Information note 8. The consolidated annual accounts for corporate income tax

Along with the Tax Collection Report (IART) of 2018, the Informative Note was published The Consolidated Annual Accounts for Corporate Income Tax due to the publication, since the 2016 fiscal year, of the new statistics referred to in the note. As was explained then, statistics Consolidated annual accounts for Corporate Income Tax It combines the information provided by the 200 models of individual companies not integrated into groups and that from the 220 models presented by the groups, so that all figures, except profit, are calculated on a consolidated basis. This overcomes the limitations that the Statistics by item and statistics Unconsolidated annual accounts for Corporation Tax, providing a comprehensive view that revolves around the consolidated net tax liability, which is the appropriate measure of the contribution of all companies to the State's tax revenues.

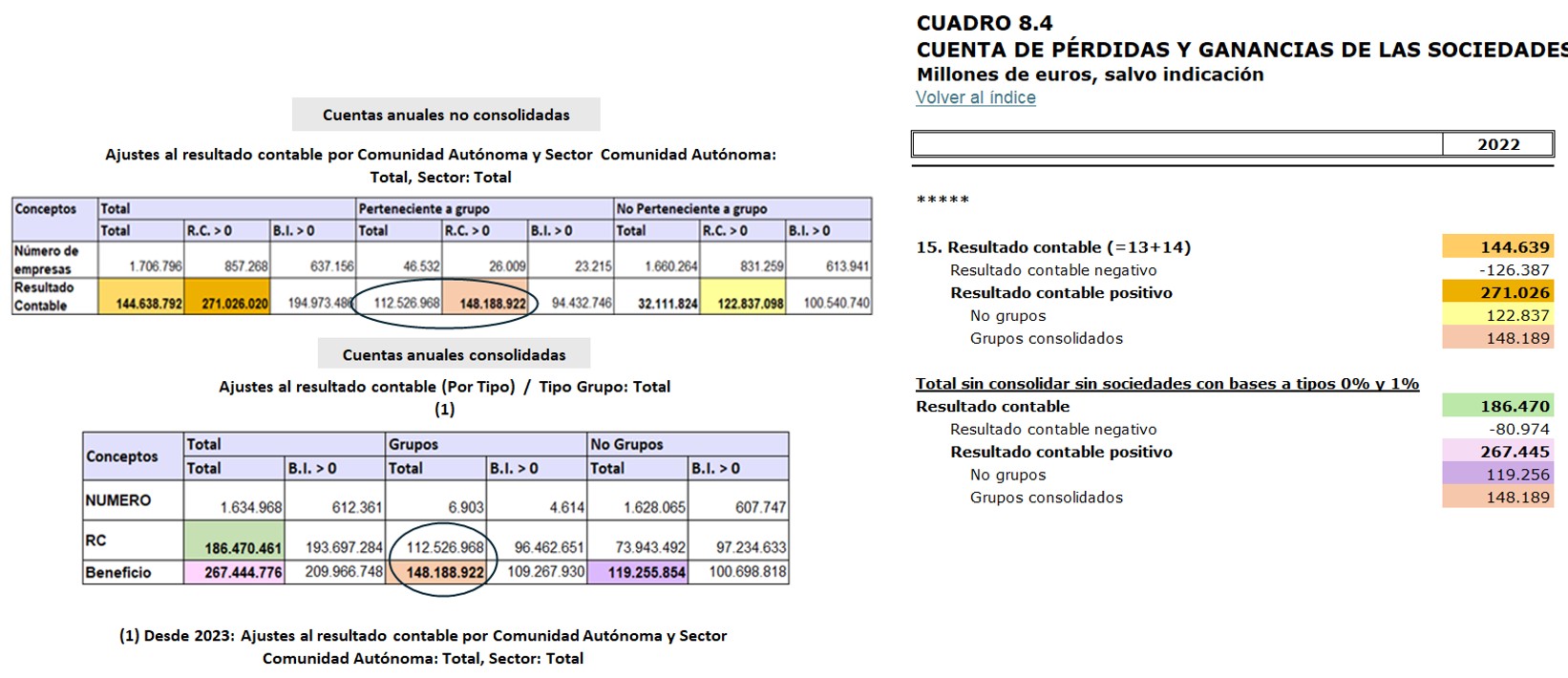

The Annual Revenue Reports include the analysis of Corporate Income Tax in tables 8.4 and 8.5. The first one presents the profit and loss account up to the accounting result of the group of companies, information that is not affected by consolidation.

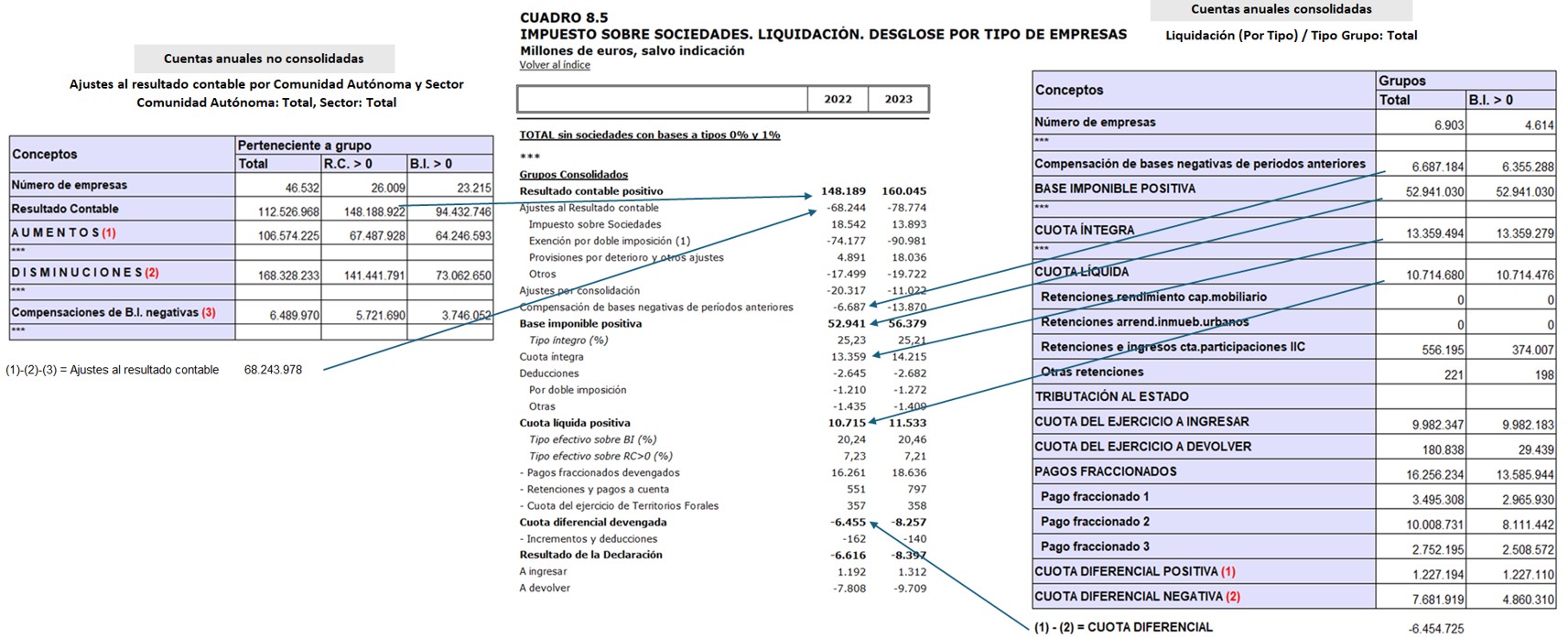

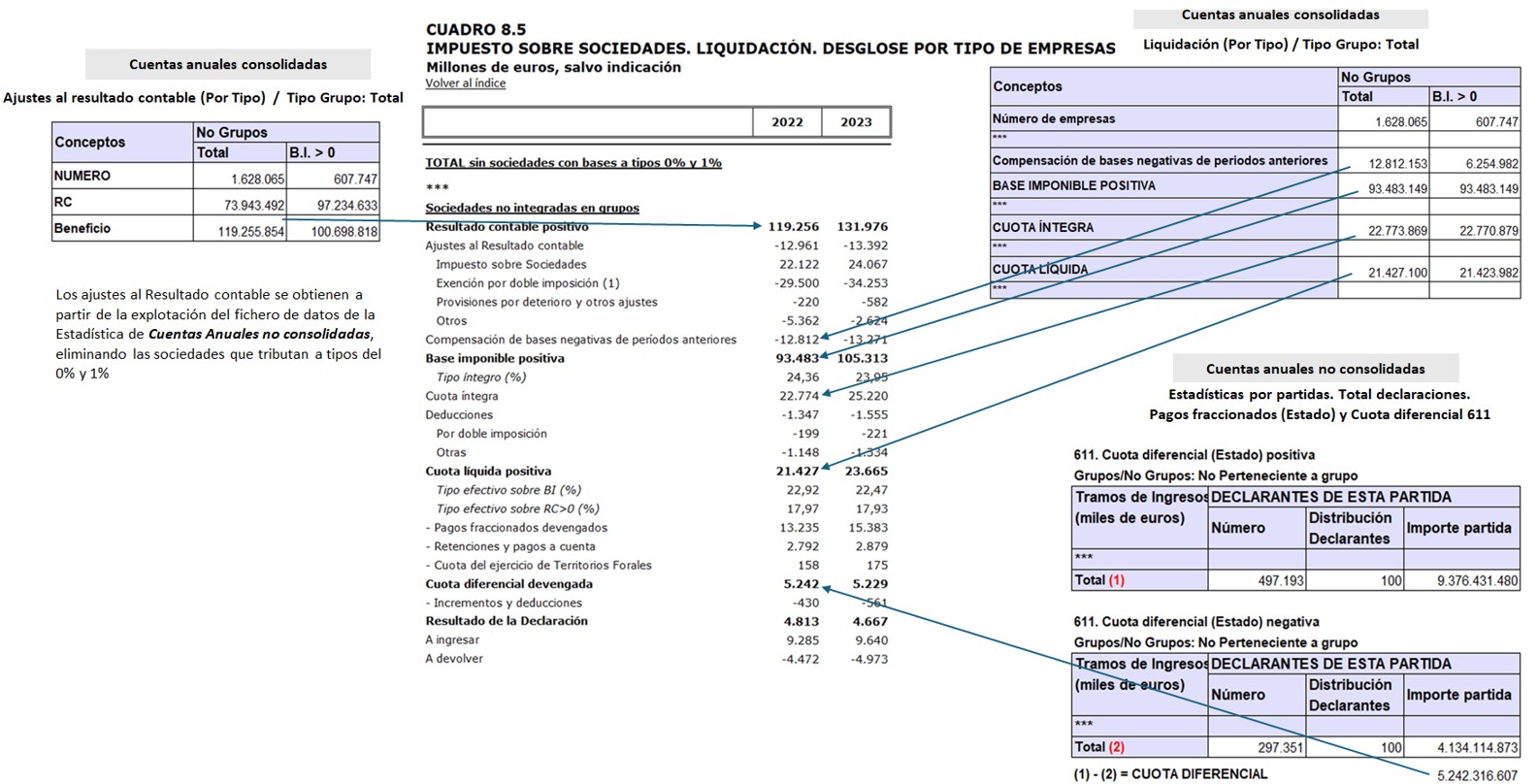

Since the publication of IART As of 2024, Table 8.4 incorporates a section that includes the accounting result excluding companies with tax bases at rates of 0% and 1%, which becomes the initial item in Table 8.5, where the tax settlement is summarized. The reason for this change (previously table 8.5 began with the total positive accounting result) is the irregular behavior of the profits of companies with bases at rates of 0% and 1%, almost all of them financial (pension funds, investment companies, …), which are linked to the valuation of their assets which, in turn, depends on changes in interest rates and the reactions of the financial markets. This fact has a significant impact on the variation of profits, but it barely affects the tax given its low or non-existent taxation. The exclusion of these companies brings coherence to the comparative analysis of the evolution of profits and the tax base, and is the criterion used in the Consolidated Annual Accounts of Corporate Income Tax statistics. Table 8.5 shows the tax settlement for the two relevant groups, companies not belonging to groups and consolidated groups, integrating the information from forms 200 and 220.

The charts below detail the source of information for both tables and the connection of the main variables with the two annual accounts statistics.