Payment of settlements and debts by bank transfer

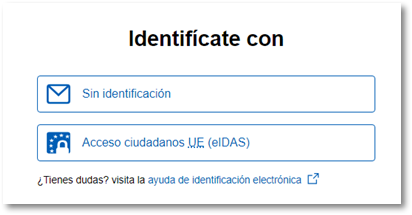

The payment of settlements and debts through the AEAT It can be done by transfer, provided a IBAN corresponding to a non-collaborating entity in the tax collection of taxes of the AEAT. You can identify yourself with eIDAS or access without identification.

The transfer is a non-face-to-face payment option for those obliged parties who do not have an account in their name in any collaborating entity of the AEAT and also accepts financial entities in foreign countries.

Note: payment by bank transfer is not available for accounts of collaborating entities with AEAT, for which the payment services by direct debit and card payment or Bizum are available.

Through this formality, the taxpayer establishes a payment commitment with the AEAT and obtains the necessary data to subsequently make the transfer from your financial institution within the established term.

Follow these instructions to obtain the identifying data of the bank account of the AEAT to which you must make the transfer, as well as the payment IDENTIFIER that you must use in the "Concept" field of the transfer. Please note that this identifier will be valid for 30 calendar days from the date of its issuance.

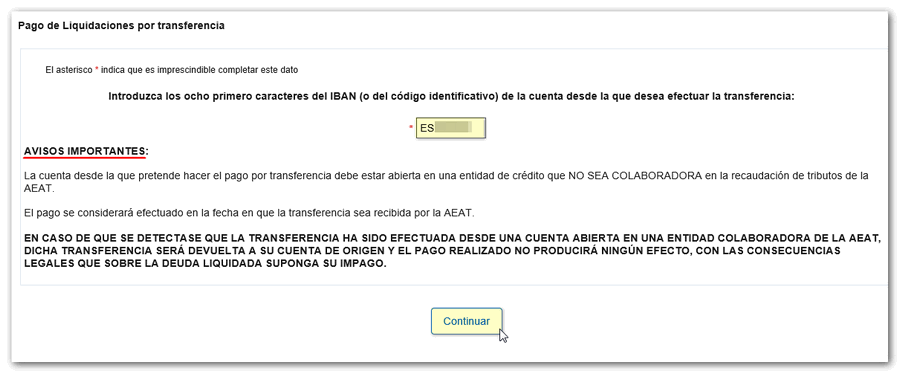

After logging in, you must enter the first eight characters of the IBAN (or the identification code) of the account from which you wish to make the transfer.

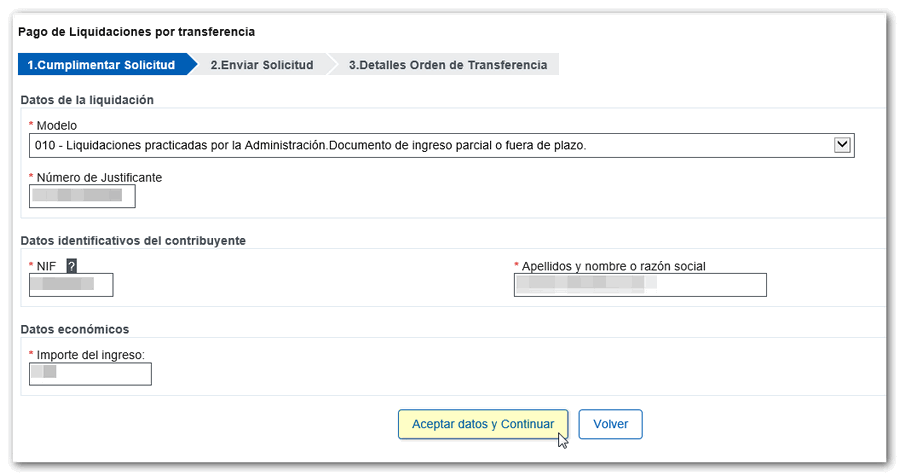

Select the appropriate model, the payment letter receipt number, the taxpayer's identification data and the amount. Then press "Accept data and Continue" .

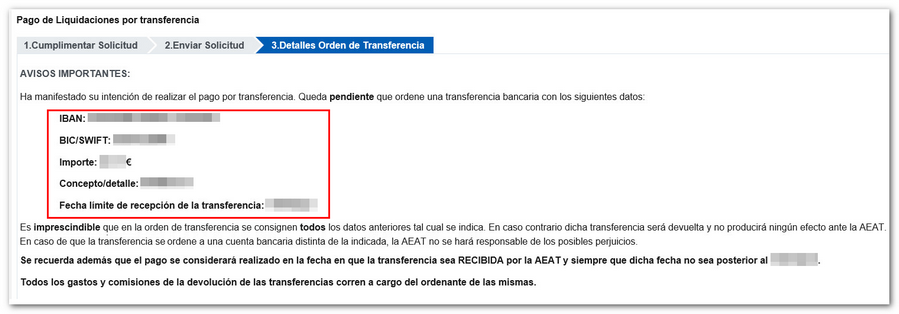

The data with which the transfer must be ordered from the bank will be obtained: IBAN , BIC / SWIFT , amount, concept/details and deadline for receipt.

Particular attention should be paid to the notices to ensure that the transfer is carried out correctly.

Payment will be considered made on the date the transfer is received by AEAT and provided that said date is within the indicated reception limit.