Monthly Tax Revenue Reports

The Monthly Tax Revenue Report (IMRT) shows the level and monthly evolution of tax revenues managed by the Tax Agency on behalf of the State. and the Local Corporations. within the Common Tax Regime Territory.

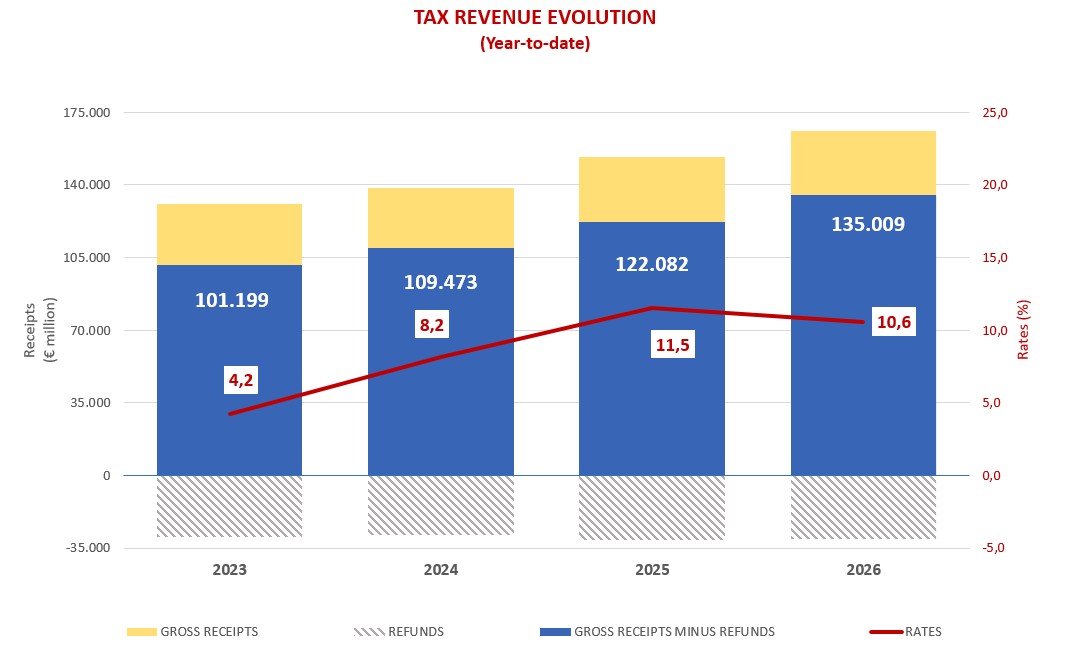

IMRT tax revenues are presented on a cash and liquid basis, i.e. as the difference between gross revenues and refunds made.

TOTAL TAX REVENUE MAY 2026

Revenues in May come mostly from the monthly self-assessments (withholdings, most of the Excise Duties and Insurance Premiums for the month of April, and VAT for the month of March) and the first quarter of Alcohol, Beer and Intermediate Products and the Tax on the Value of Electric Energy Production.

Tax revenues in May amounted to €16.45 billion, 10.4% above the same month of 2025. The growth is the result of an increase of 7.3% in gross revenues and of 0.7% in refunds paid.

In the year-to-date revenues increase by 10.6%. Gross revenues grew in that period by 8.4% and returns decreased by 1.6%. So far this year, revenues in homogeneous terms grow by 9.3%, one tenth above the estimated rate until April.

In May, the impact of the measures included in RDL 7/2026, adopted in response to the conflict in the Middle East, enlarged. In April, the impact reflected the effect of the measures in the last days of March and only in those tax forms involving the payment of the accrual of that month. May already records tax figures where the tax cut affected an entire month and, in addition, March’s VAT and the first quarter of the Tax on the Value of Electric Energy Production entered. Overall, the estimated impact in May amounts to €470 million, which adds to the preceding €113 million.

Revenue growth remained strong in May. Withholdings on earned income, which are usually the ones that contribute the most to the collection increase, given their size, moderated their growth, but other revenue showed greater dynamism, such as gross VAT (still with little impact from the rate cuts as the collection relates to March’s accrual), income from previous periods and from audit and control measures (particularly in Corporate Income Tax and VAT) and Non-Resident Income Tax (thanks to the payout of dividends in companies with high foreign participation).

Next release: 31 July (June 2026 report)