The "Veri*factu Regulation"

After extensive processing, on December 6, 2023, Royal Decree 1007/2023, of December 5, was published in the BOE, approving the Regulation that establishes the requirements that must be adopted by computer or electronic systems and programs that support the billing processes of entrepreneurs and professionals, and the standardization of billing record formats.

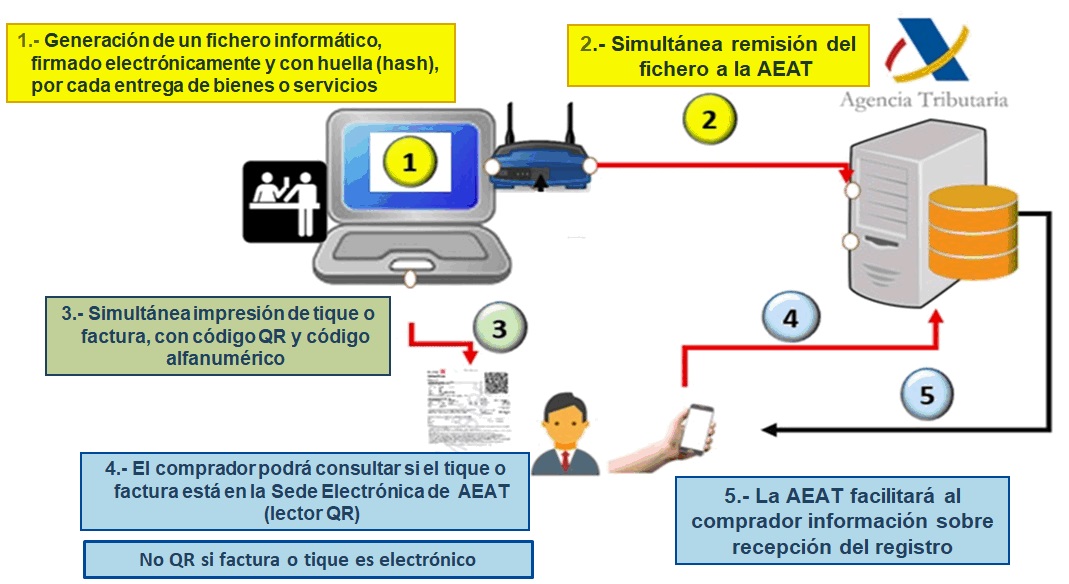

The regulation is a direct development of the modification of article 29.2.j) of Law 58/2003, of December 17, General Tax Law, in the wording added by Law 11/2021, of July 9, on measures to prevent and combat tax fraud. The standard aims to establish the way in which billing records produced by computer systems must comply with the legal requirements of integrity, conservation, accessibility, legibility, traceability and inalterability, thus avoiding the so-called 'dual-use software' or 'sales concealment software' that has sometimes been observed in sales to the final consumer. For this primary purpose, the Royal Decree defines an invoice register, with a specific format and structure, to which certain computer security elements are added (chained hashes and electronic signature) that ensure that said register cannot be modified, after it has been produced, without the corresponding record of said modification remaining.

This regulation is colloquially known as the 'Veri*factu Regulation', referring to the simplest and most efficient method for complying with the standard by sending the billing records to the electronic headquarters of the Tax Agency at the time of their production.

In addition to the fight against fraud and tax evasion, these systems will allow progress in the digitalisation of companies and improve the assistance services that the Tax Agency provides to taxpayers, offering them the possibility, when they use 'Veri*factu' systems with data submission, to download operations, thus facilitating the preparation of tax record books and tax forms.

The new regulation will apply to all businesses and all their operations, with the exception of those who are already subject to the Immediate Supply of Information (SII) or those who do not have an obligation to invoice. As regards its territorial scope, it is applicable throughout Spain except in territories with a regional tax regime. In the Historical Territories of Vizcaya, Guipúzcoa and Álava, the so-called 'Ticket Bai' systems have recently been applicable, the operation of which is similar to that now approved for the rest of Spain.

It should be noted that, in the system provided for in the regulation, clients will be able to check the tax quality of the simplified invoices received by comparing them on the Tax Agency website.

This Royal Decree will be followed by the Ministerial Order for technical development, from which software developers will have to comply with its provisions within a maximum period of 9 months. In addition, their products must include a “responsible declaration” of compliance with this regulation.

All companies and self-employed persons required to comply with the regulations must comply by 1 July 2025. To this end, it is planned that SMEs and self-employed workers can use the digital kit of the Recovery, Transformation and Resilience Plan to finance the modifications to computer programs that are necessary to adapt to the new regulations.

Finally, it should be noted that this regulation is compatible with the Draft Regulation on B2B Electronic Invoicing, currently being processed by the Ministry of Economy, Trade and Business with the participation of the Tax Agency. The IT systems of businesses must be fully adapted to both changes, using a single data model based on mandatory invoice details and payment methods and terms.

![]()