Hydrocarbon Tax

Find out about tax on fuels and combustibles

Tax measures to combat the energy crisis resulting from the armed conflict in the Middle East.

Modifications to the regulations governing the Hydrocarbons Tax. Royal Decree-Law 18/2026, of June 29, adopting certain measures within the framework of the Comprehensive Response Plan to the Crisis in the Middle East

1.- TAX RATES FOR THE HYDROCARBON TAX CORRESPONDING TO THE MONTHS OF JULY, AUGUST AND SEPTEMBER 2026

In order to mitigate the effects of the Middle East Crisis on the increase in energy product prices, various reductions in the tax rates of the hydrocarbon tax are approved for the months of July, August and September 2026. These price reductions affect, among other products, unleaded gasoline and diesel fuels (the most widely used).

The planned price reductions for gasoline and diesel in August 2026 will increase if the CPI for these products in June 2026 exceeds the CPI for the same month of the previous year by more than 15 percent.

Meanwhile, the planned price reductions for September 2026 will increase if the CPI for these products in July 2026 exceeds the CPI for the same month of the previous year by more than 15 percent. A larger increase is expected this month when the CPI for these products in July 2026 does not exceed the CPI of the same month of the previous year by more than 15 percent, but does exceed it in June 2026.

- Applicable tax rates in July 2026

In accordance with Article 5 of Royal Decree-Law 18/2026, the tax rates for the Hydrocarbons Tax on gasoline and diesel applicable during the month of JULY 2026 are as follows:

(tax rates are set per 1,000 liters)

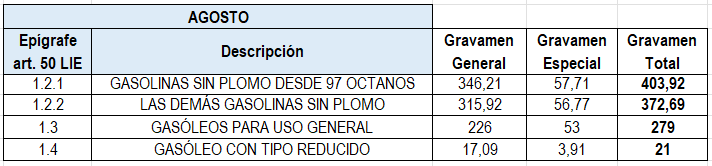

2. Applicable tax rates in August 2026

In accordance with Article 6 of Royal Decree-Law 18/2026, the tax rates for the Hydrocarbons Tax on gasoline and diesel applicable during the month of AUGUST 2026 are reduced as follows:

(tax rates are set per 1,000 liters)

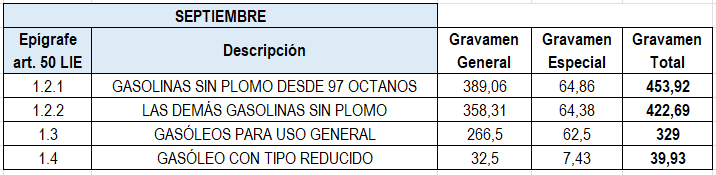

3. Applicable tax rates in September 2026

In accordance with Article 7 of Royal Decree-Law 18/2026, the tax rates for the Hydrocarbons Tax on gasoline and diesel applicable during the month of SEPTEMBER 2026 are as follows:

(tax rates are set per 1,000 liters)

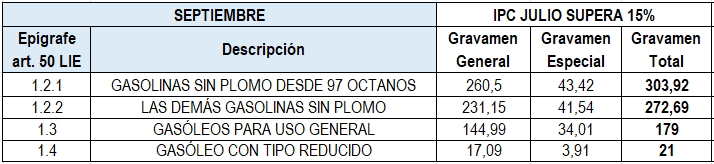

However, depending on the evolution of the CPI for gasoline and diesel in July 2026 compared to the same month of the previous year, the following tax rates may apply in September 2026:

(tax rates are set per 1,000 liters)

2.- RATE OF PARTIAL REFUND OF THE HYDROCARBON TAX FOR DIESEL FOR PROFESSIONAL USE

Pursuant to Article 8 of Royal Decree-Law 18/2026, from July 1, 2026 until September 30, 2026, the refund rate regulated in Article 52 bis.6 of Law 38/1992, of December 28, on Special Taxes, will be zero euros.

3.- RATE OF PARTIAL REFUND OF THE TAX ON HYDROCARBONS FOR DIESEL INTENDED FOR AGRICULTURE

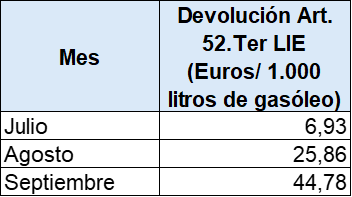

Pursuant to Article 9 of Royal Decree-Law 18/2026, the amount of the fees to be refunded for the Hydrocarbons Tax on diesel fuel actually used in agriculture, including horticulture, livestock and forestry, regulated in Article 52 ter b) of Law 38/1992, of December 28, on Special Taxes, will be:

In August 2026, the refund rate will be 0 euros per thousand liters if the tax rate for diesel in section 1.4 for that same month amounts to 21 euros per thousand liters (17.09 + 3.91) depending on the evolution of the CPI.

For its part, in September 2026 the refund rate will be 0 euros per thousand liters if the tax rate for diesel in section 1.4 for that same month amounts to 21 euros per thousand liters (17.09 + 3.91) depending on the evolution of the CPI.