Form 030

Skip information indexApplication for NIF of a natural person without NIF NIE not in person

Following the declaration of the state of alarm by RD 463/2020, the service "Application for NIF of a natural person - without DNI / NIE - not in person" was created to allow the non-face-to-face processing of the application for assignment of a tax identification number ( NIF ) without requiring the appearance of the interested party, or their representative or presenter, at the offices of the AEAT for:

- Spanish individuals who do not have a national identity document ( DNI )

- Foreigners who do not have NIE

They need a NIF because they are going to carry out operations of a tax nature or significance without requiring the appearance of the interested party at the offices of the AEAT .

This NIF assigned by the State Tax Administration Agency will be temporary until they obtain a DNI or a NIE , which is granted exclusively, in both cases, by the Ministry of the Interior.

This extraordinary procedure makes it possible to obtain the NIF with initial letter:

- K : Minors under 14 years of age, Spanish and residents in Spain

- L : Non-resident Spaniards of any age, not required to have DNI

- M: Foreigners who do not have NIE

When submitting the application for assignment of NIF K, L and M of a natural person, 3 steps must be followed:

- Obtaining the completed Form 030 in PDF ;

- Additional scanned documentation;

- Submission of Form 030 in PDF and the additional documentation required in the Electronic Registry of the Tax Agency in the procedure "Application for NIF of a natural person - without DNI / NIE - not in person".

STEP 1.- Obtaining the completed Form 030 in PDF

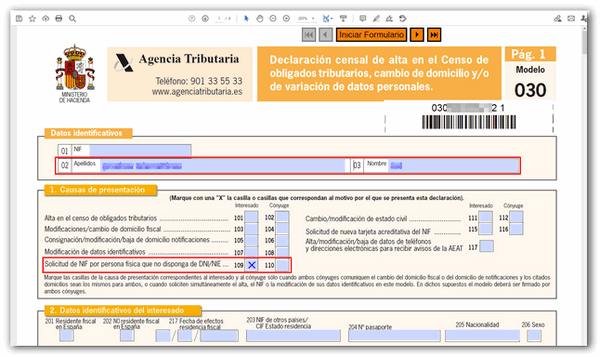

Download form 030 in PDF from the "Download form" link available in the "Related content" section of this help located on the right margin and, before printing it, fill it in with the necessary data to request the NIF by the holder or his representative. By clicking on "Fill Form" located at the top, the "Surname" and "Name" fields and the following sections of form 030 will be filled in:

- Reasons for submission which will be “Application by a natural person who does not have a DNI / NIE ”;

- Identification data of the interested party;

- Identification data of the spouse, if applicable;

- Telephone and email address information to receive notifications from the AEAT (to be completed if you want to receive notifications and especially information about the NIF assigned);

- Assignment of tax address (mandatory);

- Indication of a domicile abroad (if you are a non-resident and you indicate the domicile abroad as your tax domicile, it will be mandatory; otherwise, it is optional if you have already indicated a tax domicile in Spain);

- Assignment of the address for notification purposes (it would always be in Spain and is optional);

- Representative ( optional except in the case of minors and natural persons lacking tax capacity);

- Civil status;

- Date and signature of the declaration (mandatory, by the owner(s) or their representative).

Once Form 030 has been completed, printed and signed by the owner or his representative, it will be scanned in PDF format for submission via Electronic Registry following the instructions in STEP 3.

For any questions that may arise, you can use the help service for completing census forms by calling the Basic Tax Information telephone number 91 554 87 70.

STEP 2.- Additional scanned documentation

You must consult, obtain and, if applicable, scan the documentation that must accompany Form 030 of the application for NIF of a natural person before taking the next step.

The additional documentation will depend on the type of NIF requested. In the "Census Informant" you can consult the documentation that is necessary to provide in each case.

You can access the "Census Informant" in the electronic headquarters, in the section "Census, NIF and tax address", in the "Virtual assistance tools for Census and IAE ".

STEP 3.- Submission of Form 030 and additional documentation

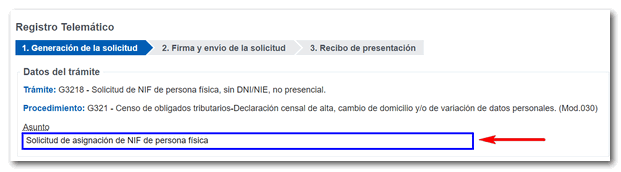

In the list of all the procedures of form 030 available in the "Highlighted procedures" section of this help located on the right margin, click on "Application for NIF of a natural person - without DNI / NIE - not in person".

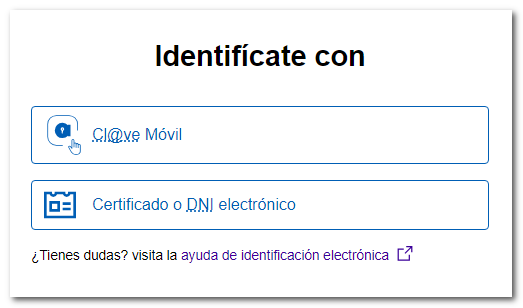

Access to the procedure requires that the presenter has a NIF registered in the Census of Taxpayers and identify himself with an electronic certificate, DNIe or Cl@ve .

Once identified, in the online registration process, you must complete the "Subject" field with the text: Request for assignment of NIF of a natural person. . In the type of presentation select "On your own behalf" or "On behalf of third parties" as appropriate.

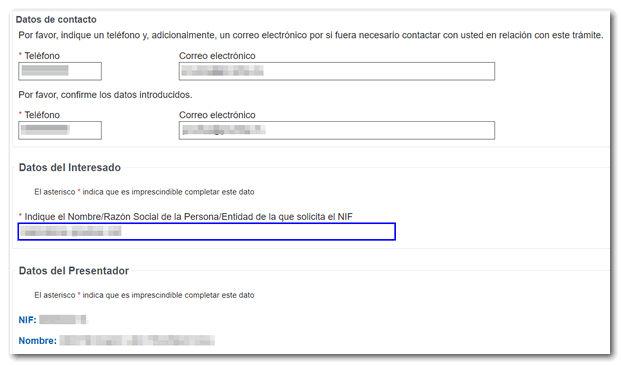

The presenter's telephone number and an email address must then be filled in in case it is necessary to contact them regarding this procedure.

Fill in the interested party's details. The presenter's data will show NIF and the name of the certificate or Cl@ve used to access the procedure.

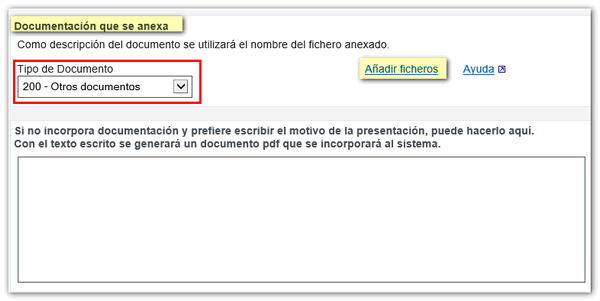

In the "Attached documentation" section, select "200 - Other documents" as the document type and click on the "Add files" link to select the file with the documentation you must submit. In the "Help" link you can check the list of formats accepted for submitting files for this procedure, the maximum size allowed for each file being 64 MB .

You must include Form 030 in PDF format obtained in STEP 1 and the additional documentation saved in STEP 2, identifying the content of each file (for example, Passport).

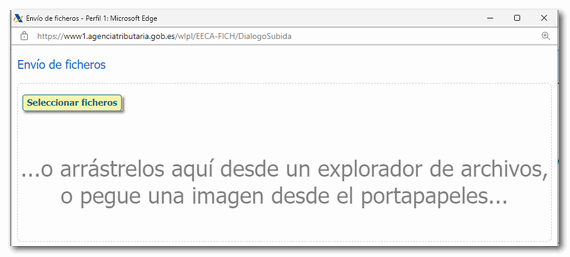

Select or drag the file. It is preferable that the file name does not have punctuation marks and is saved on the local disk, within the folder " AEAT ".

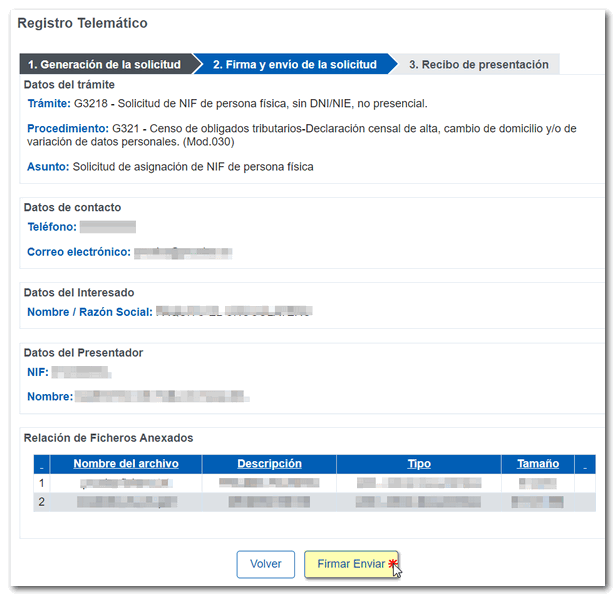

The added file will appear in the "Attached documentation" section.

When you are done attaching files, click "Submit" at the bottom. The data to be sent is then displayed. If you wish to make a change, press "Return" and if you agree, press "Sign Send".

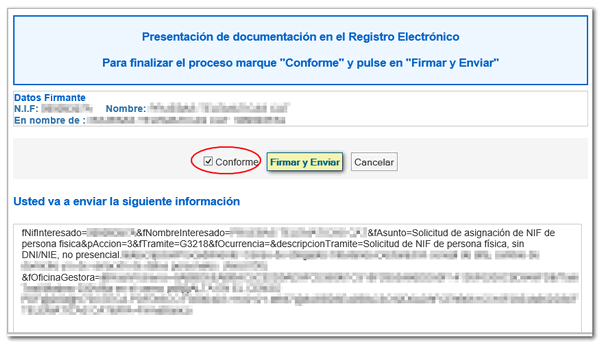

In the pop-up window, check the "I agree" box and click "Sign and Send" to complete the submission process.

Once this procedure has been carried out, an electronic Registration file is generated.

Once the NIF has been assigned, the communication of the NIF card will be issued to the tax address of the holder of the NIF assigned or, where applicable, to the preferred address for the purposes of notifications communicated in Form 030. If you have provided the telephone number or email address in the corresponding section of Form 030, you will receive a communication informing you of the Secure Verification Code for the communication of the NIF card assigned and you will be able to consult the NIF and print the card that accredits it.

It should be noted that failure to submit the necessary additional documentation or submitting it in an incomplete or inaccurate manner may result in the application being filed (articles 88 and 89 of the Regulations for the application of taxes, approved by Royal Decree 1065/2007, of July 27).