Improving efficiency. Indicator IV of the Strategic Plan

The strategic objective of the Tax Agency is to improve voluntary compliance with tax obligations; To achieve this, it uses a combination of measures of a wide range such as civic-tax education, information and assistance, prevention of tax and customs fraud, a posteriori control actions, the promotion of anti-fraud regulatory changes, agreements with other organizations, cooperative relations, etc.

It also happens that the Tax Agency not only aims to improve voluntary compliance with all the previous actions, but also sets the improvement of its efficiency as an autonomous and complementary objective.

A good way to measure this efficiency (and its evolution) is to relate the budgetary expenditure of the Tax Agency with the net tax revenues that it manages in each exercise. This relationship constitutes Indicator IV of the Strategic Plan.

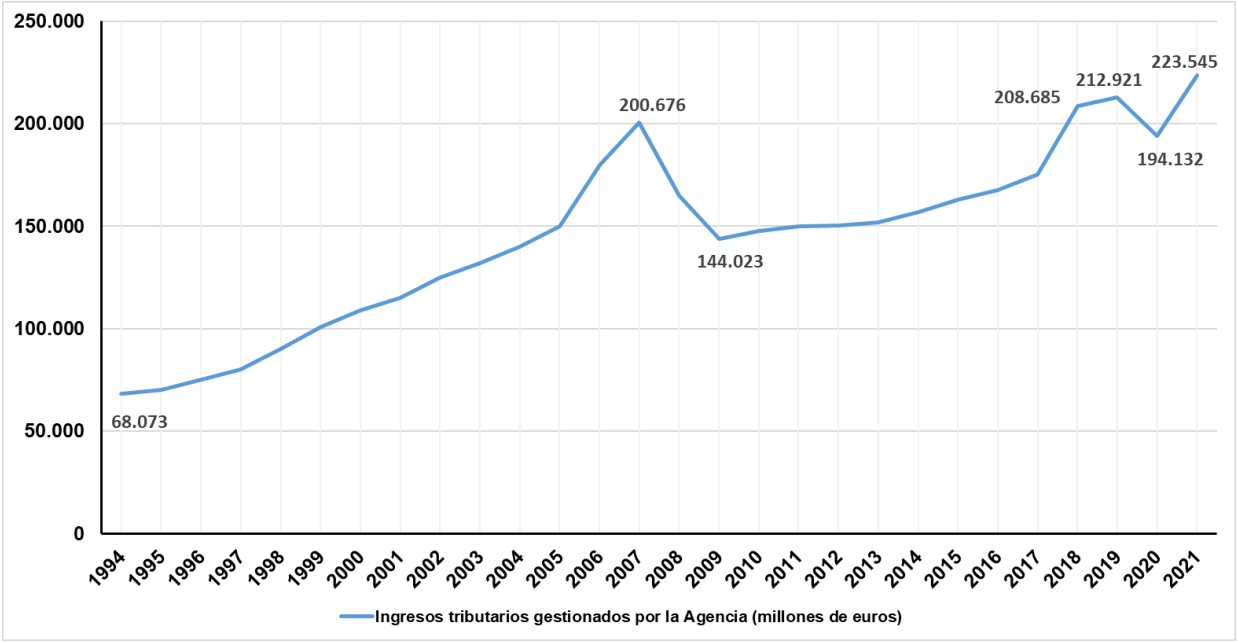

net tax revenues grew constantly between 1995 and 2007, with a sharp decline in 2008 and 2009 as a consequence of the economic crisis, returning to the growth path from 2010 until 2019 -2020, in which it was cut short as a result of the pandemic. In 2021 there was a strong recovery that allowed collection to reach 223,545 million euros (15.15% more than the previous year).

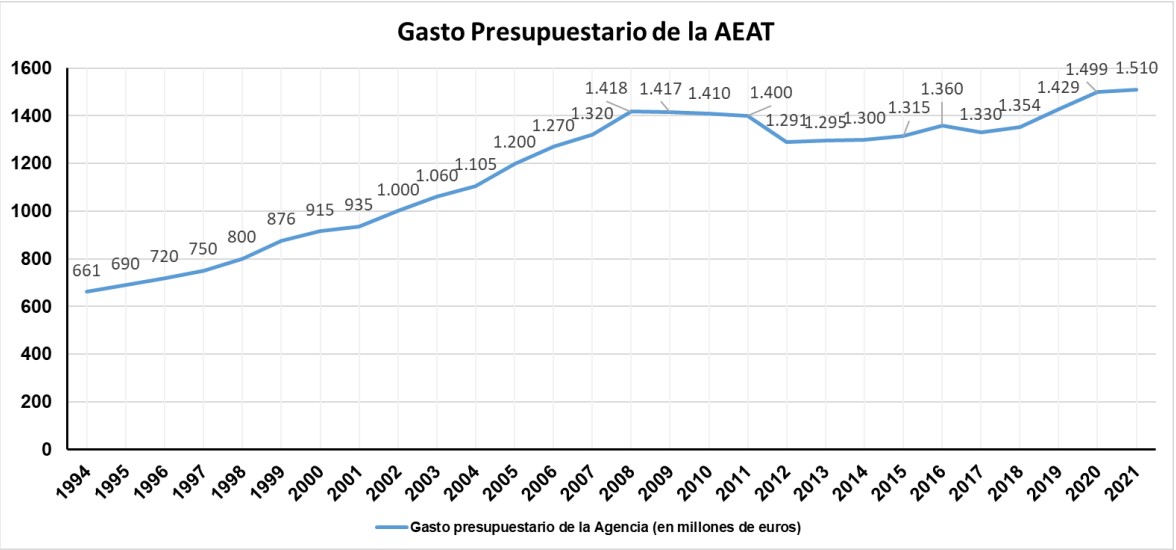

Regarding the budget expenditure executed by the Tax Agency, after the budgetary restrictions derived from the economic crisis, the budget has been recovering slowly, boosted in its growth due to the gradual incorporation of new personnel into its workforce.

The comparison of the previous data - for the period 1995-2021 - allows us to appreciate that while the collection managed by the Tax Agency multiplied by 3.3, the institution's budgetary expenditure multiplied only by 2.2.

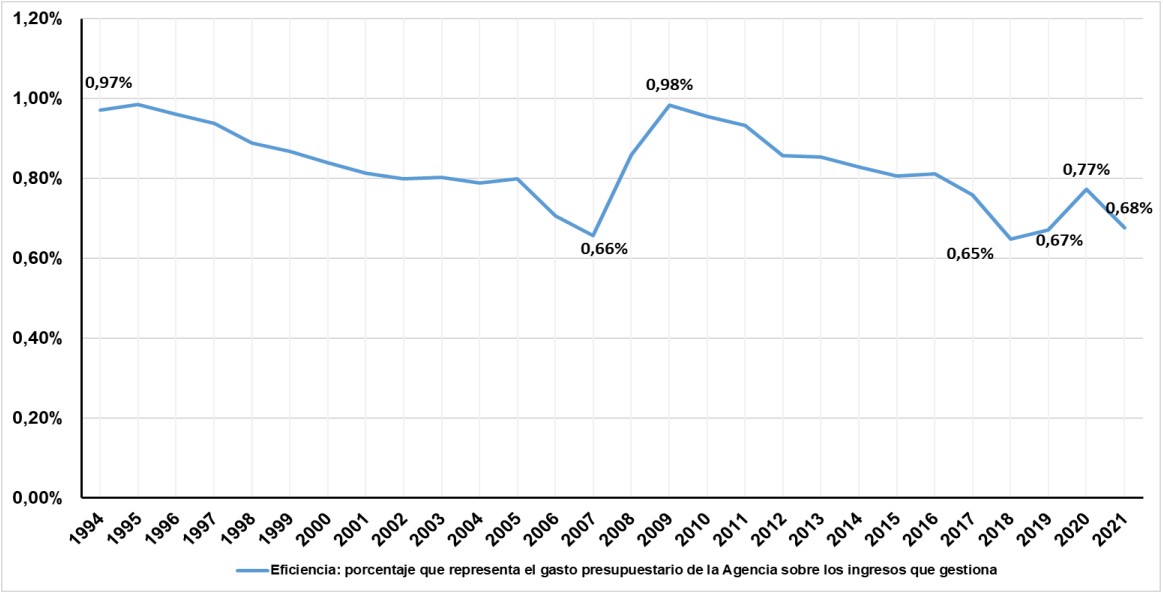

The combination of the two aforementioned magnitudes, tax revenue and budgetary expenditure, allows us to calculate the efficiency ratio of the organization, meaning, expressed as a percentage, the annual budgetary cost that the Agency represents. Tax with respect to all the net tax revenues managed in each year. (For the analysis and assessment of said ratio, years in which exceptional circumstances have occurred - abnormal growth in income or prolonged budget restrictions over time - should not be used as valid references).

Having stated the above, the Strategic Plan considers that the efficiency ratio of the Tax Agency must be around 0.7% (below the average of the countries around us), that is, the annual budgetary cost of the organization should not exceed 0.7% of the net tax revenues it manages, understanding that this ratio is compatible with the increase in staff necessary to recover the staff that the Tax Agency had before the crisis.

The following table shows the evolution of the ratio and how in 2021 it stood at 0.68%, thus meeting the efficiency objective committed by the Tax Agency in its Strategic Plan.