Information note 10. The tax on tobacco products

On January 1, 2025, the increase in tax rates applicable to tobacco products came into effect, an increase that affected all products subject to this special tax. Since 2013 there had not been a significant variation in types that extended to all tobacco products. That is why it may be of interest to carry out an analysis of the evolution of tax rates, prices and consumption of tobacco, as well as an international comparison of the taxation of these products in the countries around us. All the information relevant to the analysis of the Special Tax on Tobacco Products presented in this note, as well as information relating to the other special and environmental taxes, can be found in the Special Tax Report accessible on the website of AEAT.

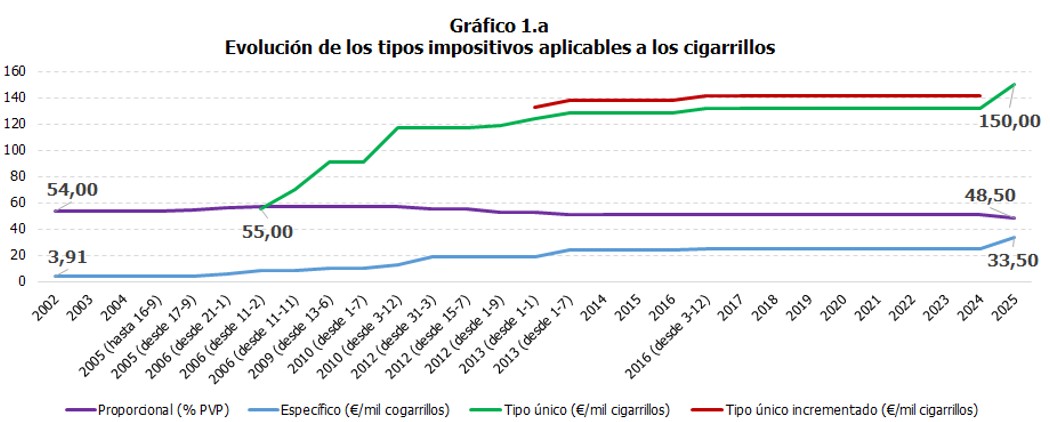

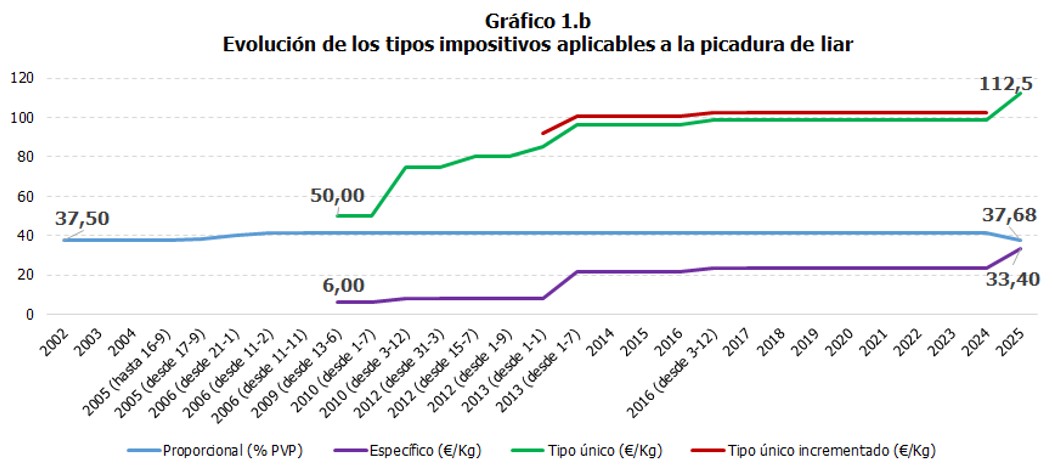

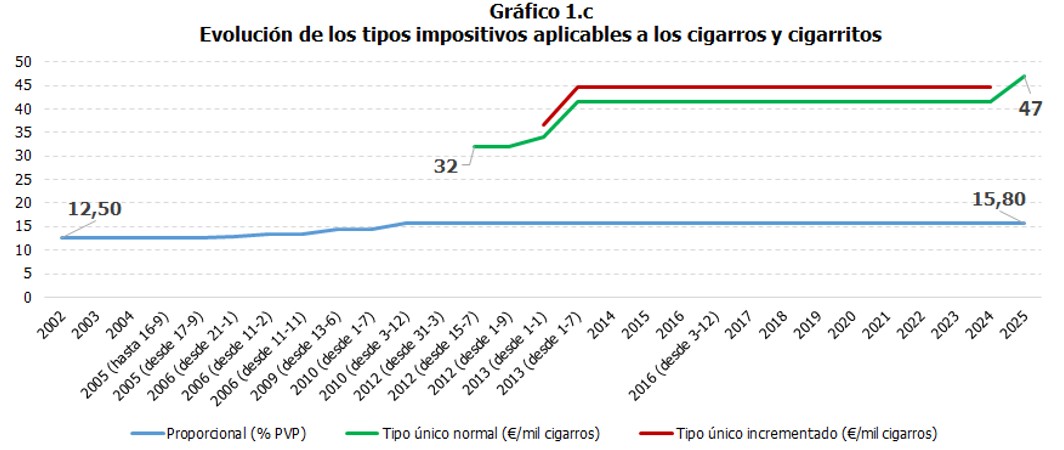

The 2025 rate changes involved, among other things, a simplification of the tax structure by eliminating the single increased rates on cigarettes, cigars and tobacco. At the same time, this elimination was accompanied by an increase in the single rates of between 13% and 14%, except in the case of the rest of the tobacco products in which the increase was greater, around 36%. In addition, the specific types of cigars and cigarettes increased, and their proportional types decreased. Finally, the proportional rate applied to the rest of the tobacco products was increased, while the rate for cigars remained the same.

Graphs 1.a, 1.b and 1.c show the evolution of the rates applied to the main tobacco processes1It can be seen how there has indeed been a long period of time in the Special Tax on Tobacco Products characterized by relative stability.

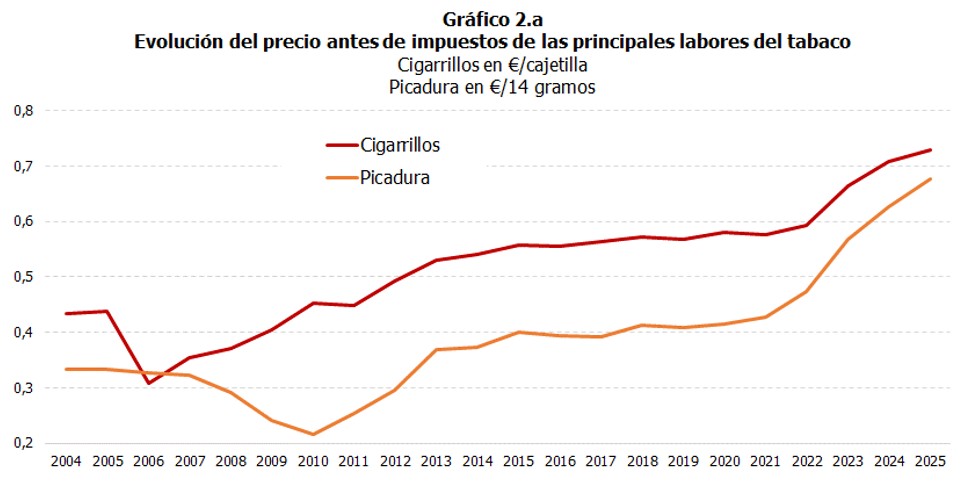

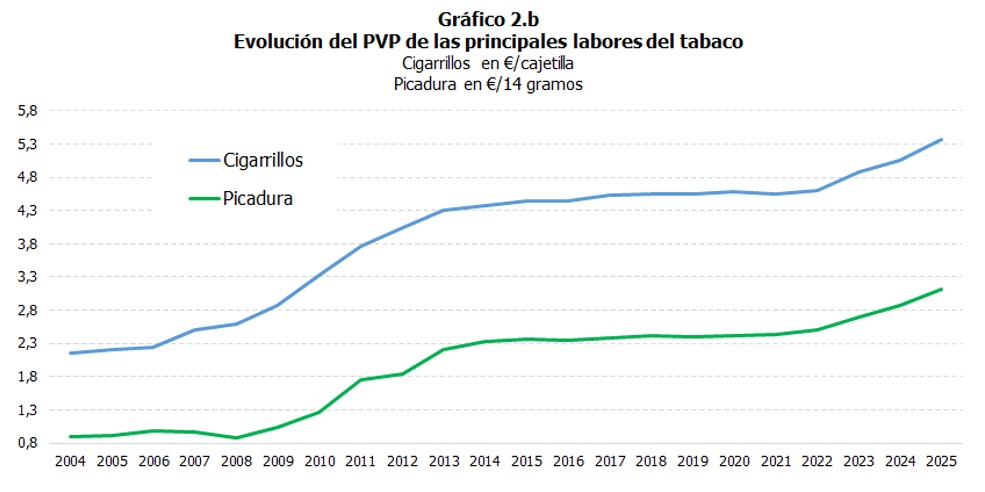

The tax structure and its evolution has had a clear impact on the evolution of retail prices (RRP) of the different tobacco processes in Spain. As can be seen in Graph 2.a, the pre-tax price of a pack of cigarettes and 14 grams of loose tobacco (an amount approximately equal to the amount of tobacco contained in a pack) have moved in a very similar way, with a slight upward trend in both cases, and the price of loose tobacco always remaining lower. In the case of the RRP For both products (Graph 2.b), the trend has also been upward and very similar, although in absolute terms the RRP The consumption of cigarette packs has been significantly higher than that of the equivalent amount of loose tobacco throughout the analyzed period.

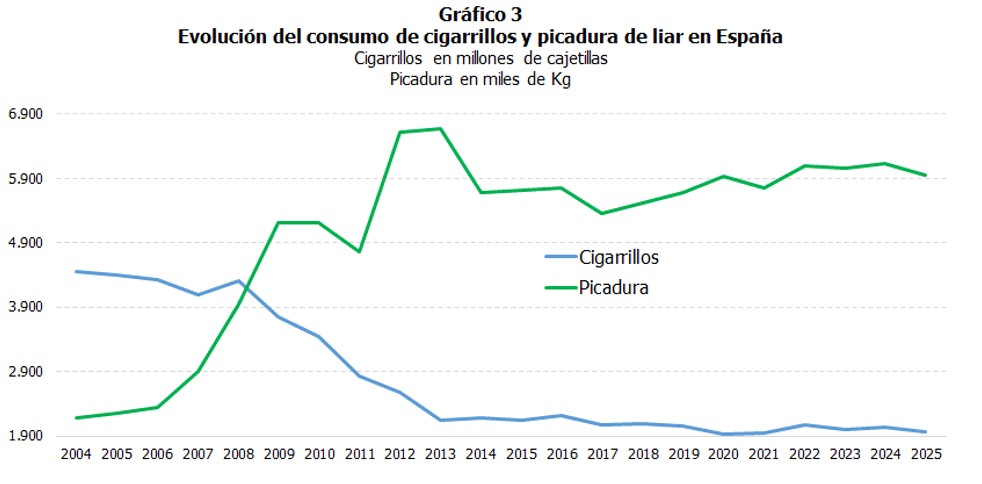

This evolution of prices, in turn, underlies the changes observed in tobacco consumption trends in Spain. Chart 3 shows how the increase in RRP The price difference between packs of tobacco and the equivalent amount of loose tobacco has led to a systematic increase in the consumption of loose tobacco, to the detriment of cigarette consumption, although both have stabilized in recent years.

The taxation of tobacco products, as with all other excise taxes, is governed by the common rules agreed upon in the EU to ensure that these taxes are applied uniformly and to the same products throughout the Community territory. The current standards of the EU The rules on the taxation of energy products and electricity are set out in Directive 2011/64/EU of the Council, of 21 June 2011, on the structure and rates of excise duty on tobacco products. This Directive establishes, among other things, minimum levels of taxation applicable to these products. In the case of cigarettes, the tax rate must include a specific part and a proportional (ad valorem) part, in addition to complying with a minimum taxation. In the case of the rest of the products, the obligation of a minimum tax is established which can be regulated in proportional or specific terms, with each country being able to choose one of these options or a combination of both. Furthermore, each country may establish minimum rates higher than those regulated in the aforementioned Directive, as is the case here. Hence, the tax structure of the different member states is not fully comparable.

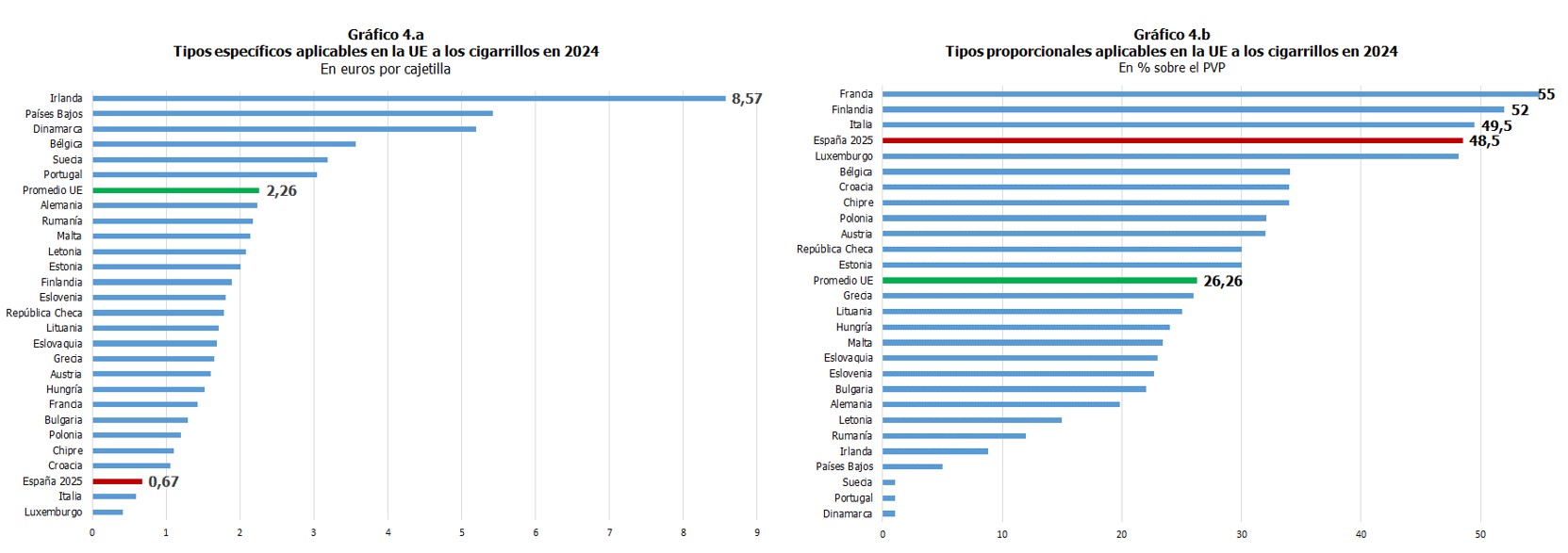

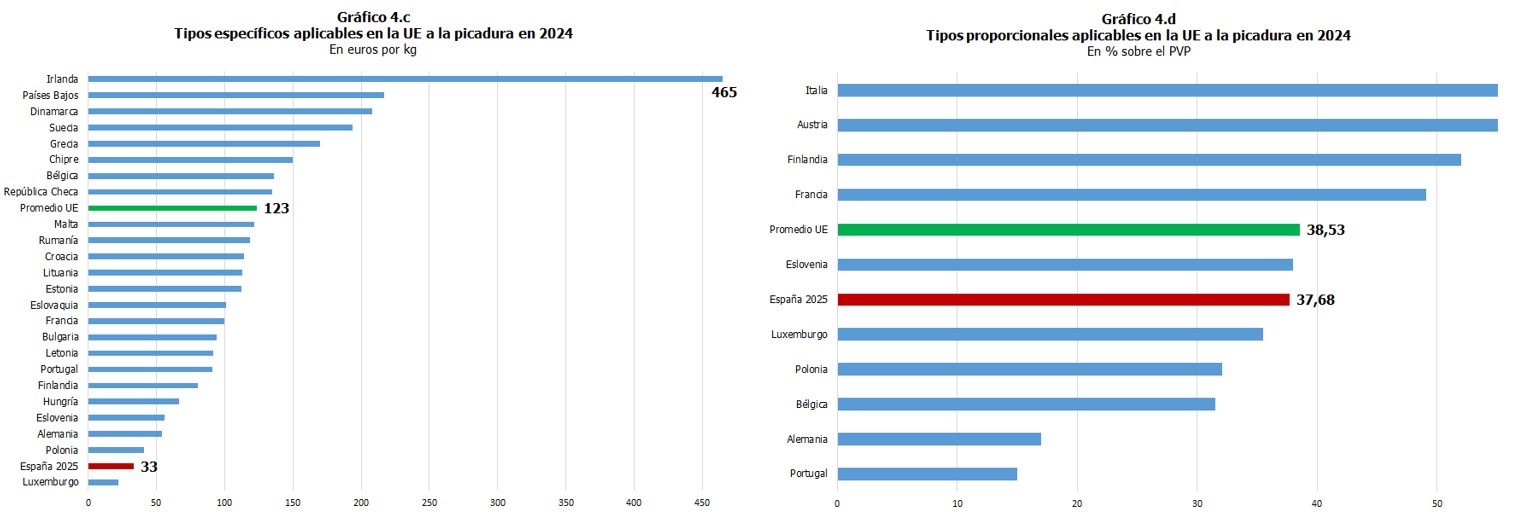

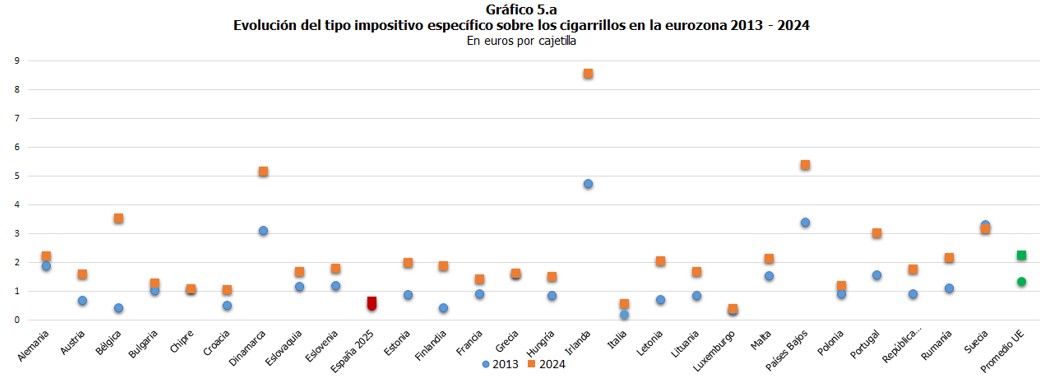

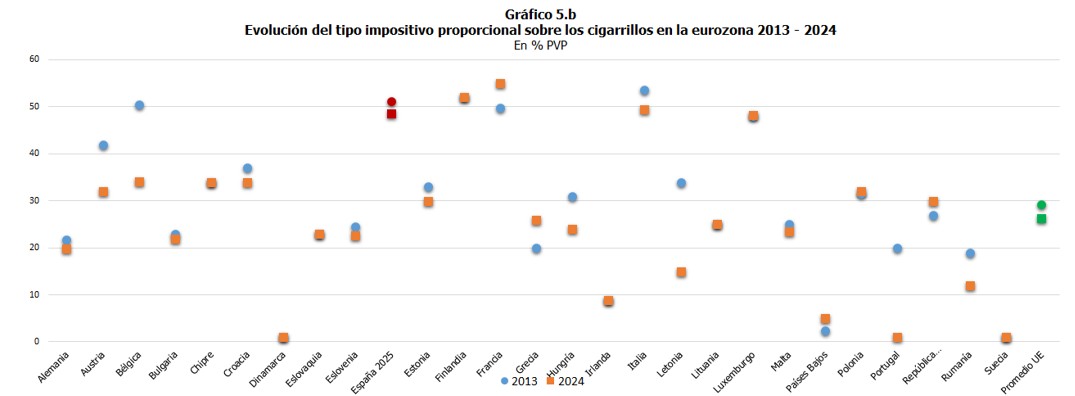

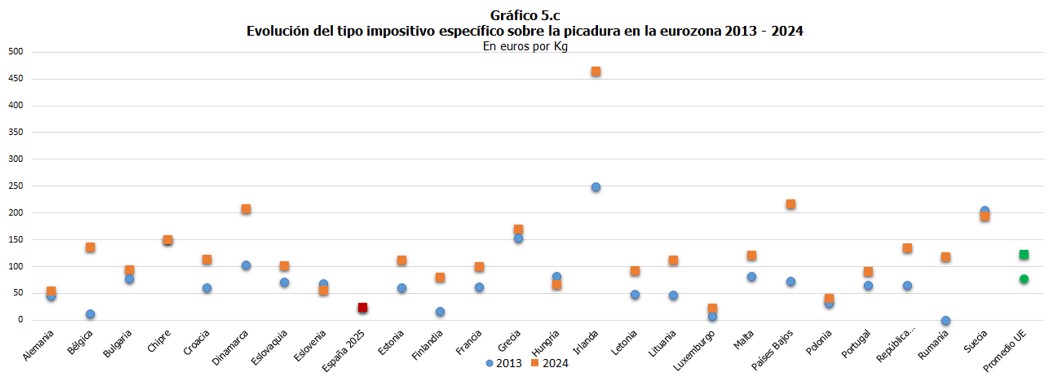

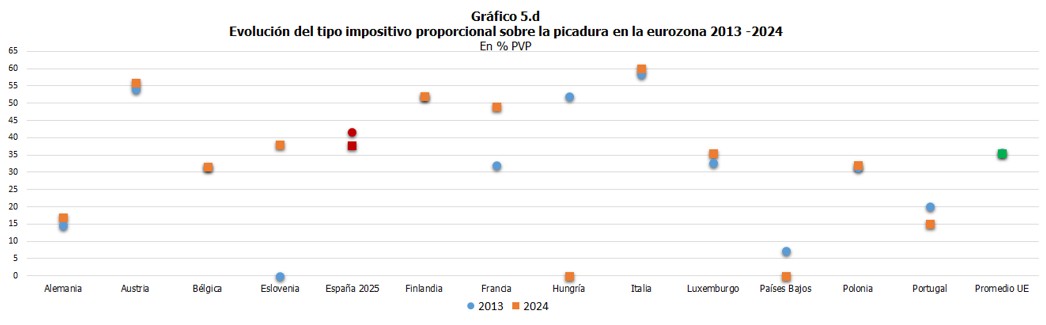

Charts 4.a and 4.d show the tax rates applicable to cigarettes and rolling tobacco in the EU, as well as the average rate. It can be observed that, in both cases, in our country specific rates lower than the average are applied. EU, while the proportional rates are among the highest in the case of cigarettes, but below average in the case of loose tobacco.

If we analyze the evolution of the rates over the last few years, specifically in the period 2013-2024, we conclude that Spain is one of the countries where the taxation on tobacco products has remained more stable.

If we analyze the evolution of the rates over the last few years, specifically in the period 2013-2024, we conclude that Spain is one of the countries where the taxation on tobacco products has remained more stable.

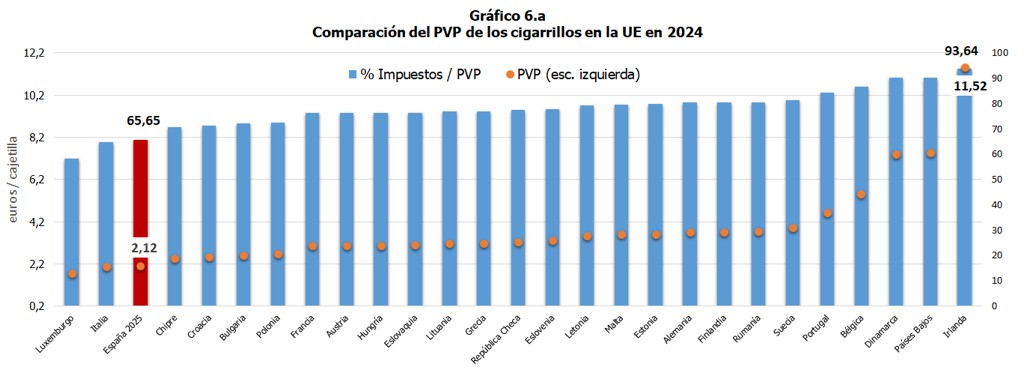

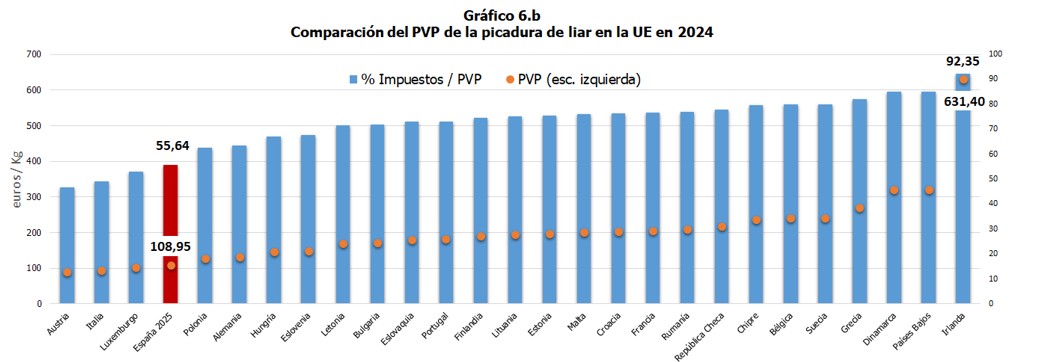

In this international comparison, one of the most relevant issues is how the existing difference in the tax structure affects RRP. To do this, the following exercise is performed: Based on the average pre-tax price of cigarettes and rolling tobacco in Spain, an approximation is calculated of RRP in each member state of the EU according to their tax rates, including the VAT, without taking into account the minimum rates of each country and without including other charges, such as, in our case, the retailer's margin or the equivalence surcharge in the VAT.

As shown in Graphs 6.ay and 6.b, the design of the tax on tobacco products in Spain, starting from the same pre-tax price, results in one of the lowest retail prices in the entire EU, both for cigarettes and for rolling tobacco. Thus, in Spain the revenue-generating capacity of these products, expressed as a percentage of the total taxes per unit of consumption, on the RRP It is also one of the lowest among the countries in our region.

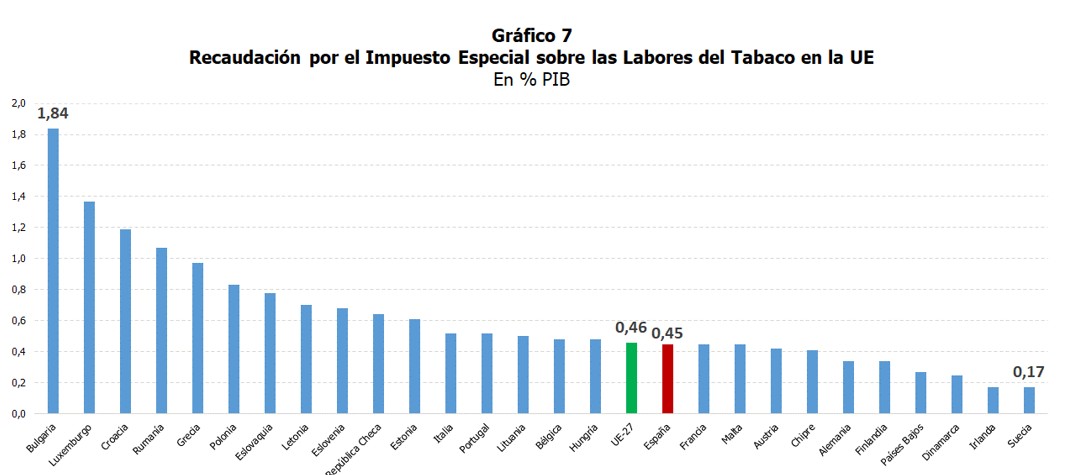

With rates close to the minimum rate and lower than the levels of many of our surrounding countries, and with hardly any changes in recent years, the result is a tax burden of the Special Tax on Tobacco Products in terms of GDP in Spain, among the lowest EU, as shown in Chart 7 with the latest available data. And this is despite the fact that the absolute consumption of cigarettes and rolling tobacco in Spain is among the highest in the world. EU.

1 The evolution of rates in excise taxes can be found in the cited report, but also, along with information on other taxes, in the file Regulatory summary which is published every month accompanying the Monthly Tax Collection Report.