Deductions for energy efficiency

Find out how you can deduct the amounts paid for this type of work from your Income Tax Return

Deduction for works to improve the consumption of non-renewable primary energy

Housing in which the works can be carried out:

The taxpayer's main residence or any other property owned by the taxpayer that is rented out for use as a residence or is expected to be rented, provided that, in the latter case, the residence is rented out before December 31, 2027.

However, the part of the work carried out on parking spaces, storage rooms, gardens, parks, swimming pools and sports facilities and other similar elements, as well as the part of the housing affected by an economic activity, is not eligible for this.

Works that are not eligible:

Those that have reduced the non-renewable primary energy consumption indicator by at least 30 per cent, or achieve an improvement in the housing’s energy rating to obtain energy class "A" or "B" on the same rating scale.

These points must be accredited by means of the energy efficiency certificate for the housing issued by the competent technician after the works have been carried out, with respect to the one issued before the start of the works, with a maximum of two years. The certificates must be issued and registered in accordance with the provisions of Royal Decree 390/2021, of June 1, which approves the basic procedure for the certification of the energy efficiency of buildings.

Conducted from October 6, 2021 to December 31, 2025.

Deduction base:

Amounts paid for the works from October 6, 2021 to December 31, 2025 qualify for the deduction.

Maximum €7,500.

Tax period during which this applies:

The one in which the energy performance certificate was issued after the work was carried out. Therefore, in order to apply the deduction in IRPF 2025 the certificate must be issued in 2025.

Deduction percentage: 40%

COMPLETING BOXES ON RENTA WEB

LOCATION OF DATA IN THE ISSUED CERTIFICATE

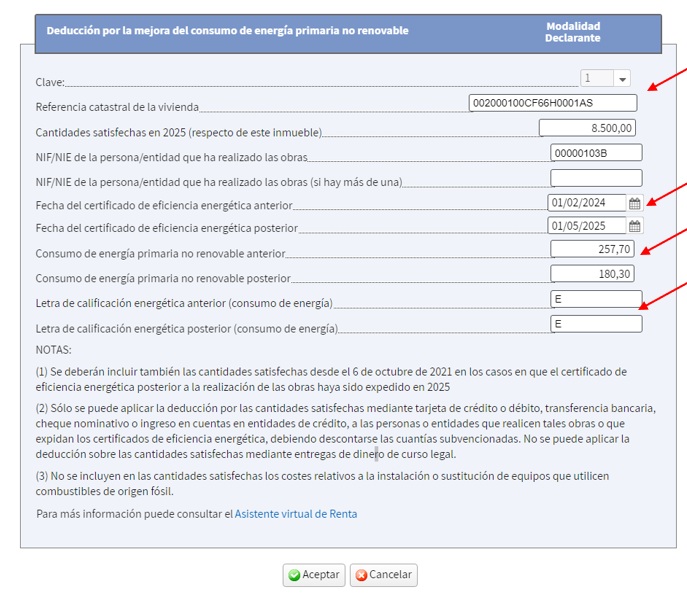

The data to be entered in the energy efficiency certificates are:

-

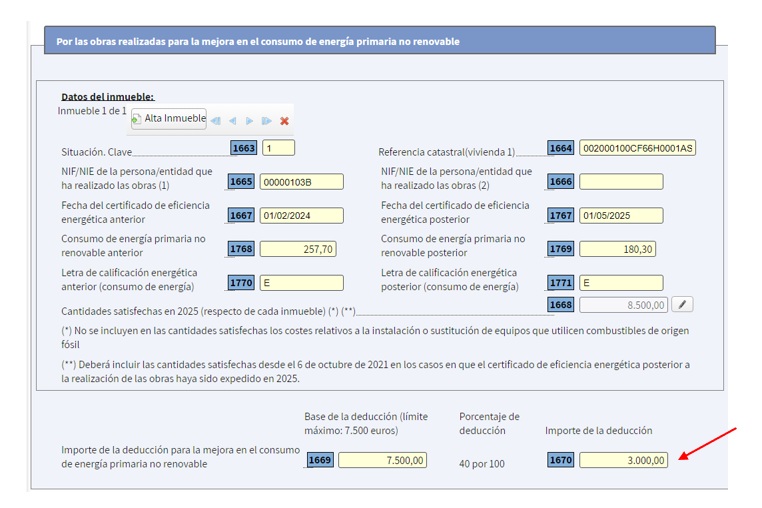

Land registry reference number

-

Date of each of the certificates

-

Non-renewable primary energy consumption of each of the certificates

-

Energy rating letter for each of the certificates

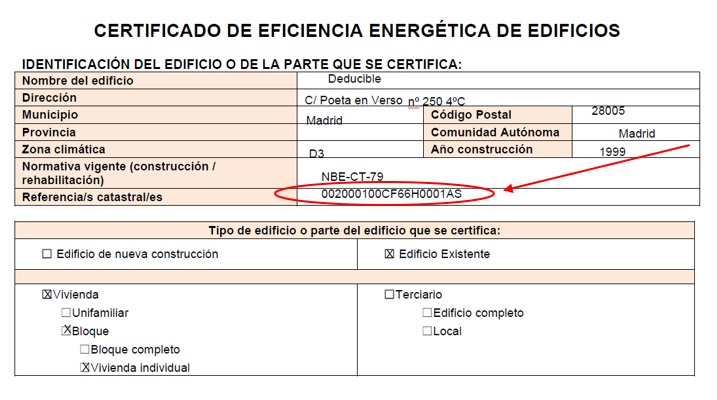

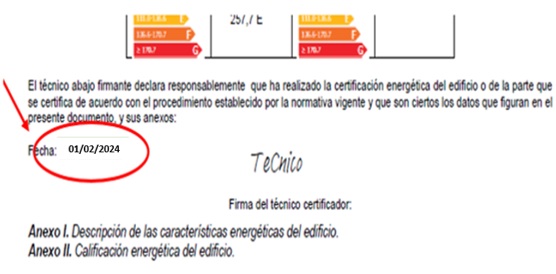

The cadastral reference and the date of the certificate appear on the first page of the energy efficiency certificate, where the certificate's identification data is listed.

The cadastral reference at the top of this page 1.

The date appears at the bottom of the page of each of the certificates:

In our example, the date of the first certificate is 01/02/2024 and the date of the second is 01/05/2025.

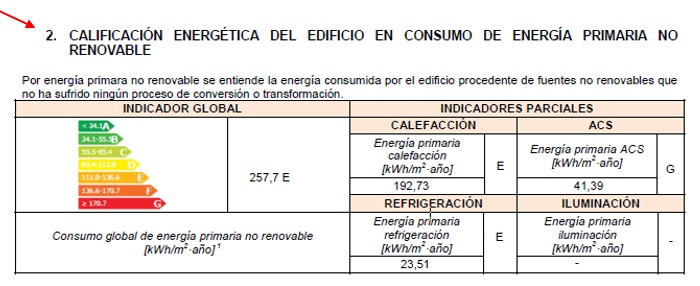

The energy rating of the home in non-renewable primary energy consumption is listed in section 2 of Annex II of each of the Energy Efficiency Certificates:

First certificate, in the central part of the page:

In our example, the non-renewable energy consumption indicator of the first certificate is 257.7 and the energy class is E. Both data are recorded in Renta Web.

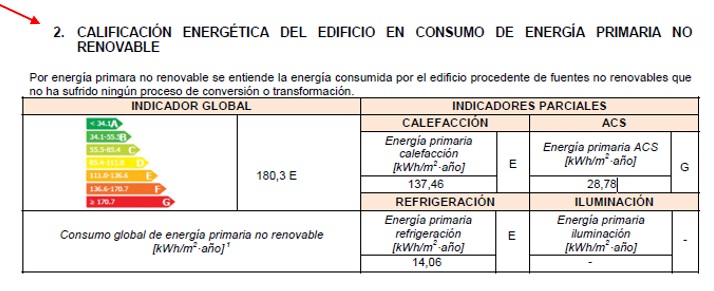

Second certificate, in the central part of the page:

In our example, the non-renewable energy consumption indicator of the second certificate is 180.3 and the energy class is E. Both data are recorded in Renta Web.

Although efficiency has not improved by moving up a range and reaching at least B, the consumption indicator has been reduced by at least 30%.

Therefore, by meeting either of the two requirements, Renta Web applies the deduction, in this case, since the maximum base per taxpayer is €7,500, €7,500 x 40% = €3,000.