The obligation to file the annual personal income tax return: What are the characteristics of people who file a tax return without exceeding the thresholds?

The Income Tax Campaign is currently underway, as is customary at this time of year. It is worth remembering that all people who reside in the country and receive income, regardless of where it comes from, are taxpayers. However, not all of them are required to file the annual tax return.

The delimitation of the obligation to declare has several aspects of very different nature. The basic idea is that people whose income has not exceeded certain amounts, which in turn depend on the type of income received, should not file a tax return. In the most widespread case, that which refers to the total income from work, the threshold is set at 22,000 euros per year when the income comes from a single payer and at 15,876 euros if there are several payers (with various exceptions in which the threshold is again the previous one). Other limits apply to other types of income and circumstances (for example, 1,600 euros for those who obtain income from movable capital subject to withholding, such as bank interest).

In addition to the obligation imposed by these thresholds, in recent years the duty to file a declaration has been added to some groups regardless of the amount of their income, such as the beneficiaries of the Minimum Living Income or, from 1 January 2023, those people who have been registered at some point during the year in the special self-employed schemes of the Social Security.

Furthermore, those who wish to enjoy some of the refunds or reductions of the taxable base to which they are entitled and which can only be exercised by submitting the declaration must also file their declaration. This is the case, for example, of those people entitled to family refunds if they have not been received in full in advance, or those who have made contributions to pension plans that reduce their taxable income and, as a result, generate a refund of withheld amounts.

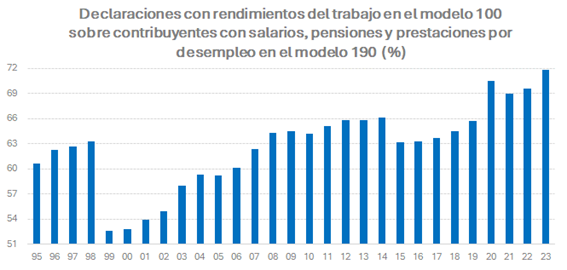

The existence of people who, being taxpayers, are not required to submit the annual return already existed before the change in the tax structure that occurred in 1999 through Law 40/1998. However, that modification and the associated management changes significantly increased the number of people not obligated. The following graph shows an indicator of non-obligation to declare, calculated as the number of declarations with employment income divided by the number of people with salaries, pensions, and unemployment benefits in the annual form 190, which is the declaration of payers that reports on these withholdings (the data can be consulted in the Annual Tax Revenue Report). The indicator allows us to see the effect of the changes that occurred in 1999 and the subsequent upward trend.

The upward trend in this ratio indicates the existence of an increasing number, in relative terms, of people required to file the declaration. There are several reasons for this trend; These include the creation of new deductions (both state and regional) that can only be used in the annual tax return, the inclusion of groups of taxpayers regardless of their income, and the growing mismatch between the rate used in calculating withholdings and the one used in determining the final tax liability due to the greater exercise of their regulatory power by the Autonomous Communities. and finally, the incomplete updating of the thresholds (the general limit, which is currently at 22,000 euros, was 21,035 euros in 1999).

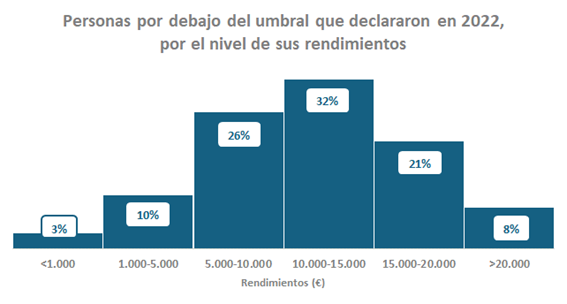

The progressive extension of the obligation to declare, for one reason or another, can be analyzed from the number of people who do not exceed the thresholds, but who file their annual declaration. In fact, in recent years, around half of the people whose incomes are below those limits file a tax return. How many of these people are there, and what are they like?

In the 2023 fiscal year, the last with closed and published data, 6.6 million taxpayers filed their tax return despite having income below the thresholds. That figure represented 48.1% of the total number of people in that situation. The percentage was slightly higher than in previous years, which was around 46.5%, but in any case, it indicates a consistency that makes this circumstance not anecdotal.

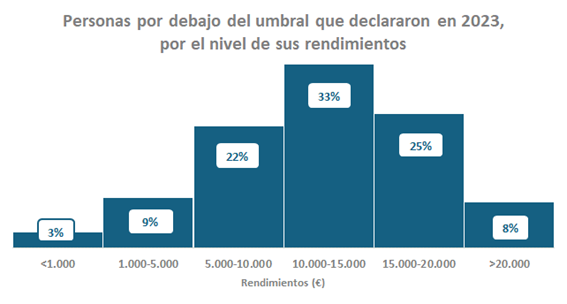

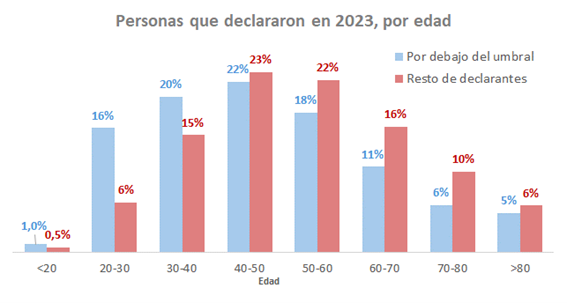

Contrary to what one might think, the people who file the declaration are not those closest to the general threshold of 22,000 euros, but are distributed following an asymmetric normal distribution, with the vast majority being people with incomes between 10,000 and 15,000 euros. The distribution is also very similar in different years. The last two are shown in the following graphs.

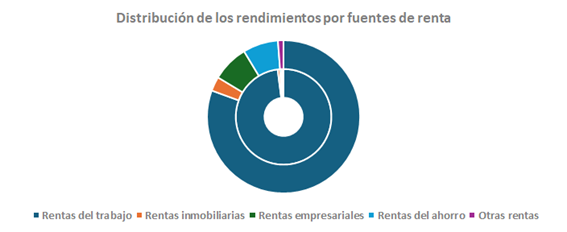

The structure of their returns has a clear bias towards labor compensation. The following chart compares the distribution of income by source for individuals below the threshold (inner ring) and the set of declarations in 2023.

As can be seen, the source of income for people below the thresholds is primarily from work; around 98% of it comes from this source, compared to approximately 80% for all taxpayers. The remaining incomes that do not reach the thresholds are marginal and concentrated in real estate and savings income.

There is more similarity in personal characteristics, although with significant differences. If the distribution by age is analyzed, it can be seen that people below the threshold are somewhat younger than the rest of the declarants; On average, the former are about six years younger than the latter.

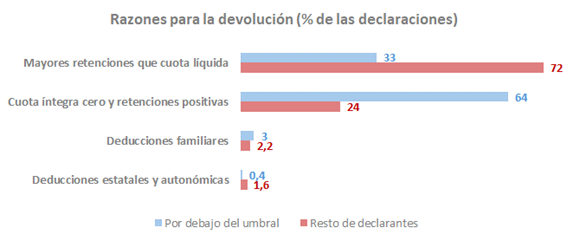

Logically, most people who file tax returns even if they are below the threshold do so, if they are not required to do so for other reasons, to request a refund of the amounts previously withheld or paid on account. In the 2023 tax year, 85% of these people's tax returns resulted in a refund (virtually all the remaining returns resulted in zero income, and only a very marginal portion had a tax liability). The reasons for the negative sign are, however, different from those observed in the rest of the declarants. The following chart shows the four reasons why a statement might return a result for both groups.

The most significant reason why the tax return result is negative for people below the thresholds is having a total tax liability equal to zero, which is explained by the low level of their income. In that case, almost two-thirds of the returns are due for refund. In one-third more the net quota becomes positive, but lower than the withholdings made. Negative results due to the existence of deductions, of one type or another, are residual. The result is very different from that obtained in the rest of the declarants in which almost three-quarters of the refund requests are caused by having withholdings higher than the net tax liability and only in a quarter of the refunds does the taxable base give rise to a total tax liability of zero.

In conclusion, it can be said that, although the system was originally intended to exempt a large number of taxpayers from the obligation to file tax returns, the evolution of the tax has gradually incorporated more and more people. Among these are those that fall below the established thresholds, but end up filing their tax return because their tax liability is zero or very small, and thus manage to recover all or part of the withholdings that have been applied to them throughout the previous year.