns from these incomes, the part that makes up the taxable base, grew by 70.4%, compared to the 32.8% increase in the same period for income from employment (salaries, pensions and unemployment benefits), which can be considered the only ones that are fully subject to withholding. This note examines, based on the separate analysis of tax returns to be paid and refunded, how this different growth of the various incomes has influenced the evolution of the result of the tax return.

The table at the end of the note presents several indicators that allow you to see the differences between the declarations to be entered and returned. In the period 2021-2024 the average result was around 5.25 billion, which contrasts with the just over 1.6 billion in 2019 and 2020. The increase between these two figures of approximately 4.8 billion is due to higher income from tax returns with a positive balance, partially offset by the increase in refund requests during the same period. The higher income means having positive balances that are 27% higher in the last four years than in the previous two.

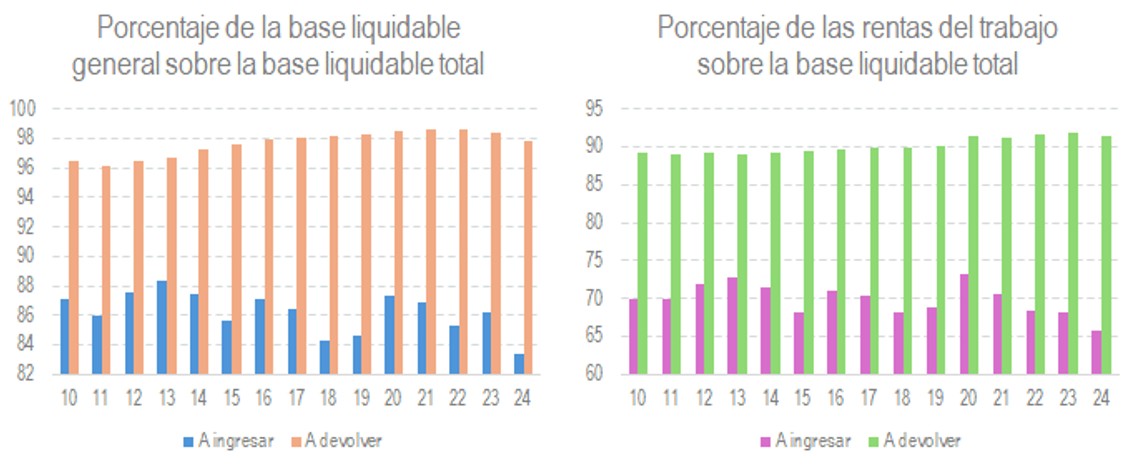

When analyzing separately the declarations to be paid and refunded, the most notable feature is the different origin of their income. The following graphs clearly illustrate this idea:

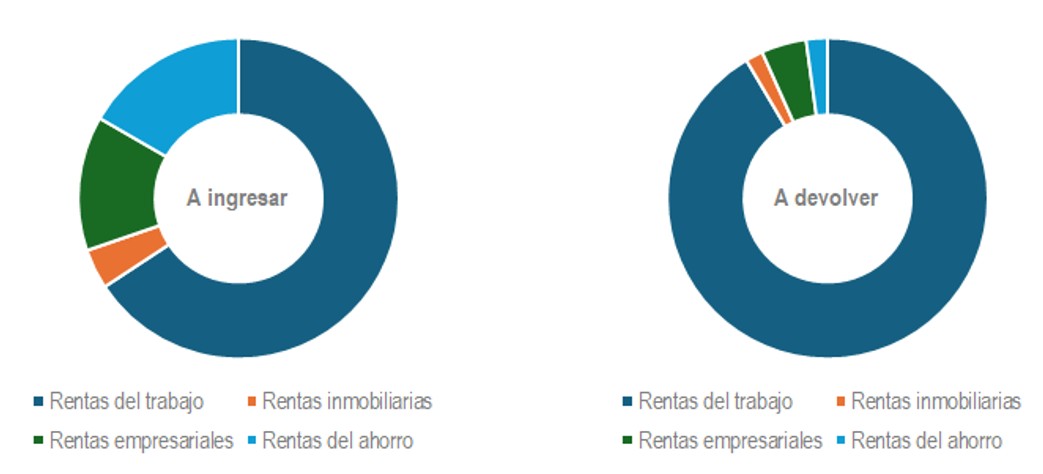

The chart on the left shows the percentage that the general taxable base represents in relation to the total taxable base. As can be seen, in the tax returns, practically the entire base is general with only a small contribution from the savings base, which is where almost all income derived from movable capital and capital gains is concentrated. In the declarations to be paid, on the other hand, the savings base meant more than 11% in all years since 2010 and more than 14.5% in the last four. Within the taxable base, the largest source of income is employment income; therefore, the result shown in the graph on the right, which displays the percentage of employment income relative to the total taxable base for both groups of tax returns, is not surprising: In tax returns with refunds, that percentage is around 90%, with an increasing trend, while in tax returns with payments due, that percentage is around 70%, although in recent years it has been below that figure due to the increase in other income. A more detailed breakdown can be seen in the following charts with data for 2024:

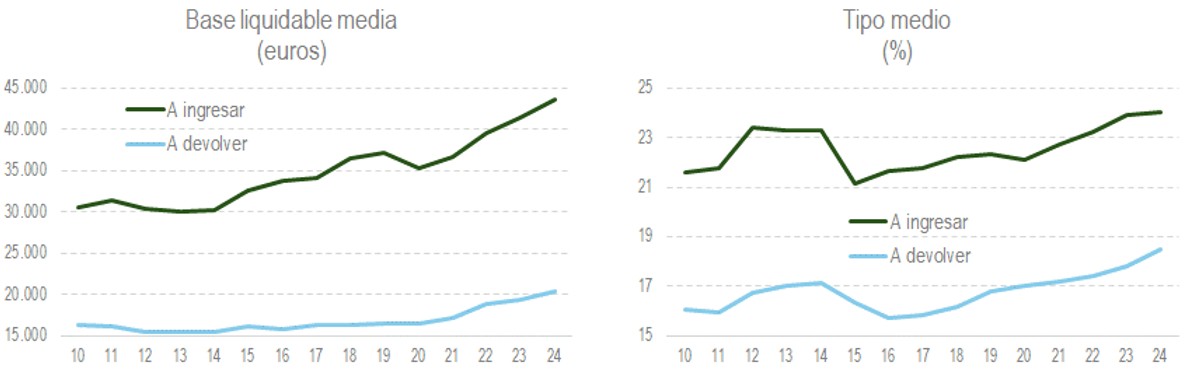

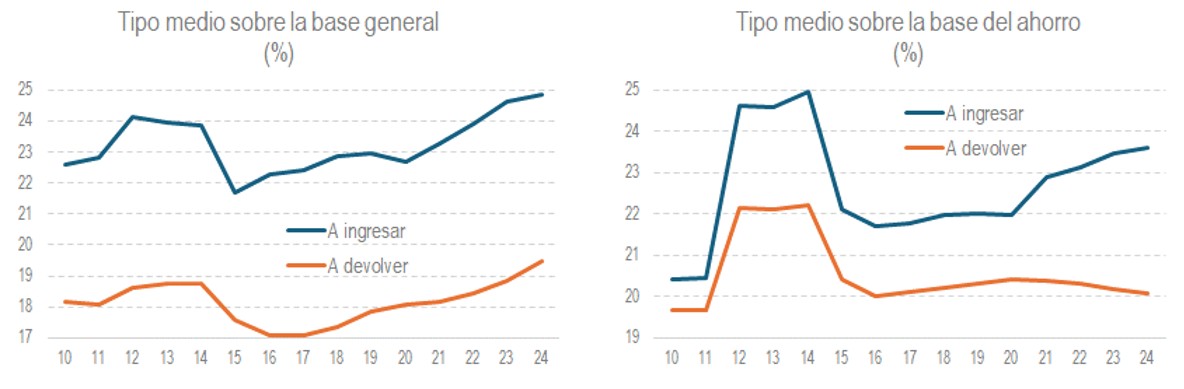

The differences between taxpayers occur not only in the origin of income, but also in the level of the taxable base and, consequently, in the average rates:

For the purposes of this analysis, it is useful to distinguish between the evolution of the rates applied on a general basis and those applied on a savings basis:

The general rate increases for both types of taxpayers, but there is a key difference. The increase in the general rate does not necessarily result in a larger positive balance or a smaller negative balance because income may be subject to withholding and this may already reflect that increase, so there would be no effect on the result of the annual declaration. This is what happens in tax returns where practically the entire general base comes from work and is therefore subject to withholdings. However, this general base also includes income from real estate capital and business activities that are subject to withholdings or payments on account only partially. These incomes have a significant weight in the tax returns, and through this channel there is indeed an impact of the rate increase on the result of their return.

In the case of the savings base, that effect is clearer. In recent years, tax rate increases for higher incomes have come into effect. As seen in the graph on the right, these increases affected income earners, which is where the highest incomes are. Furthermore, these rising rates are the ones that affect incomes with high growth since 2020 and which are mostly not subject to withholding tax, and if they are, they are subject to the minimum rate of 19%, well below the average rate.

From all of the above, it can be concluded that for the profile of taxpayers whose returns have a result to be paid, characterized by having a significant percentage of income not subject to withholding, the high growth of the latter and the rise in the rates explain why the amounts to be paid grew, this being one of the causes of the growing trend observed in the result of the return.