Reduction for income from artistic activities obtained in an exceptional manner

Learn how this reduction applies to Income Tax 2025 for an employee or through an economic activity

Reduction for income from artistic activities obtained by carrying out an economic activity

It will apply to the net income from economic activities obtained in the tax period to which the reduction for irregularity provided for in article 32.1 of the LIRPF does not apply, derived from:

-

Activities included in groups 851, 852, 853, 861, 862, 864 and 869 of section two and in groups 01, 02, 03 and 05 of section three of the Economic Activities Tax Rates.

The activities of the groups in the second section are:

-

Group 851. Technical representatives of the show

-

Group 852. Bullfighting agents and representatives.

-

Group 853. Artist placement agents.

-

Group 861. Painters, Sculptors, Ceramists, Craftsmen, Engravers, Fallas Artists and similar artists.

-

Group 862. Art restorers.

-

Group 864. Writers and screenwriters.

-

Group 869. Other professionals related to artistic and cultural activities not classified in section three.

And the groups of the third section:

-

Group 01. Activities related to film, theater and circus.

-

Group 02. Activities related to dance.

-

Group 03. Music-related activities.

-

Group 05. Activities related to bullfighting shows.

-

-

The provision of professional services which, by its nature, if carried out on behalf of others, would be included in the scope of application of the special employment relationship of artists who carry out their activity in the performing, audiovisual and musical arts, as well as of the people who carry out technical or auxiliary activities necessary for the development of said activity.

The reduction will be applied if the 2025 returns exceed 130% of the average amount of net returns imputed in 2022, 2023 and 2024. The reduction will be 30% of the aforementioned excess.

The amount to which this reduction will be applied may not exceed €150,000 per year.

This reduction will be applied after the reductions for the exercise of certain economic activities and for the start of an economic activity provided for in sections 2 and 3 of article 32 LIRPF.

In Renta Web you will access:

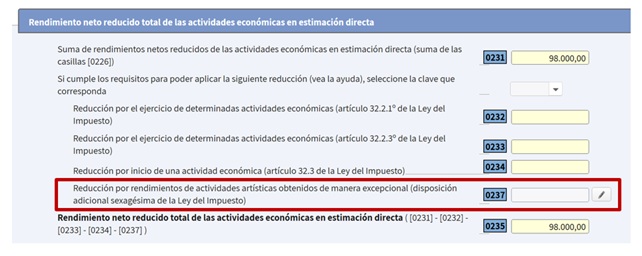

And once the economic data relating to the activity has been included in the declaration, it will be completed from box 0237:

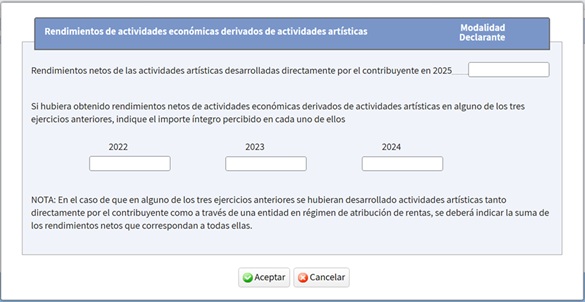

Accessing the interior:

The amount of net income obtained from 2022 to 2025 will have to be filled in.

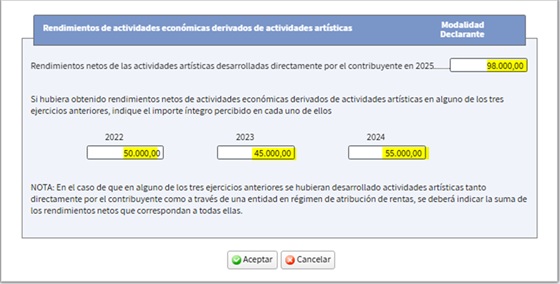

Let's assume that in each of the three previous exercises the following results were obtained: €50,000 in 2022, €45,000 in 2023 and €55,000 in 2024 and in 2025 an amount of €98,000:

After completion, the reduction is calculated, where applicable; in this case it is €9,900:

The average amount of imputed income in 2022, 2023 and 2024 amounts to €50,000: (50,000 + 45,000 + 55,000) / 3 = 50,000 €.

130% of the average amount is €65,000 (130% of 50,000 = 65,000).

Since the net returns for 2025 (€98,000) are higher than 130% of the average amount of the previous three years (€65,000), the 30% reduction will be applied to the excess.

The excess is €33,000 (98,000 – 65,000 = 33,000).

Amount of the reduction: 30% of 33,000 = €9,900, an amount that is reflected in box 0235 above.

Additional Information:

The amount to be entered in relation to the 2022, 2023 and 2024 tax years can be obtained from box 0224 of the tax returns for those years.

If you have carried out several artistic activities, you must reflect the sum of boxes 0224 for each of the activities.

Deductible expenses that are common to other income from economic activities other than artistic ones will be prorated proportionally based on the amount of the different gross income from economic activities computed in said years.