Deductions for energy efficiency

Find out how you can deduct the amounts paid for this type of work from your Income Tax Return

Deduction for energy rehabilitation works

Buildings on which the works can be carried out:

Housing owned by the taxpayer - located in buildings of predominantly residential use - and parking spaces and storage rooms acquired with these. However, the part of the housing used for economic activities is not eligible.

Works that are not eligible:

Those that have reduced the consumption of non-renewable primary energy by at least 30 per cent or improved the building’s energy rating to energy class "A" or "B" on the same rating scale.

These points must be accredited by means of the energy efficiency certificate for the housing issued by the competent technician after the works have been carried out, with respect to the one issued before the start of the works, with a maximum of two years. The certificates must be issued and registered in accordance with the provisions of Royal Decree 390/2021, of June 1, which approves the basic procedure for the certification of the energy efficiency of buildings.

Conducted from October 6, 2021 to December 31, 2025.

Tax periods during which this applies:

In principle, it can be applied in 2021, 2022, 2023, 2024 and 2025. However, in order to be able to apply the deduction, the energy efficiency certificate must have been issued after the works have been carried out. These certificates must be issued before January 1, 2026.

Annual deduction base:

-

When the certificate has been issued during the tax period:

Amounts paid from 6 October 2021 until the end of the tax period.

-

When the certificate was issued during a previous tax period:

The amounts paid during the year.

Maximum base €5,000 per year.

The amounts paid that have not been deducted because they exceed the maximum annual deduction base may be deducted, with the same limit, during the following four financial years, although in no case may the accumulated deduction base exceed 15,000 euros.

In the case of work carried out by a community of owners, the amount that may form the basis of the deduction for each taxpayer will be determined by the result of applying the coefficient of participation that he/she has in the community of owners to the amounts paid by the community of owners.

Deduction percentage: 60%

COMPLETING BOXES ON RENTA WEB

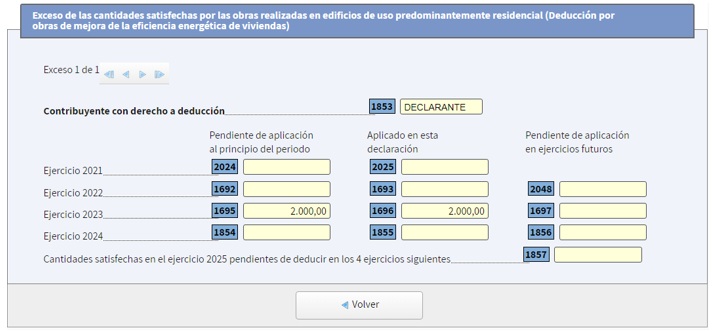

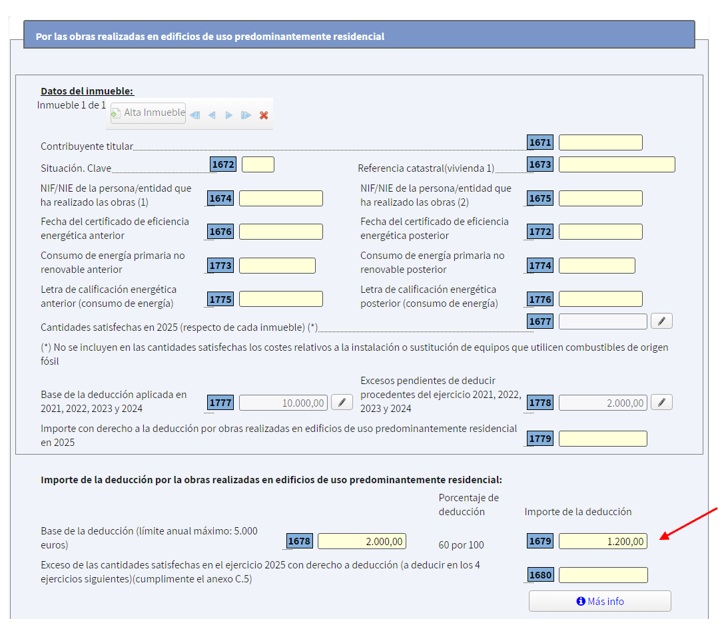

In this example, the energy efficiency certificate after the completion of the works is from 2023. The amounts paid from October 6, 2021 to December 31, 2023 were €12,000.

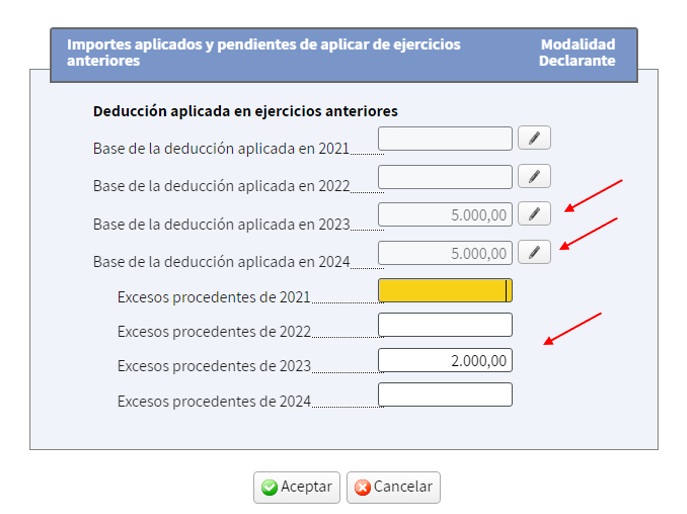

Since the date of the energy efficiency certificate, issued after the completion of the works, is 2023, the taxpayer claimed the deduction in their 2023 Personal Income Tax return for the amounts paid, up to the maximum annual deduction base (€5,000), leaving €7,000 pending deduction, of which €5,000 were applied in the tax return. IRPFABBR 2024. Consequently, it has some excess amounts pending deduction from 2023 of €2,000 that will be applied in 2025.

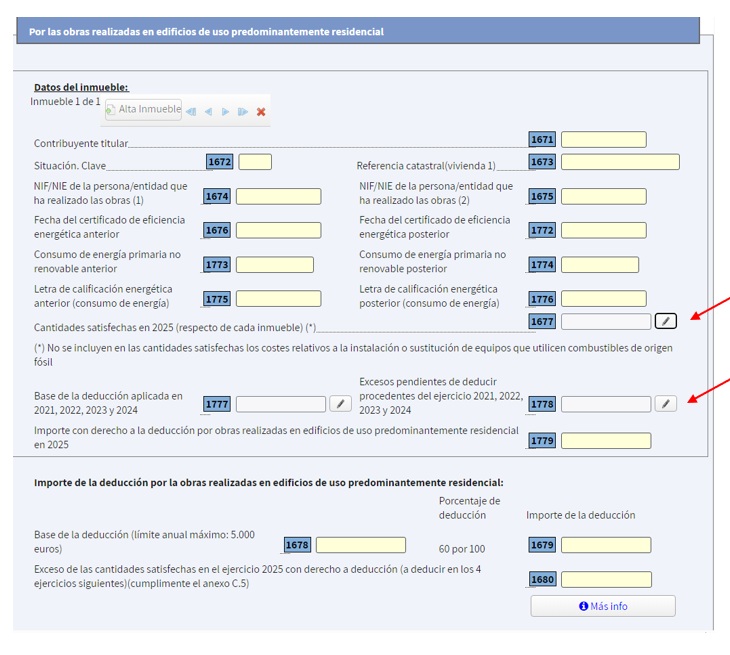

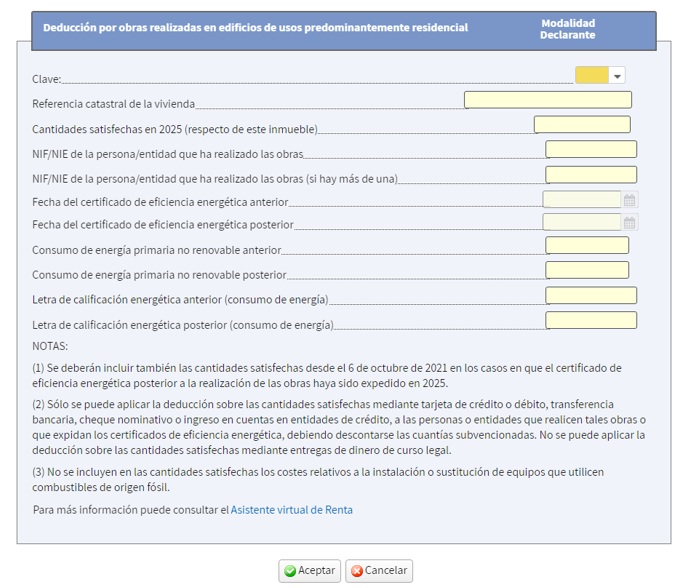

Since no amount was paid in the 2025 tax year, the window that opens from box 1677 should not be completed (this window will have been filled in the tax return for the year in which the amounts were paid).

The applied bases and the excess amounts pending deduction will be incorporated in the window that opens from boxes 1777 and 1778.

In the window corresponding to the deduction applied in each of the years:

In this exercise, the €2,000 pending application from 2023 will be applied.

Clicking on “More info” displays the amounts applied in this exercise.