Tax revenues in the year 2025

It was published on April 23rd Annual Tax Revenue Report corresponding to 2025. The report is an analysis of the collection behavior throughout 2025, an analysis that is carried out month by month during the course of the year in the monthly reports. The annual report allows for a deeper and more detailed study of the ultimate reasons for revenue growth by providing the economic information behind the revenue flows. The publication is completed with several files that include all the variables used in the analysis, in addition to other additional information (salary and personal income tax distributions, allocation to the Catholic Church and social purposes,…) and a set of notes that develop some specific aspects relevant to understanding the evolution of the collection.

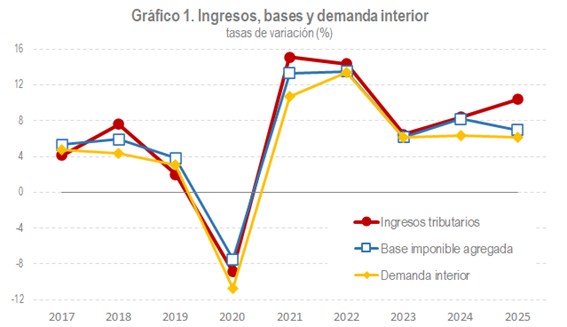

In 2025 tax revenues amounted to €325.36 billion, 10.4% above those recorded in 2024. The increase in revenue in 2025 is explained by the increase in tax bases (estimated at 7%) and the positive impact of regulatory and management measures (7,820 million, 2.7 points of the growth in revenue). This second factor is clearly seen in Chart 1, where bases and revenue are separated in 2025. Meanwhile, domestic demand in the National Accounts, which appears in the graph as the most appropriate aggregate indicator of economic activity to approximate the evolution of tax revenue, returned to its baseline levels after its separation in 2024.

The aggregate tax base of the main taxes grew by 7% in 2025, below the 8.2% estimated for 2024. The moderation is explained by the evolution of the bases linked to income, which showed a tendency to slow down, accentuated by the intense growth in 2024 of income from movable capital and income from economic activities, as well as by the rebound, linked to regulatory changes, that occurred then in the consolidated base of Corporate Income Tax. Together, these bases grew by 8%, down from 11.2% in 2024, and slightly above the rise in 2023. In contrast, the bases linked to spending improved compared to the previous year, with an increase of 5.5% compared to 4% in 2024, mainly due to the recovery of the value of consumption subject to Special Taxes, although the growth of final spending subject to VAT also exceeded that observed in 2024 (6.1% and 5.7%, respectively).

The positive impact of regulatory and management changes is estimated at €7.82 billion. The total effect includes a negative impact of €3 billion from extraordinary receipts and refunds (if added, collection would grow by 11.4%, a rate similar to that of homogeneous revenue). The remaining measures, which resulted in net additional revenue of 10,798 million, were primarily the result of measures in Corporate Income Tax, the return to full normality in VAT (the recovery of rates on energy products and basic food) and in taxes on electricity, the new taxes (on the Interest Margin and Commissions of Certain Financial Entities and on Liquids for Electronic Cigarettes) and the increase in the rate in the Tax on Tobacco Products.

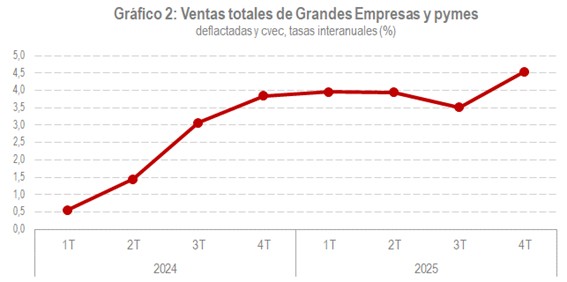

Economic activity showed the same pattern of moderation as the tax bases. The volume index of GDP, which measures real growth, increased by 2.8% in 2025, seven tenths less than in 2024. In nominal terms the slowdown was similar: GDP at current prices grew by 5.8% after 6.4% in 2024. Fiscal indicators (daily sales, monthly sales of Large Companies to the constant population and quarterly sales of Large Companies and corporate SMEs) also moderated in the middle part of the year, although in the last stretch an improvement was observed and overall the rates were higher than those recorded in 2024. The indicator that best expresses this trajectory is the Quarterly sales of large companies and SMEs, representative of what happens in more than a million companies and, therefore, the one with the greatest coverage of the statistical system. This is shown in Chart 2, which includes the year-on-year rates of sales deflated and corrected for seasonality and calendar effects (cvec).

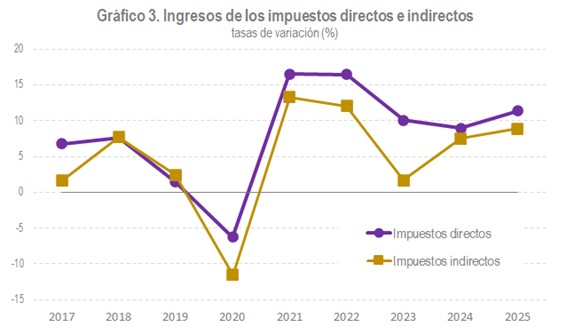

The 10.4% growth in revenue in 2025 originated from an 11.4% increase in direct taxes and an 8.9% increase in the sum of indirect taxes, fees and other income.

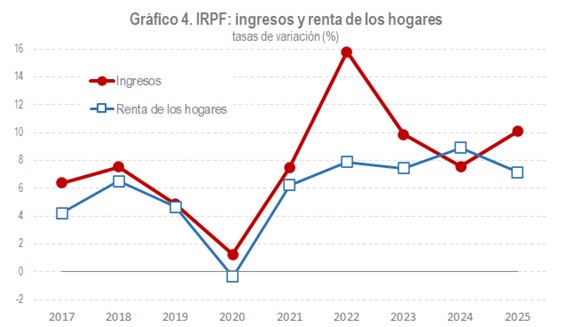

Personal income tax revenues increased by 10.1% in 2025. Household income grew by 7.2%, an increase which, together with the change in the rate, explains the notable increase in the tax, even with the negative impact that the refunds to mutual members had in 2025 (2,717 million were refunded, almost 2,200 million more than in 2024). The elements that made the greatest contribution to income growth were the withholdings on employment income and the gross result of the annual tax return. Withholdings on income from work and economic activities grew by 8.7%, with an increase of 8.9% in the private sector and 8.1% in income from public salaries and pensions. The second element, the gross result of the annual declaration (mostly corresponding to the 2024 financial year), increased by 26%. We have to deduct about 300 million from the postponement of the payment of the second installment of the 2023 declaration of the taxpayers of the province of Valencia, affected by the DANA, which was paid at the beginning of 2025. Even so, the increase would be higher than 22%. The reason for this high growth was the sharp increase in income not fully subject to withholding or advance payments (capital gains, income from movable and immovable capital and income from economic activities) that occurred in the 2024 declaration filed in 2025. Other concepts, such as installment payments or withholdings for capital gains in investment funds, also experienced growth exceeding 10%, although they do not have as much weight in the collection.

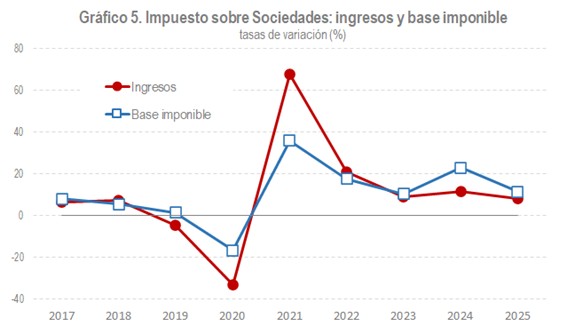

Corporate tax revenues grew by 8.1%. The evolution of the tax is determined by the behavior of the installment payments, linked to the profits generated in the year. Payments in 2025 grew by 8.1%, while the profits of large companies and groups grew by 6.1%. The difference in favor of the payments is explained by the limitation on the consolidation of losses in the groups, in force in the 2025 payments, but not in those of 2024 (in that year the measure only affected the annual fee). As with the Personal Income Tax, the gross result of the annual declaration (corresponding to the 2024 financial year) also had a high growth of 16.9%, although in this case with a part due to the positive impacts of regulatory measures, especially in groups. This increase in gross revenue was offset by a similarly sharp increase in refunds, mainly for two reasons: the large amounts of refunds from the previous campaign (fiscal year 2023) that were made in the first months of 2025, and the extraordinary refunds linked to the ruling on the limitation of negative tax bases of Royal Decree-Law 3/2016 (1,432 million).

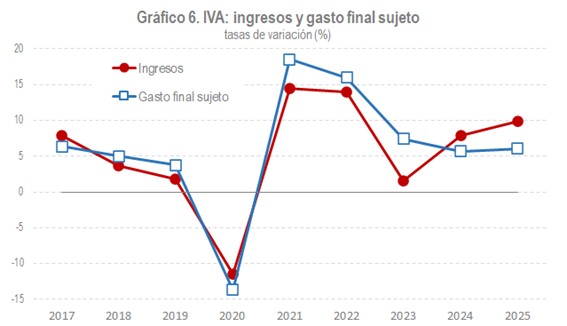

Regarding indirect taxes, the growth in VAT revenue was 9.9%. It is estimated that final taxable expenditure grew by 6.1%. To this must be added the rise in the average rate (3.7%) resulting from the return to normal rates applied to energy and basic food products. The adjustments between accrual and cash, and, in particular, the income from deferrals, would explain the small additional growth in revenue.

Finally, revenue from Special Taxes grew by 4.3%. In this case too, there was a positive impact from the regulatory measures; Specifically, the full reinstatement of the Electricity Tax rate, the increase in the Tobacco Products Tax rate, and the new Electronic Cigarette Liquids Tax. Together they contributed an income of 831 million; Without them, revenue from Special Taxes would have only grown by 0.6%.