3. Corporate Income Tax

In the Corporate Tax revenue grew by 9% to 35.06 billion. Corporate profits increased by more than 10% in 2023, reaching a new record high, surpassing the level reached in 2019 (up 4%). In the case of the benefits from the split payments of Large Companies and groups, growth was above 15% (17% in Large Companies and 14.3% in groups), which was reflected in a similar increase in the collection from split payments, the main component of income in this figure. The growth of these profits was very high in the first months of the year, especially in the groups (and, in particular, in the energy and financial sectors), it moderated in the central part of the year, which was also compared with very good results from the previous year, and it recovered in the final part of the year. Part of the increase was due to the regulatory change that came into force at the beginning of 2023, whereby the tax base of a group was calculated in 2023 by adding the positive tax bases and 50% of the negative tax bases of the entities comprising the group.

The positive share of the annual declaration, corresponding to the 2022 settlement, also experienced a notable growth, exceeding 12%. As with payments, there was a regulatory change that boosted revenue; In this case, the minimum rate of 15%, which, although it was approved in the 2022 Budget, had its first application in the 2022 declaration submitted in 2023.

Despite these two elements, total revenue grew by only 9% as a result of the high amount of refunds in 2023, which is explained, in turn, by two reasons: the existence of a large volume of refund requests from the 2021 tax year (which were paid at the beginning of 2023) and the advance in the schedule for making refunds for the 2022 campaign.

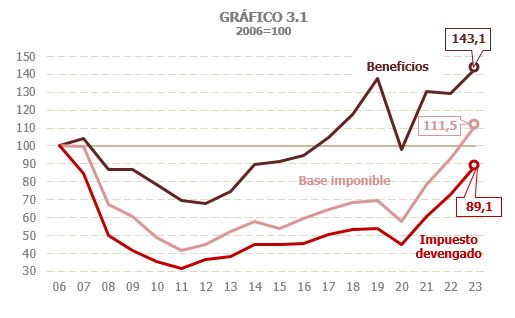

The consolidated tax base of Corporate Tax grew by 19.5%, a notable increase, especially considering that it is the third year with high records (18.7% in 2022 and 36% in 2021, Table 3.1 ). Chart 3.1 shows the evolution of the tax over the last 18 years, taking 2006 as a base, when both the tax base and the tax accrued reached their maximum amounts until 2023. Compared to 2006, profits in 2023 were 43.1% higher than then, while the tax base was only 11.5% higher, although for the first time above the previous peak reached in 2006. The tax accrued is still below the figures for that year, as is the case with the collection. The detailed trend of the tax since 1995 is shown in Table 8.5.

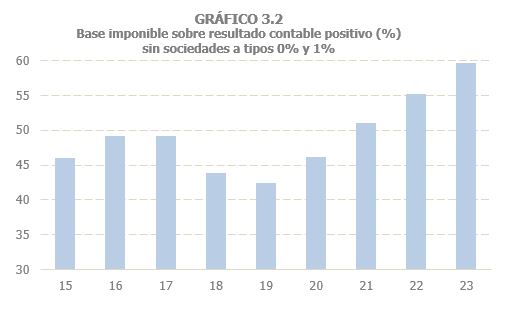

The effective rate on the tax base grew by 2.5% after the 0.8% increase in 2022, due to the effect of the regulatory changes discussed ( Table 3.1 ; Chart 3.5). The rate on profits, which depends not only on regulations but also on the different pace of profit growth in different types of companies and the relationship between profits and base, is estimated to rise by 10.8%. In this regard, it is necessary to note, on the one hand, the distortions that have been generated in recent years by companies that pay taxes at 0% and 1% rates with very irregular profits (linked to the valuation of their assets and, in turn, dependent on interest rate increases and the reactions of financial markets) that affect total profits, but hardly the tax accrued or the income given their low or non-existent taxation. On the other hand, in the last three years there has been a progressive approximation of the tax base to profits. In Chart 3.2 you can see this movement, which is fundamentally related to the lower adjustments derived from the exemption for double taxation ( Table 8.5 ) whose regulation was modified in fiscal year 2021.

The Corporate Tax accrued increased by 22.5% in 2023, 13.7% without the differential rate ( Table 3.1 ), thanks to the 15.2% increase in fractional payments, which already link three years of strong increases. This year they also benefited from the regulatory change that affected the calculation of the taxable bases of the groups. Payments by consolidated groups grew by 14.6%, with a lower contribution from the minimum payment, which grew by 9.1% (712 million more than the previous year, compared to the 2,943 million increase in 2022). The growth in payments from large companies not belonging to groups was slightly higher, at 17.8%, with the increase in payments calculated according to the taxable base also being higher in this case (19%, compared to 8.9% for those using the minimum payment method). For their part, payments from SMEs grew at a rate of 12.3%. The largest increase was observed in the SMEs , the majority, which paid taxes according to their last annual quota (17.8%), while payments from companies that declared according to the profits of the year were reduced (-1.2%).

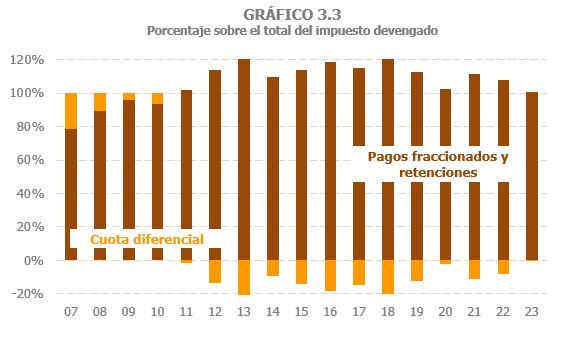

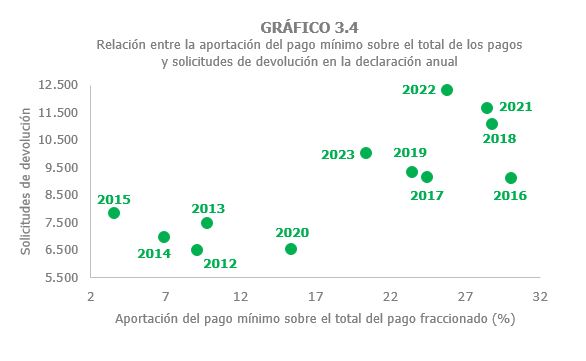

Charts 3.3 and 3.4 illustrate the relationship between payments and differential rate until completing the total amount of tax accrued. In 2021 and 2022, the high percentage of income from minimum installment payments also resulted in a high amount of refund requests and a negative differential rate. It is expected that the reduction in the weight of the minimum payment in 2023 to 20.4% will lead to a lower amount of refund requests when the annual declaration for the year is submitted and, consequently, that the differential rate will be of a reduced magnitude ( Table 3.3 ).

Cash revenue grew by 9% ( Table 3.1 ). The two concepts that most boosted tax collection were installment payments and income from the annual declaration. Split payments, which are the main component of the tax, grew by 15.2%, in line with the benefits associated with split payments by large companies and groups.

The contribution of income from the annual declaration was also positive, increasing by 12.1%. Income from the liquidation of the 2022 financial year increased by 11.3%, which is explained by the growth in profits in 2022 of companies excluding companies that pay 0% and 1% tax ( Table 3.1 ). In addition, we must add the effect of the new minimum rate of 15% applicable to groups and other companies with a turnover of more than 20 million, a measure that, when approved in the 2022 Budget, had its first effect in the 2022 financial year, the declaration of which was submitted in 2023.

One of the notable features of the year was the importance of the refunds of this tax, especially in the first part of 2023, although its effect conditioned the evolution of income throughout the year. Refunds of the result of the annual declaration, including those derived from settlements, were 21% higher than those of 2022 ( Table 3.3 ), which had already reached a high amount (only surpassed by those made in 2020). The two reasons for this increase were, on the one hand, the existence of a large volume of refund requests for the 2021 financial year, which grew by 78.5% and most of which were paid in 2023, and, on the other, the advance in the schedule for the 2022 campaign refunds (returns submitted from the end of July 2023). This high growth in refunds explains most of the discrepancy between the increase in tax accrued and the increase in revenue. The cash-to-accrual graph in Figure 3.5 illustrates this effect.