Consultation of Companies tax data

The online consultation of the 2025 tax data for Corporate Income Tax is a service for the purpose of completing the tax return for the 2025 tax year, exclusively for legal entities, regardless of the type of entity, the settlement period or whether they have submitted the self-assessment of the tax for the previous year.

Taxpayers whose tax period does not coincide with the calendar yearThat is, declaration types 2 and 3, should take into account that the data provided corresponds to the calendar year 2025.

To access in your own name, you need to identify yourself with an electronic certificate. ID card electronic or eIDAS.

This query only supports access with proxy (Does NOT support social collaboration) and the specific empowerment required is DFIS (Corporate Tax Data Consultation) or the general one for personal data consultation GENERAL ATPE.

At the top of the page you can find explanatory information about the tax data that will be provided in this service.

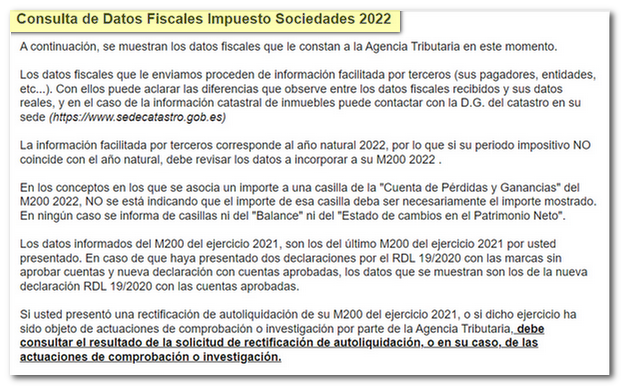

Below you will find the tax data for the year 2025. It does not have a printable format or option for downloading since it is an online consultation. This service only displays information provided by third parties that corresponds to the calendar year 2025. If the tax period does not coincide with the calendar year, you must review the data that you must include in your 2025 Form 200.

The data provided can be grouped into the following categories :

-

Data available at the Tax Agency from information returns or other sources of information from third parties . With them you can clarify the differences you observe between the tax data received and your real data, and in the case of property cadastral information you can contact the DG of the Cadastre at its headquarters (https://www.sedecatastro.gob.es)

-

Data from self-assessments and information returns of the taxpayer (M202, M190, M390 or M303).

-

In the concepts where an amount is associated with a box of the "Profit and Loss Account" of Model 200 of 2025, it is not being indicated that the amount of that box must necessarily be the amount shown. In no case are boxes reported on either the "Balance Sheet" or the "Statement of Changes in Net Worth".

-

Data declared in form 200 for the 2024 fiscal year corresponding to amounts pending application in future fiscal years, indicating the box of form 200 of the 2025 fiscal year in which they should be recorded. If you submitted a self-assessment correction for your Form 200 for the 2024 tax year, or if that tax year has been subject to verification or investigation by the Tax Agency, you should check the result of the self-assessment correction request, or, where applicable, the verification or investigation. Likewise, the information included on pages 1 and 2 will be provided.

-

Information to take into account in the declaration, such as those relating to penalties and surcharges issued and notified by the AEAT during the 2025 financial year, late payment interest paid by the AEAT and by other Administrations during 2025, etc.

-

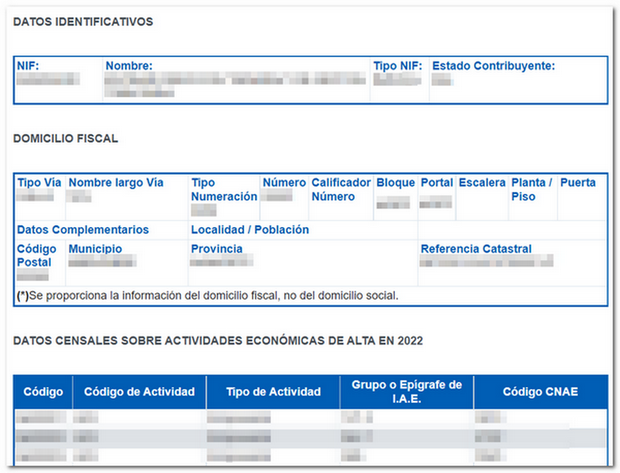

Sections of the IAE in which the taxpayer is registered, including the National Economic Activity Code ( CNAE ) equivalent.