2026

Skip information indexSettlement data

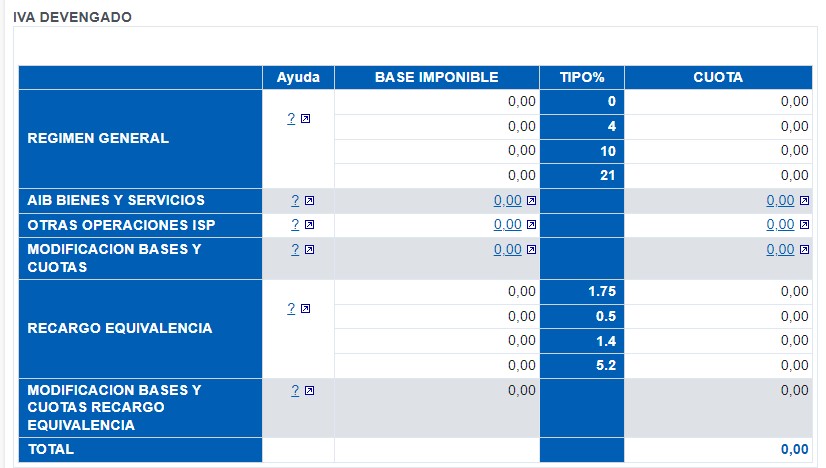

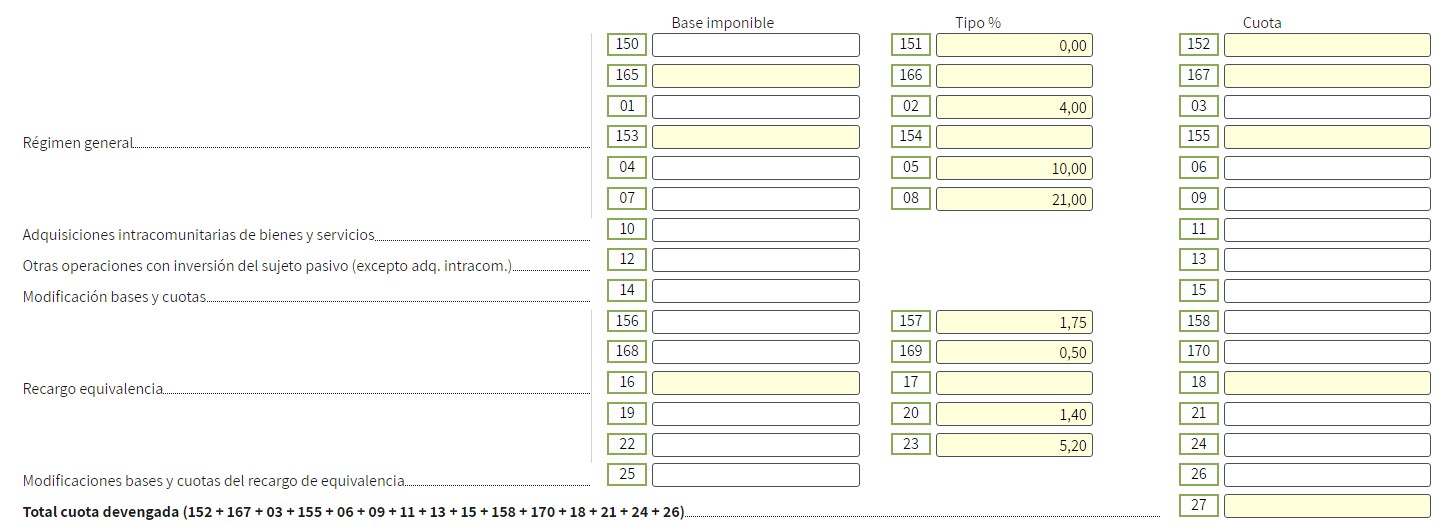

The format of the LL.AA. for the accrued VAT which coincides with that of model 303 is the following:

As you can see, there must be a NOTE in each of the categories.

The content is as follows:

GENERAL REGIME

"Taxable base and the fee for deliveries of goods and services subject to and not exempt without reverse charge carried out by the taxpayer in the period subject to settlement, differentiated by the tax rate applied."

You can view the details of the calculations performed in the link available in the section located on the right margin, click on "VAT accrued".

You can view the corresponding invoices in the link that exists in the tax fee for the Added Books.

INTRA-COMMUNITY ACQUISITIONS OF GOODS AND SERVICES

"Taxable bases and the corresponding fees for the total intra-community acquisitions of goods and services subject to and not exempt from tax carried out in the settlement period."

You can view the details of the calculations performed in the link available in the section located on the right margin, click on "VAT accrued".

If in the period there are intra-community acquisitions made by taxable persons under the equivalence surcharge in addition to those under the general regime, the taxable base of the equivalence surcharge must be included manually, adding to the amount shown in the Pre303 in the boxes of taxable base of the equivalence surcharge.

You can view the corresponding invoices in the link that exists in the tax fee for the Added Books.

OTHER TRANSACTIONS WITH REVERSE CHARGE (except acquisitions) Intracom)

"Taxable bases and accrued fees in the settlement period as a result of investment operations of the taxable person, when they originate from operations other than those recorded in boxes 10 and 11."

You can view the details of the calculations performed in the link available in the section located on the right margin, click on "VAT accrued".

You can view the corresponding invoices in the link that exists in the tax fee for the Added Books.

MODIFICATION OF BASES AND FEES

"The modification of taxable bases and quotas of operations in which any of the causes provided for in article 80 of the LIVA occur, as well as any other modification of bases and quotas, will be recorded with the corresponding sign."

You can view the details of the calculations performed in the link available in the section located on the right margin, click on "VAT accrued".

You can view the corresponding invoices in the link that exists in the tax fee for the Added Books.

EQUIVALENCE SURCHARGE

"Taxable base and the fee for taxable transactions subject to the equivalence surcharge carried out by the taxpayer in the period subject to settlement, differentiated by the tax rate applied."

You can view the details of the calculations performed in the link available in the section located on the right margin, click on "VAT accrued".

You can view the corresponding invoices in the link that exists in the tax fee for the Added Books.

MODIFICATIONS TO THE BASES AND RATES OF THE EQUIVALENCE SURCHARGE

"The modification of taxable bases and equivalence surcharge of operations in which any of the causes provided for in article 80 of the LIVA occur, as well as any other modification of bases and quotas, will be recorded with the corresponding sign."

You can see the details of the calculations performed in the link on the right.

You can view the corresponding invoices in the link that exists in the tax fee for the Added Books.

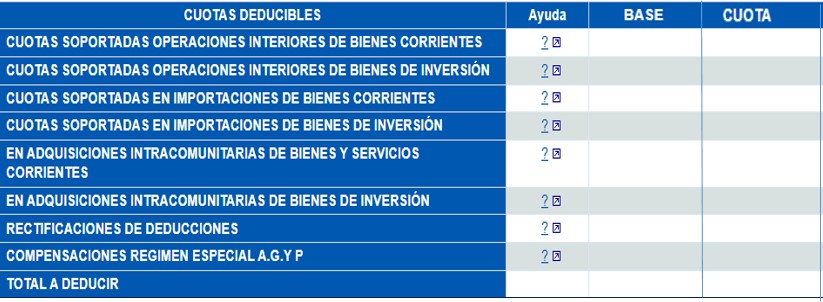

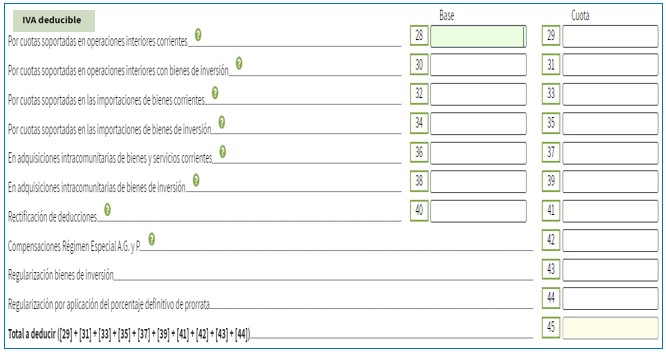

The format of the LL.AA. for deductible VATwhich coincides with that of model 303 is the following:

There will be a NOTE in each of the categories.

The content is as follows:

FEES PAID ON CURRENT DOMESTIC TRANSACTIONS

"Taxable bases and deductible input VAT for domestic transactions involving current goods."

If the taxpayer has not indicated in the invoice register that they are investment goods, the total taxable bases and deductible input VAT for domestic transactions will appear in this box.

You can view the details of the calculations performed in the link available in the section located on the right margin, click on "VAT deductible".

If there are intra-community acquisitions at a zero rate during the period, the amount is not displayed in box 28 in the Pre303 form because the deductible amount is zero.

You can view the corresponding invoices via the link provided in the section for the tax on the Aggregated Books.

TAXES PAID ON DOMESTIC TRANSACTIONS IN INVESTMENT GOODS

"Taxable bases and deductible input VAT for domestic transactions involving capital goods."

If the taxpayer has not indicated in the invoice register that they are investment goods, the total taxable bases and deductible input VAT for domestic transactions will appear in this box.

You can view the details of the calculations performed in the link available in the section located on the right margin, click on "VAT deductible".

You can view the corresponding invoices in the link that exists in the tax fee for the Added Books.

Duties borne on imports of current goods

"Taxable bases and deductible input VAT for imports of capital goods."

If the taxpayer has not indicated in the invoice register that the goods are investment goods, the total taxable bases and deductible input VAT for imports will appear in this box.

You can view the details of the calculations performed in the link available in the section located on the right margin, click on "VAT deductible".

If there are zero-rated intra-Community acquisitions during the period, the amount is not displayed in box 32 in Pre303 since the deductible rate is zero.

You can view the corresponding invoices in the link that exists in the tax fee for the Added Books.

Duties borne on imports of capital goods

"Taxable bases and deductible input VAT for imports of capital goods."

If the taxpayer has reported in the invoice registration that the goods are capital goods, the total taxable bases and deductible input taxes for imports will appear in this box.

You can view the details of the calculations performed in the link available in the section located on the right margin, click on "VAT deductible".

You can view the corresponding invoices in the link that exists in the tax fee for the Added Books.

INTRA-COMMUNITY ACQUISITIONS OF CURRENT GOODS AND SERVICES

"Taxable bases and deductible input VAT for intra-Community acquisitions of current goods and services."

If the taxpayer has not indicated in the invoice register that they are investment goods, the total taxable bases and deductible input VAT for intra-community acquisitions will appear in this box.

You can view the details of the calculations performed in the link available in the section located on the right margin, click on "VAT deductible".

If there are intra-community acquisitions at a zero rate during the period, the amount is not displayed in box 36 in the Pre303 because the deductible amount is zero.

You can view the corresponding invoices in the link that exists in the tax fee for the Added Books.

INTRA-COMMUNITY ACQUISITIONS OF INVESTMENT GOODS

"Taxable bases and deductible input VAT for intra-Community acquisitions of capital goods."

If the taxpayer has reported in the invoice registration that the goods are capital goods, the total taxable bases and deductible input taxes for intra-Community acquisitions will appear in this box.

You can view the details of the calculations performed in the link available in the section located on the right margin, click on "VAT deductible".

You can view the corresponding invoices in the link that exists in the tax fee for the Added Books.

CORRECTION OF DEDUCTIONS

"Taxable base and deductible amounts derived from corrective invoices whose settlement period corresponds to the self-assessment."

You can view the details of the calculations performed in the link available in the section located on the right margin, click on "VAT deductible".

You can view the corresponding invoices in the link that exists in the tax fee for the Added Books.

COMPENSATION SPECIAL REGIME AG And P.

“Amount of compensation paid to taxpayers covered by the Special Scheme for Agriculture, Livestock and Fishing.”

You can view the details of the calculations performed in the link available in the section located on the right margin, click on "VAT deductible".

You can view the corresponding invoices in the link that exists in the tax fee for the Added Books.

REGULARIZATION BY APPLICATION OF THE FINAL PRO RATA PERCENTAGE

Taxpayers subject to pro rata calculation must verify whether this box needs to be completed and, if so, manually enter the amount, as this data is not currently calculated automatically.

This box contains the result of the adjustment of the provisional deductions made during the year as a result of applying the final pro rata percentage that corresponds.

It will only be completed in the 4th quarter or month 12, or in cases of cessation of activity.