2026

Skip information indexTransactions performed during the year

(may be subject to some updates throughout the year)

The information will be displayed for the following fields:

-

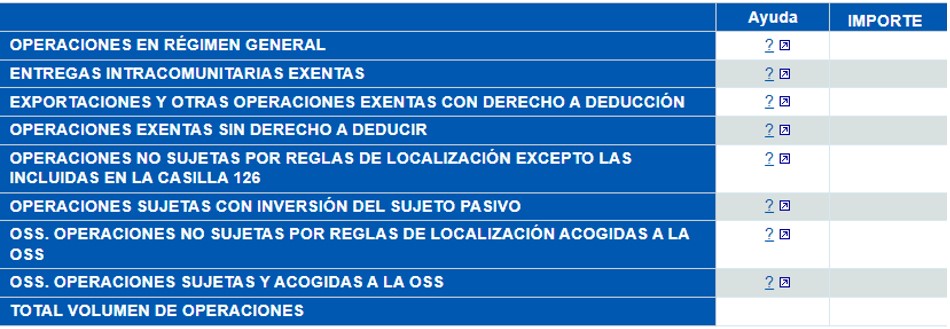

Box 80. Operations under the general regime

The calculation for this box is the sum of the following data declared by the taxpayer in their SII issued invoice register books:

- Taxable base of operations under the general regime (Code 01), leases (codes 11, 12, 13), services provided by travel agencies acting as intermediaries (code 09), successive performance operations (code 15) and operations prior to SII registration (code 16), taking into account the corrective invoices and refunds of travelers (when applicable) corresponding to the previous operations.

-

Box 81. It is NOT shown.

-

Box 93. Exempt intra-community supplies.

The calculation for this box is the sum of the following data declared by the taxpayer in their SII issued invoice register books:

- Taxable base of the operations identified exclusively as exempt operations with cause article 25 (code E5), and the amount of intra-community services provided for the year.

-

Box 94. Exports and other exempt transactions with the right to deduct.

The calculation for this box is the sum of the following data declared by the taxpayer in their SII issued invoice register books:

- Taxable base of the operations identified as subject and exempt under Article 21(E2), 22(E3), 23 and 24 (E4) as well as reason for exemption "other" (E6) or without completing anything in the "cause" box (when they are under the special export regime or the special travel agency regime) corresponding to the year.

This amount will be increased by the taxable bases corresponding to the refunds made as exports carried out under the travelers' scheme. That is, keys A5 and A6, with special regime key 02 and subject and not exempt.

-

Box 83. Exempt transactions without the right to deduction.

The calculation for this box is the sum of the following data declared by the taxpayer in their SII issued invoice register books:

- Taxable base of the operations identified as subject and exempt under Article 20(E1), as well as reason for exemption "other" (E6) or without completing anything in the "cause" box (when they do not have a special export scheme or a special scheme for travel agencies, nor is the recipient identified with an Intra-Community VAT VAT number) corresponding to the financial year

-

Box 84. Transactions not subject to location rules except those included in box 126

The calculation for this box is the sum of the following data declared by the taxpayer in their SII issued invoice register books:

- Taxable base of ALL operations not subject to location rules that are not covered by the OSS nor should be included in box 93.

-

Box 125. Transactions subject to reverse charge.

The calculation for this box is the sum of the following data declared by the taxpayer in their SII issued invoice register books:

- Taxable base for supplies of goods and services carried out in which there is reverse charge.

-

Box 126. Transactions not subject to location rules covered by special one-stop shop schemes

The calculation for this box is the sum of the following data declared by the taxpayer in their SII issued invoice register books:

- Taxable base of ALL operations not subject to location rules covered by the OSS.

-

Box 127. Operations subject to and covered by the special single window schemes

The calculation for this box is the sum of the following data declared by the taxpayer in their SII issued invoice register books:

- Taxable base of ALL operations subject to and covered by the OSS.

-

Box 128, 86, 95 and 96. These fields are not displayed.

-

Box 97. Special regime transactions involving second-hand goods, works of art, antiques and collectibles

The calculation for this box is the sum of the following data declared by the taxpayer in their SII issued invoice register books:

- Total amount, excluding Value Added Tax, of supplies of goods subject to and not exempt under the special scheme for second-hand goods, works of art, antiques and collectibles, if the method of determining the taxable base has been used by means of the profit margin of each operation.

-

Box 98. Special regime operations of travel agencies.

The calculation for this box is the sum of the following data declared by the taxpayer in their SII issued invoice register books:

- Total amount, excluding Value Added Tax, of services subject to and not exempt from VAT, provided by the taxable person during the calendar year under the special scheme for travel agencies.

-

Box 79 and 99. These fields are not displayed.

-

Box 88. Trading volume.

The result is the sum of the previous amounts.