Information note 4. The evolution of the allocation to the Catholic Church for social purposes

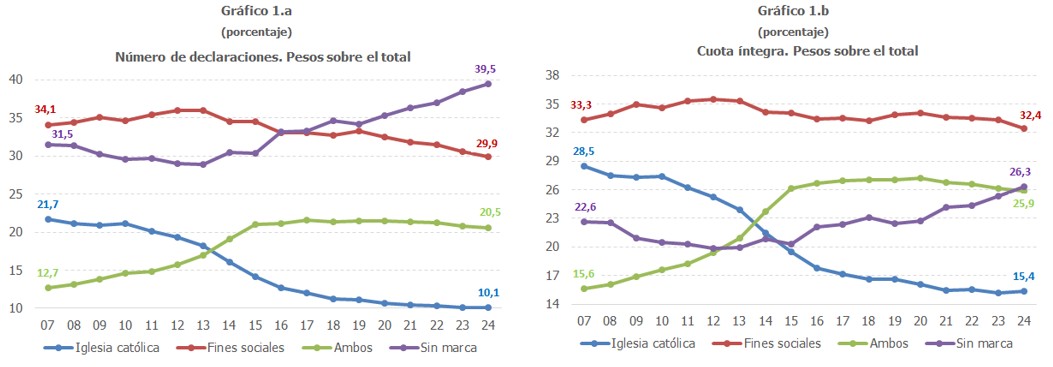

Following the approval of Law 42/2006 on the General State Budget for 2007, in the declaration of PIT Taxpayers can allocate 0.7% of their total tax liability to the support of the Catholic Church, to activities considered to be of social interest, or to both, by checking the corresponding box. The following set of graphs shows the evolution of the weight of each of the available options, both in terms of the number of declarations and the total amount of the fee1.

It is observed that, both in terms of the number of declarations and in terms of the total tax liability, the option of leaving the 0.7% allocation box unmarked has been gaining weight over the eighteen years that the rule has been in force, a trend that has become more evident since the 2015 tax year, so that in 2024, the last tax year for which information is available, the majority of declarations, 39.5%, chose the Unmarked option, which corresponds to 26.3% of the total tax liability.

It is also worth noting that, in terms of the total quota, the majority option has always been to allocate 0.7% to the support of activities considered to be of social interest (hereinafter social purposes), an option that has also had a fairly stable weight throughout the analyzed period. Thus, the initial weight in 2007 was 33.3% and grew until reaching its maximum in 2012, at 35.5%, before beginning a downward pattern that has become more evident since 2020, ending at 32.4% in 2024. In terms of the number of declarations, the loss of relevance of this option is much more evident, going from being the majority choice in 2007, to occupying second place from the 2017 fiscal year onwards and representing 29.9% of the total in 2024.

Meanwhile, the allocation to the Catholic Church shows a clear downward trend throughout the period, going from being the second most chosen option by the declarants of PIT in terms of total tax liability (the third largest in terms of the number of declarations), with a weight of 28.5% of the total tax liability in 2007, to being the minority option (between the years 2013 and 2015), its weight on the total tax liability being 15.4% in 2024 and representing only 10.1% of the number of declarations. The option to check both boxes on the declaration has followed a contrary trajectory, both from the perspective of the number of declarations and from that of the weight on the total quota. This alternative started as the least chosen in 2007, and gradually gained weight until 2020, the year from which it has gradually lost relevance, in favor of the Unbranded option.

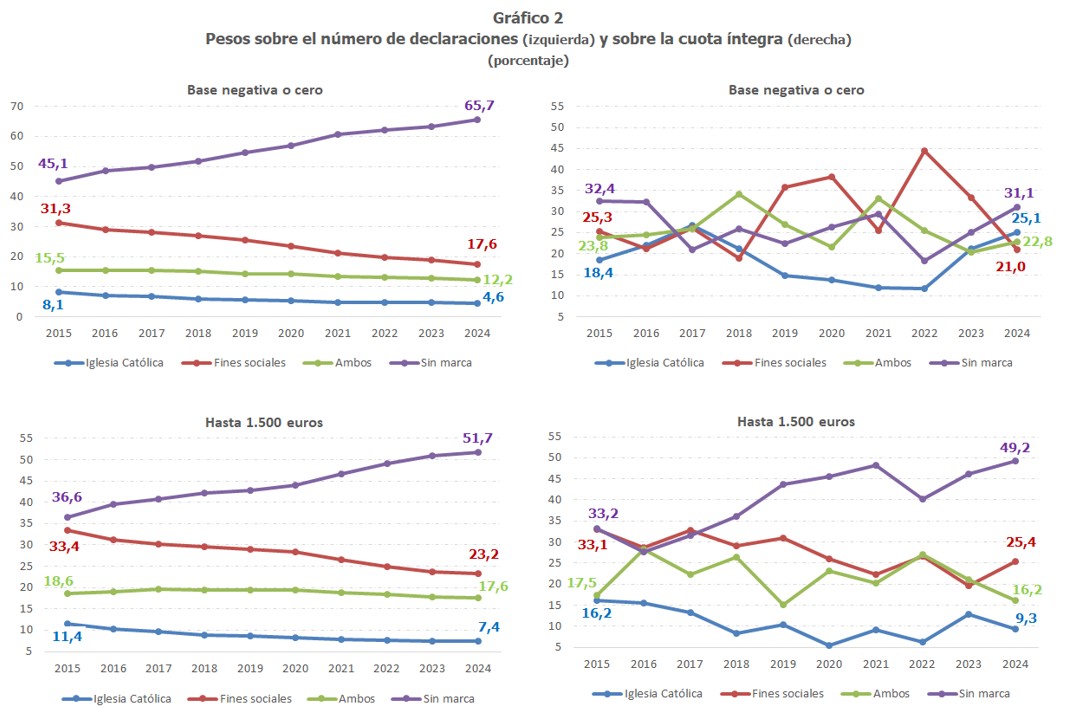

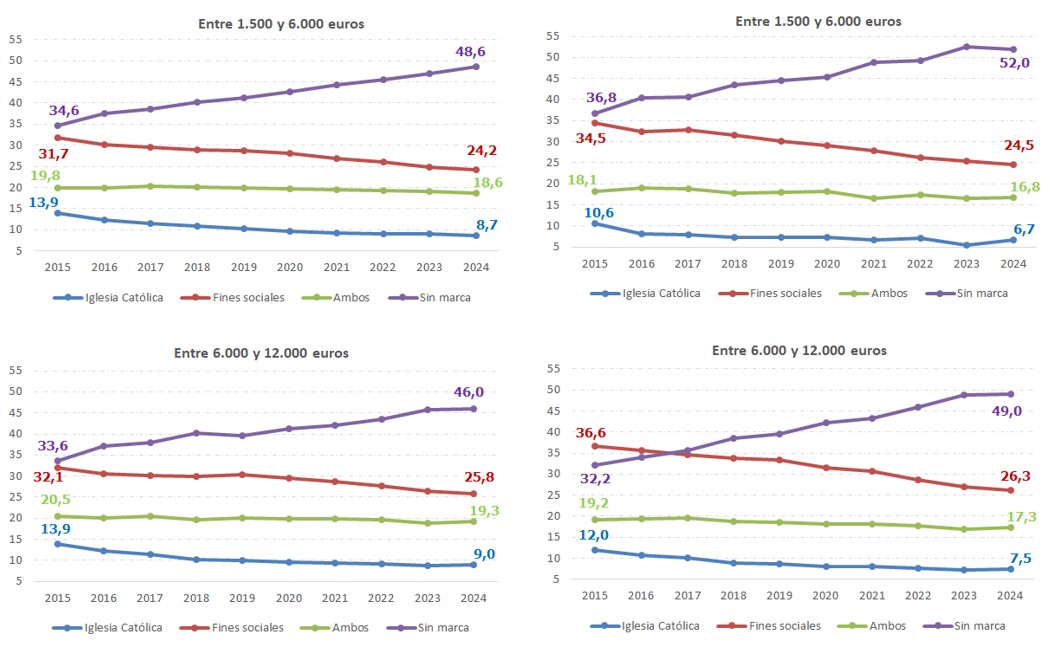

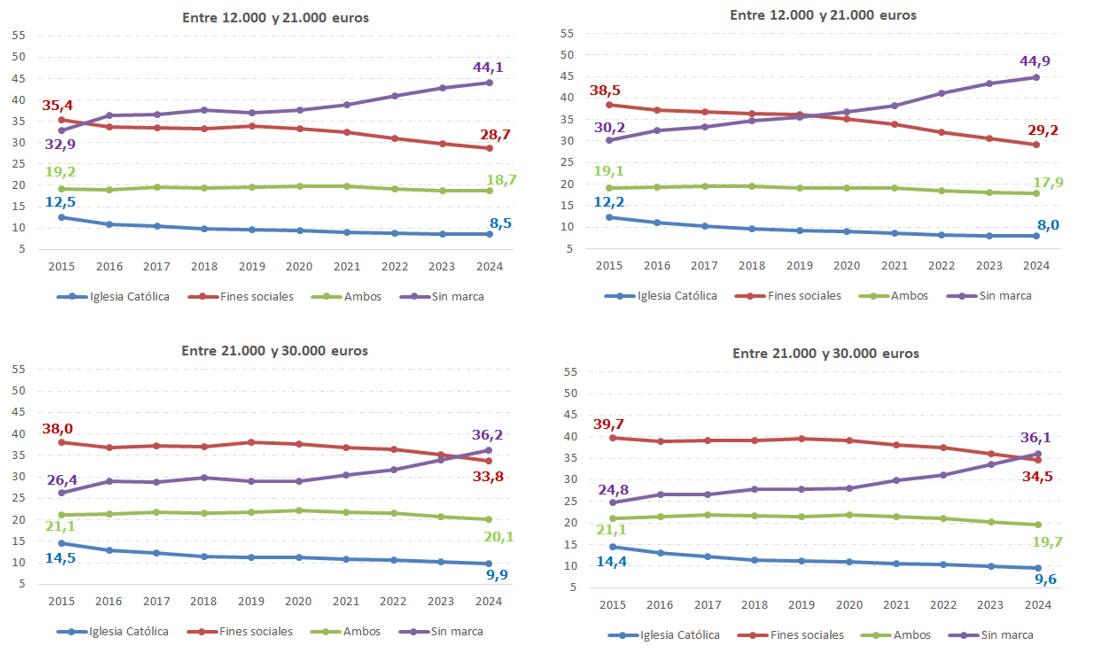

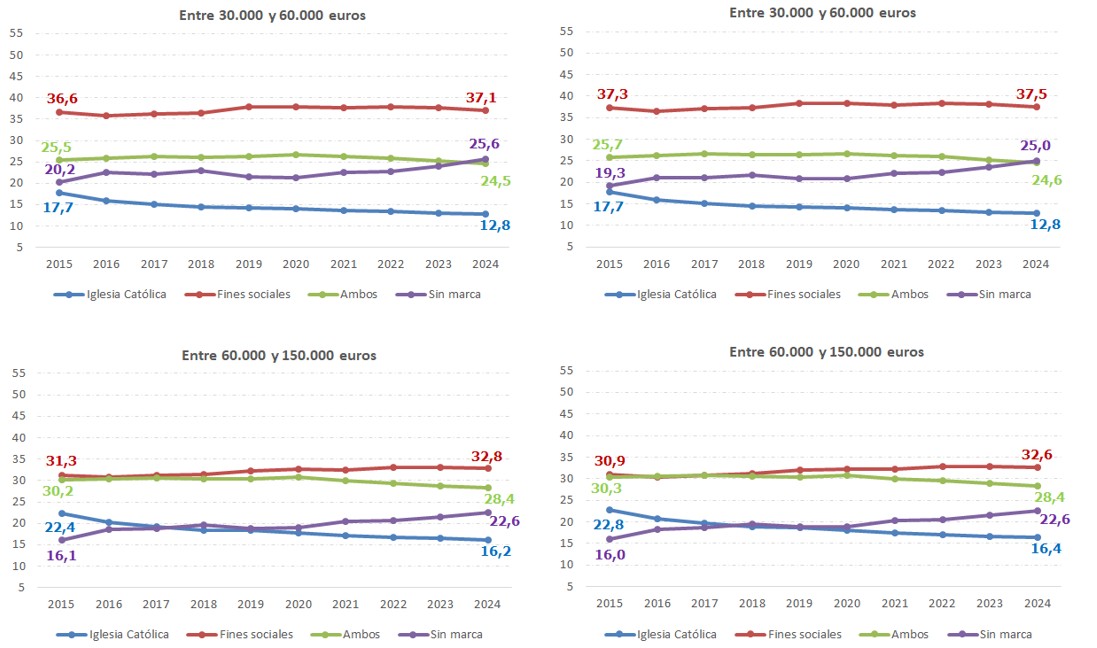

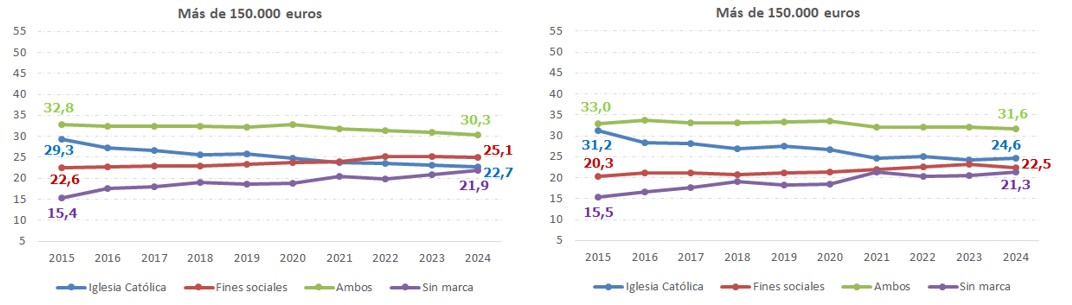

It is interesting to analyze the evolution of these options by breaking them down by the taxable base bracket. The graphs on the following pages show the trajectories for the period 2015 to 2024.

As a noteworthy aspect, it should be pointed out that in all income brackets there is an increasing trend in the weight of the "No Mark" option, with the most pronounced advance in the lower taxable income brackets, with the exception of the weights on the total tax liability for declarations with a negative or zero base, where the irregularity in the distribution is perhaps the most striking, along with the fact of the increased weight of the allocation to the Catholic Church in the last two years analyzed, to the detriment of the allocation to social purposes. A contrary trajectory, with the aforementioned exception, has shown the weight of the allocation to the Catholic Church, which has been losing importance in all basic levels. The weight of the option to check both boxes has also shown a decreasing trend, although the loss has not been as pronounced as in the case of the Catholic Church. Regarding the allocation for social purposes, its evolution is different depending on which base bracket is analyzed. Thus, for bases below 30,000 euros, the trend has been decreasing in the analyzed period, while, among bases above this figure, this option has been gaining relevance. Furthermore, the weight loss in the former has been more pronounced than the gain observed in the bases greater than 30,000 euros.

Also noteworthy is the relative importance of the unbranded option in the lower taxable income brackets, compared to the weight of the other three options, representing around half of the total tax liability for all taxable income brackets below 12,000 euros and almost always being the most popular option. For this grassroots group, the second most chosen option is allocation to social purposes. For tax bases between 12,000 and 30,000 euros, the unbranded options and those allocated to social purposes account for around 70% of the weight, with the allocation to social purposes becoming the most chosen option for taxpayers with tax bases between 21,000 and 30,000 euros. However, starting from a base income of 30,000 euros, the "No mark" box is no longer among the first two options chosen, and gives way to those taxpayers who choose to mark both boxes. This option is at very similar levels to that of those who choose to check the box for social purposes among taxpayers with incomes between 60,000 and 150,000 euros, becoming the most chosen option among taxpayers with incomes above 150,000 euros, the only group in which the option of allocation to the Catholic Church has occupied second place in importance until the 2021 fiscal year. For the rest of the bases, the allocation to the Catholic Church is the minority option.

1 All public information relating to the Allocation to the Catholic Church and Social Purposes can be found in the file Data on allocation to the Catholic Church and social purposes PIT which is published together with the Annual Tax Collection Report. Since 2015, disaggregated information has been provided by taxable income brackets, age, sex and CC. AA.