Evolution of lottery taxation in recent years

The revenue associated with lottery prizes has particularities that are not observed in other taxes. Their behavior depends not only on the regulations, but also on the collection habits themselves and the seasonality characteristic of these draws.

The Special Tax on Prizes from Certain Lotteries and Bets has been in effect since January 1, 2013. The prizes paid by the draws of the lotteries and bets organized by the State Society Loterías y Apuestas del Estado, by the bodies or entities of the Autonomous Communities, by the Spanish Red Cross and by the games authorized to the National Organization of Spanish Blind People are subject to the tax. The tax also includes prizes from lotteries, bets and raffles organized by entities from other members of the European Union or the European Economic Area that have the same objectives as the aforementioned bodies.

The tax is due when the prize is paid. At that moment the paying entity withholds a amount. This withholding is discharge-based, so the prize recipient does not have to include its amount in the taxable base when subsequently settling the IRPFABBR.

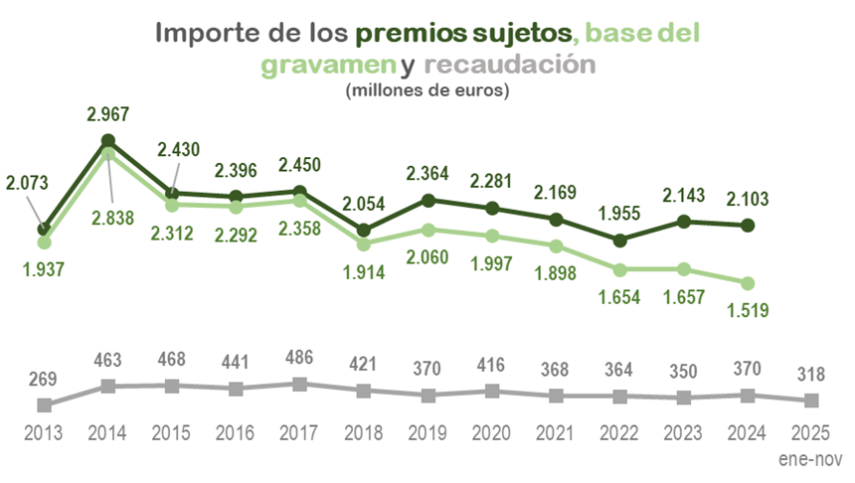

An analysis of the tax from its inception can be performed with theTable 2.7of the file that accompanies the Annual Tax Revenue ReportThe current year and monthly details of income can be tracked using the file.Statistical tables and series of the Monthly Tax Collection ReportThe following graph shows the annual evolution of the main variables.

The applicable rate has always been 20%. In contrast, the tax base has varied over time. The rule sets an exemption threshold that started at 2,500 euros and, since mid-2018, has been increasing to the current 40,000 euros. This change explains why the separation between the prizes and the base increases in the graph. This separation also varies depending on how the prizes are distributed: The smaller these are, the smaller the base and the greater the difference between the two lines.

Table 2.7 cited above also serves to clarify a doubt that often arises when analyzing the tax data in relation to other taxes. The majority of the tax is levied on individuals (since 2013, slightly over 94%) and is therefore classified under Personal Income Tax. However, what often attracts attention is the fact that there are also revenues from this source included in Corporate Income Tax. The explanation is simple: Almost all of these prizes included in the Corporate Income Tax correspond to associations and similar entities that, although not companies, are required to file the tax. In years when a major prize is won by one of these associations, clubs, fraternities, or similar organizations, it is observed that part of the revenue goes to Corporation Tax instead of being allocated to the IRPFABBR as usual.

Another issue that raises doubts is why, given that the Christmas lottery is the most popular and involves the most bets, the funds raised are not accumulated in December. To clarify this point, it is important to note that there are three relevant dates in the process: the date of the draw, the date of the prize payment (which is, in turn, the date of the tax accrual) and the date of the tax payment (which is the period in which it appears in the collection).

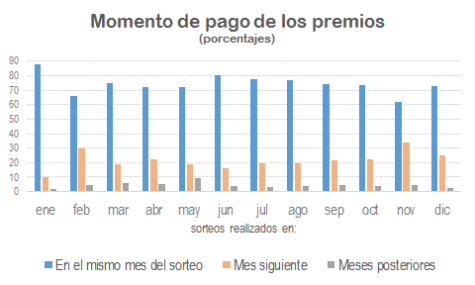

If an analysis is made of the income accrued by date of the draw, it can be seen that the income accumulates in two months, in December (on average for the period 2013-2024 they represent 39% of the total) and January (11%). In the remaining months, 5% of the total is accrued. The same conclusion is reached when analyzing revenue: 50% of the revenue is generated in January and February, and the other months account for approximately 5% in a very homogeneous way. The difference between the December-January accrual period and the January-February collection period is explained, on the one hand, by the difference between the date of the draw and the time when the prizes are paid and, on the other hand, by the difference that usually exists between the accrual time and the cash register recording time. The latter is well known and affects virtually all taxes. In contrast, the difference between the date of the draw and the time of payment of the prize is particular to this tax. Overall, on average since 2013, around three-quarters of the prizes were paid out in the same month as the draw and more than 96% between that month and the next. The following graph shows the average percentages for the draws held between 2013 and 2024.

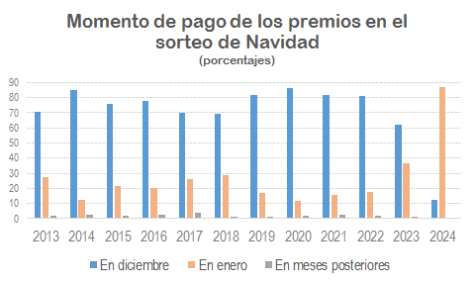

This means that the revenue seen in any given month is a mixture of prizes paid in draws held in different months. The revenue for month T does not include prizes paid for draws held in month T-1, but rather prizes paid in the previous month, regardless of the draw date. It should also be noted that, although averages are shown, the payout percentages in the month of the draw or in the following month may vary from year to year. This is precisely what happened in the Christmas draws of 2023 and 2024, a circumstance that caused a change in the relative importance of January and February in the collection of recent years. Traditionally, January's revenue exceeded that of February, but in 2024 both months had similar revenues and in 2025 February's revenue was higher than January's. The following chart, which is the same as the previous one but tailored for the Christmas lottery, perfectly illustrates the reason for these changes.

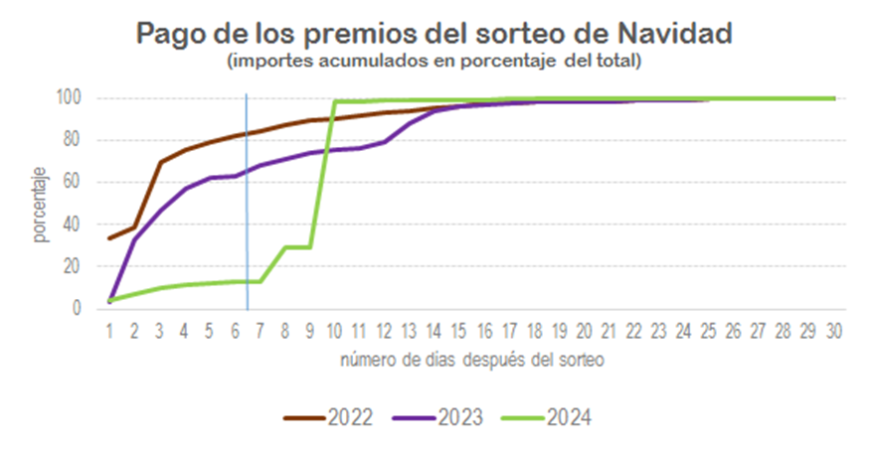

In 2023 and, especially, in 2024 the payment pattern changed. The result was a shift to February of revenue that was previously recorded in January. This effect can be seen in more detail in the last chart which shows the accumulated prize payments for the years 2022, 2023 and 2024 in the 30 working days following the draw (the vertical line indicates the end of December). As you can see, in 2024 there was a considerable group of prizes that were collected in the first days of January. However, this pattern was specific to 2024 and is not necessarily going to happen again from now on.

In summary, the evolution of the tax shows that changes in the exemption threshold and in collection patterns explain the variability observed in the base and in the monthly distribution of revenue. Although some years show occasional deviations, their overall behavior remains stable, which makes it easier to interpret their data and their contribution to total revenue.