Reduction for income from artistic activities obtained in an exceptional manner

Learn how this reduction applies to Income Tax 2025 for an employee or through an economic activity

Reduction for income from artistic activities obtained as an employee

This reduction will apply to the gross employment income obtained in the tax period to which the reduction for obtaining irregular income provided for in article 18.2 of the LIRPF does not apply.

It will apply in the following cases:

-

Preparation of literary, artistic or scientific works provided that the right to their exploitation is transferred, cases referred to in article 17.2.d) of the LIRPF.

-

The special employment relationship of artists who carry out their activity in the performing, audiovisual and musical arts, as well as of people who carry out technical or auxiliary activities necessary for the development of their activity.

Thus, when the total income obtained in 2025 exceeds 130% of the average amount of income imputed in 2022, 2023 and 2024, the aforementioned excess will be reduced by 30%.

It should be noted that the amount to which this reduction will be applied cannot exceed €150,000 per year.

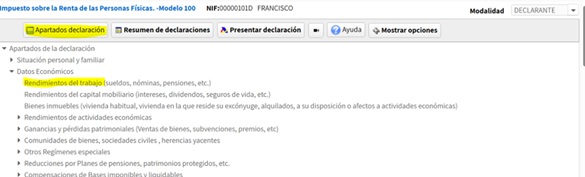

In Renta Web, the amounts of the total income obtained in the years 2022, 2023 and 2024 will be filled in so that the program can perform the calculation. To do this, you will access the employment income section from the “Declaration sections”:

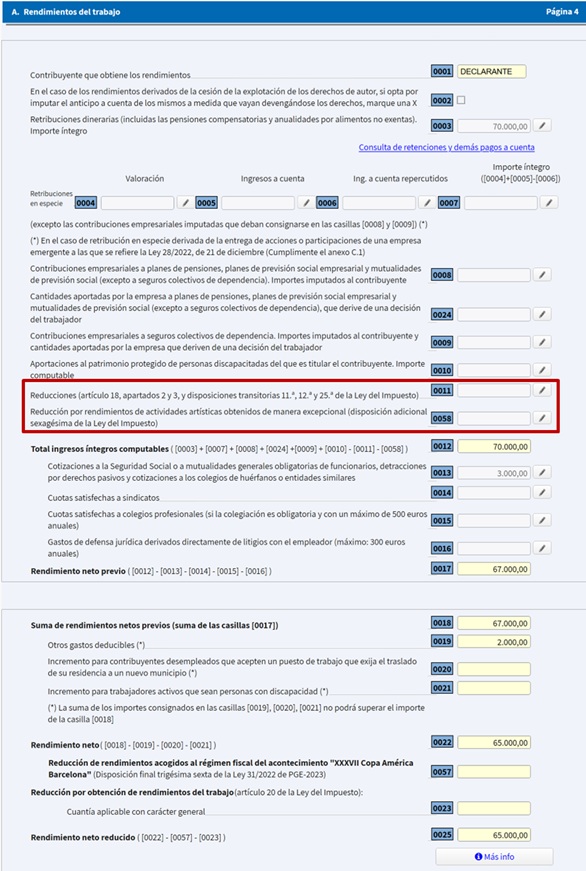

In this case, some income from work already appears. Let's assume that they have all been obtained by carrying out this type of activity.

To include the reduction, access the interior of box 0058:

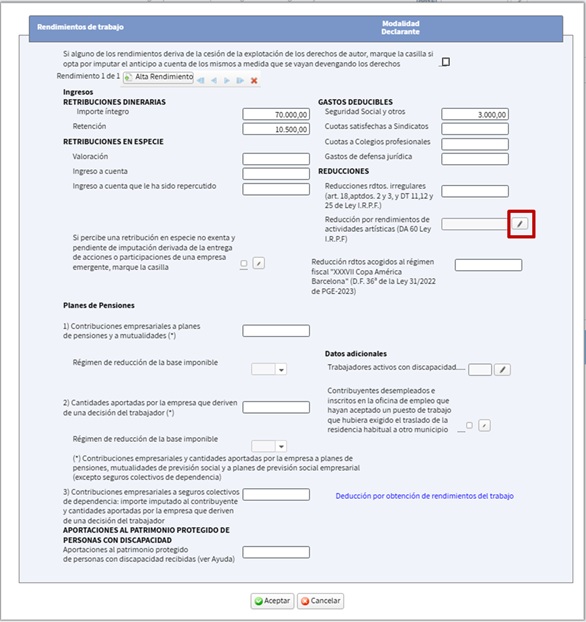

The following window will open and the reduction will be selected:

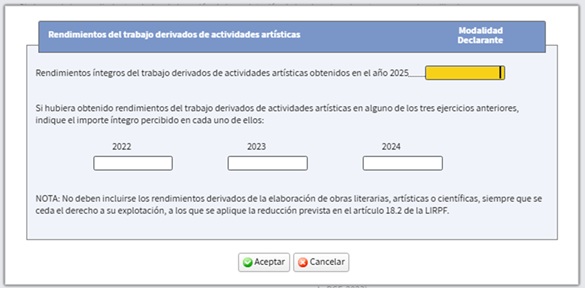

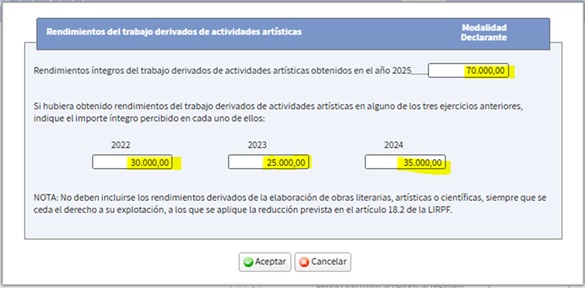

The requested amounts will be included on the next screen:

Assuming that all employment income obtained in the year (€70,000) comes from artistic activity and that the income obtained in 2022, 2023 and 2024 from that activity was €30,000, €25,000 and €35,000 respectively:

So after pressing “Accept”, the corresponding reduction will appear when applicable. In this case, it amounts to €9,300 because the total income for 2025 exceeds 130% of the average amount of income imputed in the three previous tax periods:

The calculation was performed as follows:

The average amount of imputed income in 2022, 2023 and 2024 is determined: €30,000: (30,000 + 25,000 + 35,000) / 3 = €30,000.

130% of the average amount is obtained: €39,000 (130% of 30,000 = 39,000).

Thus, since the total income for 2025 (€70,000) is greater than 130% of the average amount of income for the years 2022, 2023 and 2024 (€39,000), the 30% reduction will be applied to the excess.

The excess is €31,000 (70,000 – 39,000 = 31,000).

Amount of the reduction: 30% of 31,000 = €9,300, an amount reflected in box 0058 above.

Additional Information:

The full amount of employment income to be reported in relation to the years 2022, 2023 and 2024 can be obtained from the declarations of those years and will be the amount shown in box 0012 “Total total computable income”. In the event that a joint return has been filed, only those corresponding to the taxpayer who received them will be taken into account.

However, if in the 2022, 2023 and 2024 tax years income from work other than that obtained from artistic activities has been received, of the amount shown in box 0012 only the income from artistic activities should be taken into account.